Best Car Insurance in Nebraska for 2026 [Find the Top 10 Companies Here]

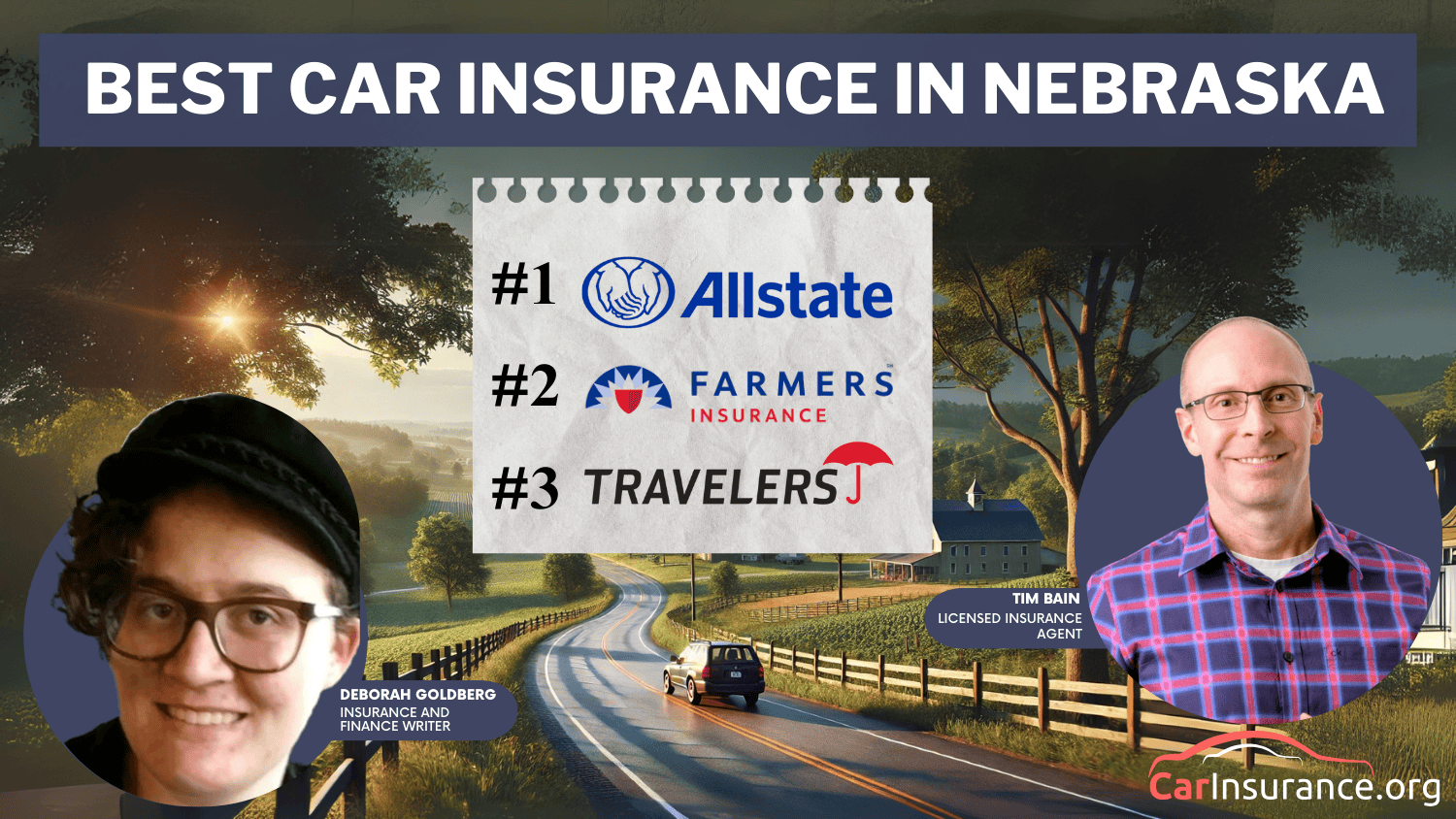

Allstate, Farmers, and Travelers provide the best car insurance in Nebraska at $33 per month. Allstate is great at bundling discounts, Farmers has family-friendly policies, and Travelers has exclusive savings. Compare Nebraska car insurance rates can help you get the best coverage.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Insurance Feature Writer

Rachel Bodine graduated from college with a BA in English. She has since worked as a Feature Writer in the insurance industry and gained a deep knowledge of state and countrywide insurance laws and rates. Her research and writing focus on helping readers understand their insurance coverage and how to find savings. Her expert advice on insurance has been featured on sites like PhotoEnforced, All...

Rachel Bodine

Licensed Insurance Agent

Eric Stauffer is an insurance agent and banker-turned-consumer advocate. His priority is educating individuals and families about the different types of insurance coverage. He is passionate about helping consumers find the best coverage for their budgets and personal needs. Eric is the CEO of C Street Media, a full-service marketing firm and the co-founder of ProperCents.com, a financial educat...

Eric Stauffer

Updated April 2025

3,072 reviews

3,072 reviewsCompany Facts

Full Coverage in Nebraska

A.M. Best Rating

Complaint Level

Pros & Cons

3,072 reviews 1,734 reviews

1,734 reviewsCompany Facts

Full Coverage in Nebraska

A.M. Best Rating

Complaint Level

Pros & Cons

1,734 reviewsAllstate, Farmers, and Travelers provide the best car insurance in Nebraska. Allstate is the highest-rated due to its comprehensive coverage and starting monthly rates of $33.

Allstate offers impressive bundling discounts, while Farmers specializes in family-friendly policies. Travelers provides special savings.

Choosing the right provider can help you get lower rates than the average cost of auto insurance in NE, especially for households with teen drivers.

Our Top 10 Company Picks: Best Car Insurance in Nebraska

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 25% | A+ | Comprehensive Coverage | Allstate | |

| #2 | 20% | A | Family Plans | Farmers |

| #3 | 13% | A++ | Innovative Discounts | Travelers | |

| #4 | 25% | A | Customizable Policies | Liberty Mutual | |

| #5 | 25% | A | Family Focus | American Family | |

| #6 | 17% | B | Wide Availability | State Farm | |

| #7 | 10% | A+ | Technology Integration | Progressive |

| #8 | 25% | A++ | Competitive Pricing | Geico | |

| #9 | 20% | A+ | Strong Financials | Nationwide | |

| #10 | 10% | A++ | Military Focus | USAA |

Choosing the right provider can help you get lower rates than the average cost of auto insurance in NE, especially for households with teen drivers.

- Allstate offers comprehensive coverage and strong bundling discounts

- Farmers has family-friendly policies with multi-vehicle discounts

- Travelers stands out with unique savings for eco-conscious drivers

If you’re also considering how to find a safe, budget-friendly car for your teen, comparing policies and coverage options can help ensure the best protection at the lowest cost.

Shop for the best NE car insurance with our free quote comparison tool. Enter your ZIP code to begin.

#1 – Allstate: Top Overall Pick

Pros

- Generous Bundling Discount: Up to 25% savings on auto insurance in Nebraska when bundling it with home or life insurance.

- Comprehensive Coverage Options: Accident forgiveness and new car replacement, providing improved monetary protection in accidents.

- Strong Local Agent Network: Nebraska-based agents provide excellent customer service. Read more: Allstate Car Insurance Review

Cons

- Higher Premium Costs: Young or high-risk drivers pay significantly higher premiums, making it less budget-friendly than other car insurance companies in Nebraska.

- Discounts Often Require Bundling: Most savings require combining multiple policies and limiting standalone discount options.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#2 – Farmers: Best for Family Plans

Pros

- Family-Friendly Policies: Multi-driver and multi-vehicle discounts make it an excellent option for families seeking affordable auto insurance quotes in Nebraska.

- Personalized Customer Support: It provides in-person agent support, allowing policyholders to have a more hands-on experience with changes to their policies and claims.

- Adaptable Coverage Options: Policies can be adjusted to driver requirements, providing flexibility that enables protection to be modified easily according to your budget.

Cons

- Not the Cheapest: Premiums can be more expensive than those of its competitors, which is a disadvantage for budget-friendly users. Learn more: Farmers Car Insurance Review

- Limited Digital Tools: Online policy management is less developed than other companies, which is a hassle for tech-savvy users.

#3 – Travelers: Best for Innovative Discounts

Pros

- Green Vehicle Discounts: Special pricing is available for hybrid and electric vehicle owners, helping lower Nebraska auto insurance rates.

- Accident Forgiveness: Avoids premium hikes after the first accident, giving responsible drivers financial relief in unexpected situations.

- Gap Insurance: Gap insurance insures drivers financing or leasing cars so they don’t incur significant out-of-pocket expenses after a total loss.

Cons

- Fewer Local Representatives: Fewer Nebraska-based customer support agents can lead to extended wait times when contacting an agent for assistance.

- Limited Bundling Options: Travelers car insurance reviews suggest that bundling discounts aren’t as substantial as competitors.

#4 – Liberty Mutual: Best for Customizable Policies

Pros

- Broad Customization: You can customize deductibles, add endorsements, and change policies.

- RightTrack Safe Driving Program: Safe drivers save on premiums via telematics programs and save substantially on auto insurance quotes in Nebraska.

- Distinct Coverage Add-ons: The new vehicle replacement and deductible savings make it a great option. Read more about them in our Liberty Mutual car insurance review.

Cons

- Higher Minimum Rates: Premiums tend to be more expensive unless drivers get discounts, which can cause cost issues for some policyholders.

- Poor Customer Service Reviews: Some policyholders gripe about delays in processing claims.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#5 – American Family: Best for Family Focus

Pros

- Family-Oriented Discounts: Offers discounts for young drivers, students, and multi-car households, making car insurance rates in Nebraska more affordable.

- Solid Financial Strength: By maintaining a high A.M. Best rating, American Family guarantees dependability for claims payments and long-term financial stability.

- Local Nebraska Presence: Most drivers seek face-to-face service from its robust agent network. The American Family car insurance review covers this in more detail.

Cons

- Limited Availability: Policies are not offered in all states, making it less accommodating for people moving around.

- Bundling Necessary for Discounts: The optimal savings necessitate bundling with home or life insurance, restricting standalone options.

#6 – State Farm: Best for Wide Availability

Pros

- Largest Agent Network: Its widespread availability makes it a leading provider for those looking for reliable NE auto insurance.

- Low-Cost Senior Driver Rates: Married and senior drivers 60 years of age and above pay lower premiums, contributing to long-term savings.

- User-Friendly Mobile App: The State Farm car insurance review also notes its highly rated app, which features policy management, payments, and e-claim processing.

Cons

- Higher Rates for Younger Drivers: Teens and young adults tend to pay above-average premiums, challenging affordability.

- Fewer Unique Discounts: Lacks incentives like green vehicle discounts, making it less competitive for those looking for specialty savings.

#7 – Progressive: Best for Technology Integration

Pros

- Snapshot Program: It rewards safe driving with lower rates for those who need affordable NE car insurance.

- Strong Digital Experience: Its mobile app and website offer convenient policy management, quote comparison, and paperless billing.

- Competitive Multi-Car Discounts: Drivers can save considerably when insuring more than one car. Read more: Progressive Car Insurance Review

Cons

- High Rates for High-Risk Drivers: High-risk or accident-prone drivers are charged more than other providers.

- Poor Service: Customer service is inconsistent, with varying reports of claims processing time.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#8 – Geico: Best for Competitive Pricing

Pros

- Typically Lower Rates: Geico’s rates are lower than the average car insurance costs in Nebraska.

- Good Student & Military Discount: Discounts for young students and military members decrease premium costs.

- Highly-Ranked Mobile App: Its user-friendly app streamlines claims, policy renewals, and premium payments for customers. Read more about it in our Geico car insurance review.

Cons

- Limited Local Agent Availability: This system heavily depends on online resources, which may be inconvenient for those who prefer in-person customer support.

- Fewer Coverage Add-ons: It does not include options such as gap insurance, which specific drivers may find valuable for additional financial security.

#9 – Nationwide: Best for Financial Stability

Pros

- Strong A.M. Best Rating: Offers financial strength, guaranteeing safe claim payments for Nebraska auto insurance policyholders.

- Vanishing Deductible: Safe drivers see their deductible decrease over time, which reduces overall expenses in the future.

- SmartRide Program: Nationwide car insurance reviews discuss its telematics program as an excellent option for getting safe driver discounts.

Cons

- Limited Discounts for Young Drivers: There are no significant discounts for teenage or first-time drivers.

- Higher Rates in Urban Areas: Cities like Omaha may experience higher-than-expected premiums compared to rural areas.

#10 – USAA: Best for Military Focus

Pros

- Lower Rates for Military: USAA offers cheaper coverage for military members and their families compared to other car insurance companies in Nebraska.

- High Customer Satisfaction: USAA car insurance reviews consistently rank the company among the best insurers for claims handling and overall customer service.

- Exclusive Member Perks: Provides financial planning resources, premium banking services, and other advantages to qualified members.

Cons

- Restricted to Military Families: Not for public use, limiting access to its competitive pricing.

- Fewer Physical Branches: Based primarily online, which might not be ideal for those who need face-to-face service.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Nebraska Car Insurance Coverage and Rates

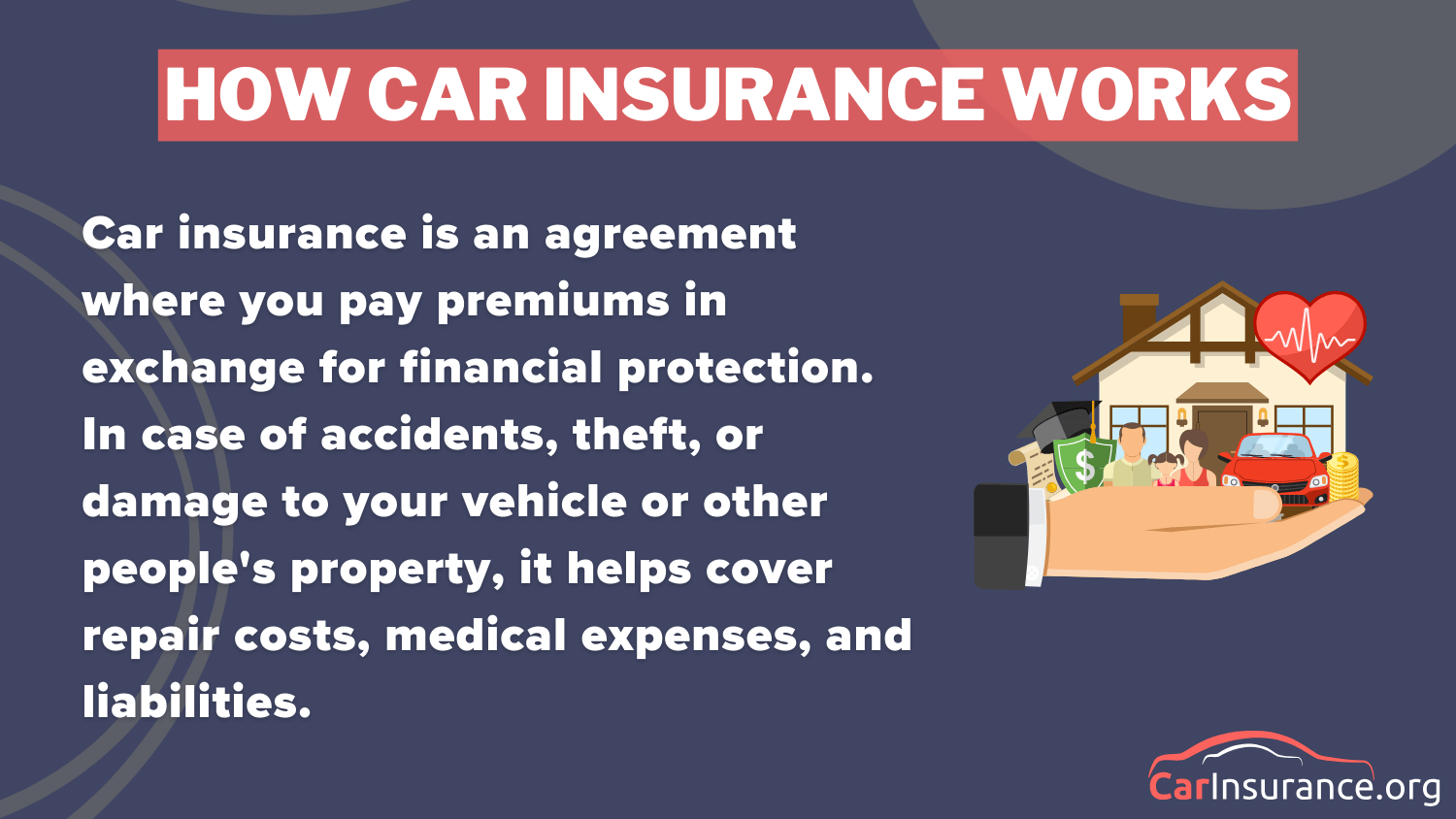

Car insurance shields Nebraska motorists from accident expenses, damage to vehicles, and liability. It offers minimum and full coverage. Understanding how car insurance works allows drivers to select protection against risks such as theft, vandalism, and inclement weather.

Nebraska Car Insurance Monthly Rates by Provider & Coverage Level

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $33 | $125 | |

| $30 | $112 | |

|

| $35 | $130 |

| $25 | $92 | |

| $48 | $179 | |

| $20 | $77 | |

|

| $25 | $95 |

| $18 | $69 | |

| $27 | $102 | |

| $15 | $56 |

Insurance costs vary by provider and type of coverage. Minimum coverage with USAA costs $15 per month, and full coverage costs $179 per month with Liberty Mutual. State Farm and Geico provide competitive rates.

Drivers will obtain the best auto insurance in Nebraska by comparing quotes and coverage.

Price isn’t the only factor in choosing insurance. Customer service, claims handling, and discounts matter. Many providers offer savings for bundling policies or safe driving. Comparing providers helps Nebraska drivers find affordable, reliable protection.

Nebraska Car Insurance Discounts

Nebraska drivers can lower costs with discounts from top providers. Car insurance in NE comes with savings for safe drivers, students, and multi-policy holders. Military and eco-friendly discounts are also available.

Car Insurance Discounts From the Top Providers in Nebraska

| Insurance Company | Available Discounts |

|---|---|

| Multi-Policy Discount, Safe Driver Discount, Anti-Theft Device Discount, New Car Discount | |

| Multi-Policy Discount, Safe Driver Discount, Defensive Driving Course Discount, Good Student Discount | |

|

| Multi-Policy Discount, Safe Driver Discount, Good Student Discount, Alternative Fuel Discount |

| Multi-Policy Discount, Defensive Driving Discount, Good Student Discount, Military Discount | |

| Multi-Policy Discount, Good Student Discount, Anti-Theft Device Discount, New Car Discount | |

| Multi-Policy Discount, Safe Driver Discount, Accident-Free Discount, Defensive Driving Discount | |

|

| Multi-Policy Discount, Snapshot Discount, Good Student Discount, Homeowner Discount |

| Multi-Policy Discount, Safe Driver Discount, Defensive Driving Discount, Good Student Discount | |

| Multi-Policy Discount, Safe Driver Discount, Hybrid/Electric Vehicle Discount, New Car Discount | |

| Multi-Policy Discount, Safe Driver Discount, Good Student Discount, Military Discount |

Insurers offer percentage-based savings. Bundling can save up to 30%, and usage-based programs reward safe driving. Defensive driving courses can also lower rates. Comparing options ensures the best discounts.

Nebraska Auto Insurance Discounts

| Insurance Company | Anti-Theft | Bundling | Good Driver | Good Student | UBI |

|---|---|---|---|---|---|

| 15% | 25% | 20% | 15% | 10% | |

| 10% | 29% | 10% | 15% | 20% | |

|

| 10% | 25% | 10% | 15% | 10% |

| 23% | 25% | 22% | 15% | 10% | |

| 15% | 30% | 10% | 15% | 30% | |

| 10% | 20% | 10% | 15% | 10% | |

|

| 10% | 20% | 10% | 15% | 30% |

| 15% | 17% | 15% | 25% | 30% | |

| 10% | 15% | 10% | 15% | 20% | |

| 20% | 10% | 30% | 15% | 15% |

To save more, check the 10 cheapest car insurance companies. Geico offers 23% off for anti-theft devices, and USAA gives 30% off for good drivers. Researching discounts helps Nebraska drivers find affordable coverage.

Nebraska Car Insurance Claims and Premiums

Collisions make up 30% of claims, averaging $3,500. Weather damage follows at 25%, costing $2,500. Theft, vandalism, and animal crashes add to the risks. Collision vs. comprehensive car insurance helps cover these dangers.

5 Most Common Auto Insurance Claims in Nebraska

| Claim Type | Portion of Claims | Cost per Claim |

|---|---|---|

| Collisions | 30% | $3,500 |

| Weather-Related Damage | 25% | $2,500 |

| Theft | 15% | $7,000 |

| Vandalism | 10% | $2,200 |

| Animal-Related Accidents | 20% | $3,000 |

Omaha sees 5,000 crashes yearly, with 3,200 claims. Lincoln reports 2,500 accidents and 1,800 claims. Even smaller cities face risks, making insurance essential.

Nebraska earns an A for low theft rates, but weather risks bring a B rating. A B+ in claim size and a C in traffic density affect premiums statewide.

Nebraska Accidents & Claims per Year by City

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Bellevue | 1,000 | 700 |

| Grand Island | 800 | 500 |

| Kearney | 600 | 400 |

| Lincoln | 2,500 | 1,800 |

| Omaha | 5,000 | 3,200 |

Uninsured drivers are a concern, earning Nebraska a C grade. To avoid financial loss, adding uninsured motorist coverage can provide better protection.

Vehicle insurance rates in Nebraska differ depending on accident rates, where you reside, and the policy. Rural residents pay less, but storms and wildlife require coverage.

Nebraska Report Card: Auto Insurance Premiums

| Category | Grade | Explanation |

|---|---|---|

| Vehicle Theft Rate | A | Low vehicle theft rate compared to national averages. |

| Average Claim Size | B+ | Moderate claim size, with weather and collision claims being common. |

| Weather-Related Risk | B | Moderate risk from storms and winter conditions. |

| Traffic Density | C | Lower traffic density compared to larger states. |

| Uninsured Drivers Rate | C | Slightly higher uninsured driver rate compared to the national average. |

Accident patterns, weather, and uninsured rates dictate Nebraska’s insurance market. Protection through proper coverage shields drivers from paying huge amounts.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Minimum Car Insurance Coverage Requirements in Nebraska

In order to drive lawfully in Nebraska, drivers must comply with the state’s auto insurance requirements, which require a minimum of 25/50/25 liability coverage. Noncompliance can lead to fines, suspension of the license, or increased insurance premiums.

Liability insurance covers others’ damages, not the policyholder’s. Additional coverage like uninsured motorist insurance is useful, considering how the states rank on uninsured drivers, ensuring better protection against losses.

Allstate excels with strong financial stability and valuable policy options, ensuring NE drivers stay protected in any situation.Michelle Robbins Licensed Insurance Agent

Meeting state insurance laws keeps drivers compliant and financially secure. Minimum coverage may not be enough for severe accidents, so increasing limits can prevent high out-of-pocket costs and offer peace of mind.

How to Find the Best Car Insurance

Choosing the proper policy is important to cover yourself financially while keeping it affordable. With so many options, understanding what to look for can assist you in making the optimal choice.

- Determine Your Coverage Needs: Depending on the value of your car, your budget, and how you drive, decide if you require basic liability, full coverage, or optional features such as roadside assistance. Reading a Nebraska auto insurance guide can also enlighten you regarding state-specific needs.

- Compare Insurance Companies: Shop at least three companies, comparing their rates, discounts, and customer reviews to determine financial stability and service quality.

- Get & Compare Quotes: Get personalized quotes online or through agents, comparing various levels of coverage to ensure the proper level of affordability versus protection.

- Seek Discounts & Savings: Search for available discounts, such as bundling, good driver rewards, and telematics programs, as well as multi-vehicle and safe driving practice savings.

- Review and Purchase a Policy: Carefully go over the policy details, ensuring you understand the terms, limits, and exclusions. Understanding different types of car insurance coverage will help you make an informed choice.

Always check and compare policies so that you secure dependable coverage at a reasonable rate. With an appropriate policy, you’ll rest easy knowing that you’re adequately covered financially when driving.

Best Car Insurance in Nebraska: Top Providers & Savings

Obtaining the best auto insurance in Nebraska starts with comparing the top auto insurance providers like Allstate, Farmers, and Travelers that offer excellent insurance coverage and discounts. Motorists can compare minimum and comprehensive coverage using our car insurance guide for maximum safety.

Comparing Nebraska car insurance companies guarantees inexpensive premiums and policies that meet individual requirements. Shop for the best NE car insurance with our free quote comparison tool. Enter your ZIP code to begin.

Frequently Asked Questions

How do Farmers’ multi-car and young-driver discounts compare to other providers?

Farmers provide family-friendly plans with multi-car and young driver discounts, making it ideal for Nebraska households needing tailored coverage. Look at our how to find a safe, budget-friendly car for your teen for expanded insights.

Which car insurance provider in Nebraska offers the best bundling discounts?

Allstate offers a 25% bundling discount, making it one of the best options for combining home and auto insurance to maximize savings. Ready to find cheaper car insurance coverage? Enter your ZIP code to begin.

What exclusive benefits does USAA provide for military members and their families?

USAA provides exclusive benefits like banking services and superior claims handling, but its coverage is limited to military members and their families.

Why is Liberty Mutual considered one of the best insurance providers in Nebraska?

Liberty Mutual allows extensive policy customization, offering unique add-ons like better car replacement and deductible savings programs. Dive into our car insurance with telematics to gain a deeper insight.

How does the American Family’s local presence in Nebraska benefit policyholders?

American Family’s strong local presence in Nebraska ensures policyholders receive personalized customer service and claims support.

What makes State Farm’s Drive Safe & Save program beneficial for Nebraska drivers?

State Farm’s Drive Safe & Save program rewards safe drivers with discounts based on monitored driving habits, potentially saving them up to 30%.

How does Nationwide’s Vanishing Deductible program work?

Nationwide’s Vanishing Deductible program reduces deductibles over time, rewarding policyholders for each year of safe driving. Explore how to drive safely, no matter the time of day, for more insights.

What are the potential downsides of Progressive’s Snapshot usage-based program?

Progressive’s Snapshot program can increase rates for drivers with inconsistent braking, high-speed habits, or late-night driving patterns.

Why is Geico considered one of the most affordable insurance providers in Nebraska?

Geico remains among the most affordable options due to its competitive base rates and extensive discounts, including military and good student savings. Get the right car insurance coverage. Enter your ZIP code to shop for coverage from the top insurers.

How does Travelers’ green vehicle discount work, and what types of cars qualify for savings?

Travelers offer a green vehicle or “eco-friendly” discount for hybrid and electric cars, helping eco-conscious drivers lower their premiums. Learn how to lower your car insurance costs.

Related Articles

-

Apr 2025

Best Car Insurance in Utah for 2026 [Find the Top 10 Companies Here]

-

Mar 2025

Best Car Insurance in Louisiana for 2026 [Check Out the Top 10 Companies]

-

Mar 2025

Best Car Insurance in North Carolina for 2026 [10 Standout Companies]

-

Mar 2025

Best Car Insurance in Delaware for 2026 [Check Out the Top 10 Companies]

-

Mar 2025

Best Car Insurance in California for 2026 [Check Out These 10 Companies]

-

Feb 2025

Best Car Insurance in Vermont for 2026 [Your Guide to the Top 10 Companies]

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.