Deadly accidents in Hawaii continue to be problematic, with 120 deadly wrecks and 130 deaths yearly. Deadly crashes have a very big effect on car wrecks and claims statewide.

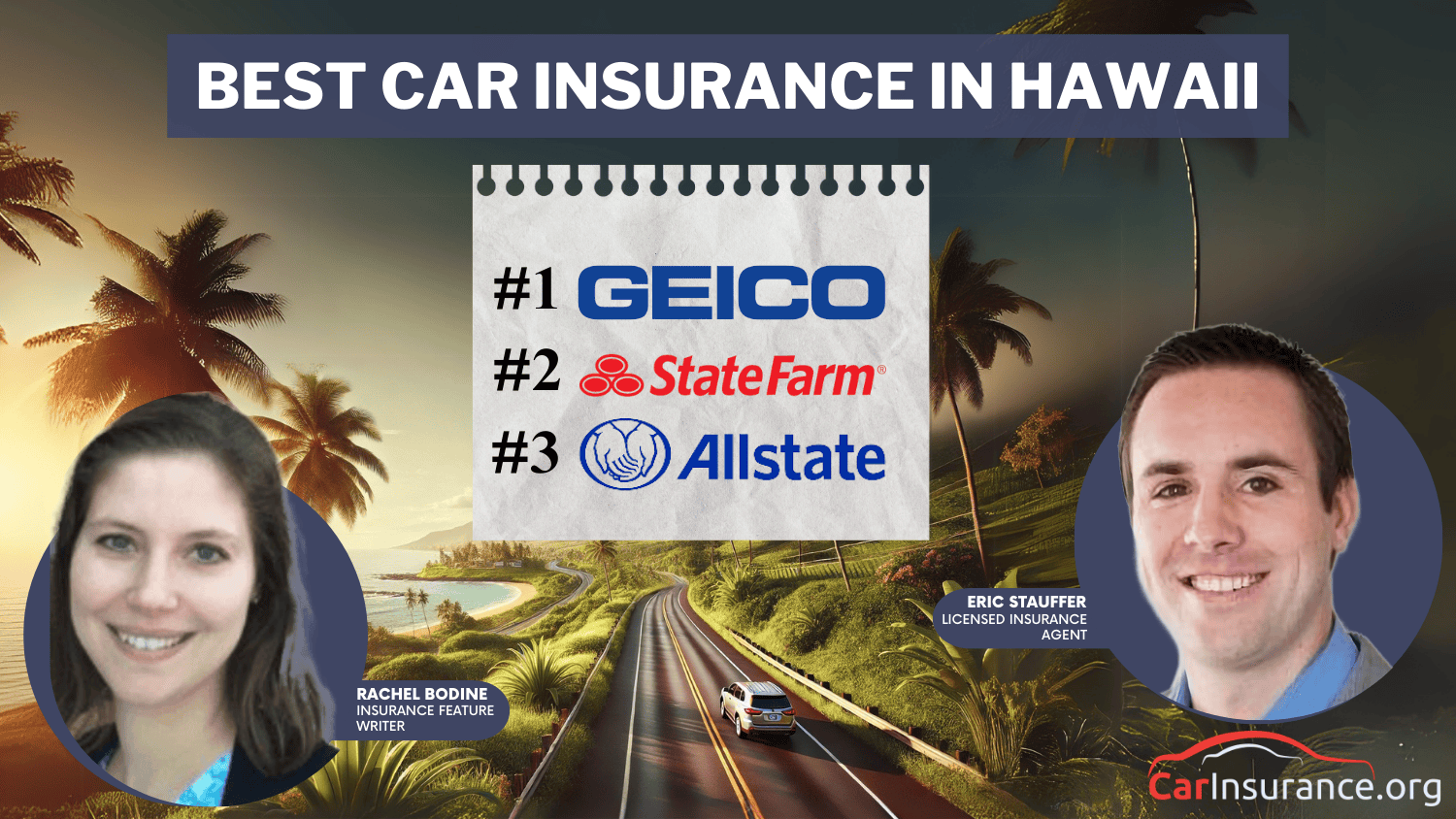

Best Car Insurance in Hawaii for 2026 [Check Out the Top 10 Companies]

Geico, State Farm, and Allstate provide the best car insurance in Hawaii. Monthly Hawaii car insurance rates start at $22. These HI car insurance providers excel based on their low rates, top-notch customer service, and customized coverage plans.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Updated Mar 2024

Learn more about Liberty Mutual Insurance, what products they offer, what their consumers think about them and... more

Learn more about Liberty Mutual Insurance, what products they offer, what their consumers think about them and how they compare against other carriers. less

Updated Jul 2025

Is State Farm Insurance good? As one of the most popular providers in the country, State Farm boasts strong fi... more

Is State Farm Insurance good? As one of the most popular providers in the country, State Farm boasts strong financial ratings and positive customer reviews. State Farm homeowners insurance reviews rank it in the top ten for claims satisfaction. Coverage is also available in all 50 states, which is important to Florida less

Updated Dec 2021

Learn more about Nationwide, what products they offer, what their consumers think about them and how they comp... more

Learn more about Nationwide, what products they offer, what their consumers think about them and how they compare against other carriers. less

Updated Mar 2025

For more than 90 years, American Family has been protecting and supporting its customers with strong customer ... more

For more than 90 years, American Family has been protecting and supporting its customers with strong customer service. They claim to be more than just an insurance company. They want to transform the way you think about insurance. At AmFam, they believe your dreams are important and that is why they work hard to protec less

Table of Contents

Table of Contents

Rachel Bodine

Insurance Feature Writer

Rachel Bodine graduated from college with a BA in English. She has since worked as a Feature Writer in the insurance industry and gained a deep knowledge of state and countrywide insurance laws and rates. Her research and writing focus on helping readers understand their insurance coverage and how to find savings. Her expert advice on insurance has been featured on sites like PhotoEnforced, All...

Written by

Rachel Bodine

Rachel Bodine

Eric Stauffer

Licensed Insurance Agent

Eric Stauffer is an insurance agent and banker-turned-consumer advocate. His priority is educating individuals and families about the different types of insurance coverage. He is passionate about helping consumers find the best coverage for their budgets and personal needs. Eric is the CEO of C Street Media, a full-service marketing firm and the co-founder of ProperCents.com, a financial educat...

Reviewed by

Eric Stauffer

Eric Stauffer

Updated April 2025

2nd Best in Hawaii: State Farm

18,157 reviewsCompany Facts

Full Coverage in Hawaii

$64/mo

A.M. Best Rating

A++

Complaint Level

Low

Pros & Cons

18,157 reviews3rd Best in Hawaii: Allstate

11,640 reviews

11,640 reviewsCompany Facts

Full Coverage in Hawaii

$118/mo

A.M. Best Rating

A+

Complaint Level

High

Pros & Cons

11,640 reviewsGeico, State Farm, and Allstate provide the best car insurance in Hawaii. Geico offers the cheapest rates, starting at $22 per month.

All these insurers are famous for their cheap premiums, good customer service, and complete coverage plans tailored specifically to Hawaii drivers.

Our Top 10 Company Picks: Best Car Insurance in Hawaii

| Company | Rank | Monthly Rates | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | $59 | A++ | Low Rates | Geico | |

| #2 | $64 | B | Local Agents | State Farm | |

| #3 | $118 | A+ | Comprehensive Coverage | Allstate | |

| #4 | $78 | A+ | Customizable Plans | Progressive |

| #5 | $44 | A++ | Military Families | USAA | |

| #6 | $99 | A | Personalized Service | Farmers |

| #7 | $128 | A | Coverage Add-Ons | Liberty Mutual | |

| #8 | $84 | A+ | Claims Satisfaction | Nationwide | |

| #9 | $82 | A | Family Discounts | American Family | |

| #10 | $72 | A++ | Discount Programs | Travelers |

Compare RatesStart Now →

When comparing the various options, it’s important to consider the range of Hawaii car insurance policies that suit your requirements. Understanding the different types of car insurance coverage will help you choose the best policy.

Just the Basics

- Geico offers the best car insurance in Hawaii with low rates

- Local agents and personalized service make State Farm a top choice

- Allstate provides comprehensive coverage tailored to Hawaii’s needs

Our free comparison tool provides you with precise quotes from leading providers in your region, enabling you to make a well-informed choice.

Read More: Car Insurance Rates by State

By comparing prices, you can get the best coverage at the lowest cost. See how much you’ll pay for car insurance by entering your ZIP code into our free comparison tool.

#1 – Geico: Top Overall Pick

Pros

- Discount Rates for Drivers: Geico offers low premiums on Hawaii car insurance policies.

- Significant Discounts: Geico offers policyholders a 25% bundle discount, which helps them save even more money.

- Convenient Online Policy Maintenance: Geico’s online tools make managing your insurance policy and submitting a claim simple.

Cons

- Limited In-Person Support: Geico offers low rates, but there are fewer local agents available to help in person.

- Varied Customer Experiences: Some drivers allege that claims resolution can be uneven, according to Geico car insurance reviews.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#2 – State Farm: Best for Local Agents

Pros

- Trustworthy Agent Support: Hawaii residents can rely on experienced agents for tailored support.

- Efficient Claims Experience: Several policyholders across the state report that making claims is quick and convenient.

- Multiple Discount Options: Discount opportunities, like those for secure drivers and scholars, can minimize premiums for Hawaii auto insurance customers.

Cons

- Higher Premium Charges: Insurance premiums in this state are usually higher than some competitors.

- Limited Internet Access: Our State Farm car insurance review observed that resolving policies typically entails speaking to agents directly.

#3 – Allstate: Best for Comprehensive Coverage

Pros

- Extensive Coverage Options: Allstate offers flexible policies that accommodate different needs, including accident forgiveness. For a more detailed overview of its options, read our Allstate car insurance review.

- Bundling Discounts: Combining home and auto policies can lead to significant savings for families.

- Safe-Driving Rewards: The Drivewise program helps responsible drivers lower their insurance costs, especially for long-term policyholders.

Cons

- Higher Premiums: Young and high-risk drivers tend to pay higher premiums, making it an expensive option.

- Competitive Discounts: Allstate provides fewer discount opportunities for HI auto insurance.

#4 – Progressive: Best for Customizable Plans

Pros

- Specialized Coverage: Offers unique policy options, such as rideshare insurance, tailored to local needs.

- Safe Driving Discounts: Responsible drivers can save through the Snapshot program. For more details, check out our Progressive car insurance review.

- Reasonably Rates for High-Risk Drivers: Compared to other providers, rates may be lower for drivers with a history of infractions.

Cons

- Potential Rate Increases: Some policyholders could face increased premiums after several years.

- Slower Claims Process: Drivers who buy Hawaii vehicle insurance may find that the claims settlement procedure takes longer than they had anticipated.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#5 – USAA: Best for Military Families

Pros

- Customized Military Policies: USAA offers policies specifically designed to meet the needs of service members, veterans, and their families.

- Top-Rated Customer Support: Many policyholders praise USAA for its excellent claims handling and assistance. Check out our USAA car insurance review.

- Exclusive Discounts for Active-Duty Members: Military personnel, especially those deployed or storing their vehicles, may qualify for unique savings.

Cons

- Limited Eligibility in Hawaii: Only military personnel, veterans, and their families are covered, which could restrict choices for others looking for Hawaii auto insurance quote.

- Fewer Physical Branches: USAA is primarily online or phone-based, which could be a hassle for those who want face-to-face service.

#6 – Farmers: Best for Personalized Service

Pros

- Customizable Plans: The unique variety of add-ons allows policyholders to choose their coverages.

- Enhanced Protection: Benefits like new car replacement help protect residents in coastal and urban areas against unforeseen accidents.

- Multi-Policy Discount: Major savings can be achieved when you combine auto, home, and life insurance.

Cons

- Higher Premiums: Hawaii car insurance premiums may be higher than those of other online insurers, making it less affordable for budget-conscious drivers.

- Discount Restrictions: Some savings programs have strict eligibility requirements. Our Farmers car insurance review provides more details.

#7 – Liberty Mutual: Best for Coverage Add-Ons

Pros

- Extensive Optional Protections: Hawaii drivers can enjoy other coverage, including benefits like better car replacement.

- Accident Forgiveness: Helps prevent premiums from increasing after an at-fault claim in Hawaii.

- Discounts for Safe Drivers: Liberty Mutual usually offers low rates to Hawaiians with clean driving records.

Cons

- Higher Premiums: Compared with Geico or USAA, car insurance rates in Hawaii may be higher.

- Customer Service Reviews: Some drivers in Hawaii report delays in claims handling and processing. Take a look at our Liberty Mutual car insurance review.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#8 – Nationwide: Best for Claims Satisfaction

Pros

- Efficient Claims Processing: Customers in Hawaii praise Nationwide’s fast and efficient claim resolutions. For more details, see our Nationwide car insurance review.

- Safe Driving Vanishing Deductible: The vanishing deductible for safe driving benefits decreases the amount you pay in the long run.

- Flexible Policy Adjustments: Hawaii residents can benefit from several add-ons offered for enhanced customization of coverage.

Cons

- Not Cost-Effective: The premiums are higher compared to other providers.

- Strict Discount Conditions: Specific discount schemes come with caps, so eligibility will differ when comparing auto insurance quotes in Hawaii.

#9 – American Family: Best for Family Discounts

Pros

- Savings for Multi-Car Households: Families in Hawaii can cut costs by insuring multiple vehicles under the same policy.

- Local Agent Support: Hawaiian policyholders benefit from personalized service and hands-on assistance from nearby agents.

- Teen Driver Discounts: Young motorists can take advantage of special programs that help lower insurance costs. This can be especially helpful when comparing car insurance quotes in Hawaii.

Cons

- Limited Reach: Unlike Geico or State Farm, American Family isn’t as widely available, which may impact accessibility. For more details, check out our American Family car insurance review.

- Basic Online Features: While policyholders can manage their accounts digitally, American Family’s tools aren’t as advanced as those of some competitors.

#10 – Travelers: Best for Discount Programs

Pros

- Broad Discounts: Hawaii motorists can get discounts such as multi-policy, safe driving, and home bundling.

- Usage-Based Program: The IntelliDrive program rewards good driving habits, offering not only lower premiums but also an opportunity to save more based on your driving.

- Competitive Rates for Eco-Friendly Cars: For hybrid and electric vehicle owners in Hawaii, there are often better and more affordable rates, which makes eco-friendly options even more attractive.

Cons

- Higher Premiums for Younger Drivers: Drivers under 25 may face higher coverage costs. Check Travelers car insurance review for insights on affordability.

- Customer Service Quality: Customer service quality can be different depending on the location and the agent, so experiences may vary.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Car Insurance Coverage and Rates in Hawaii

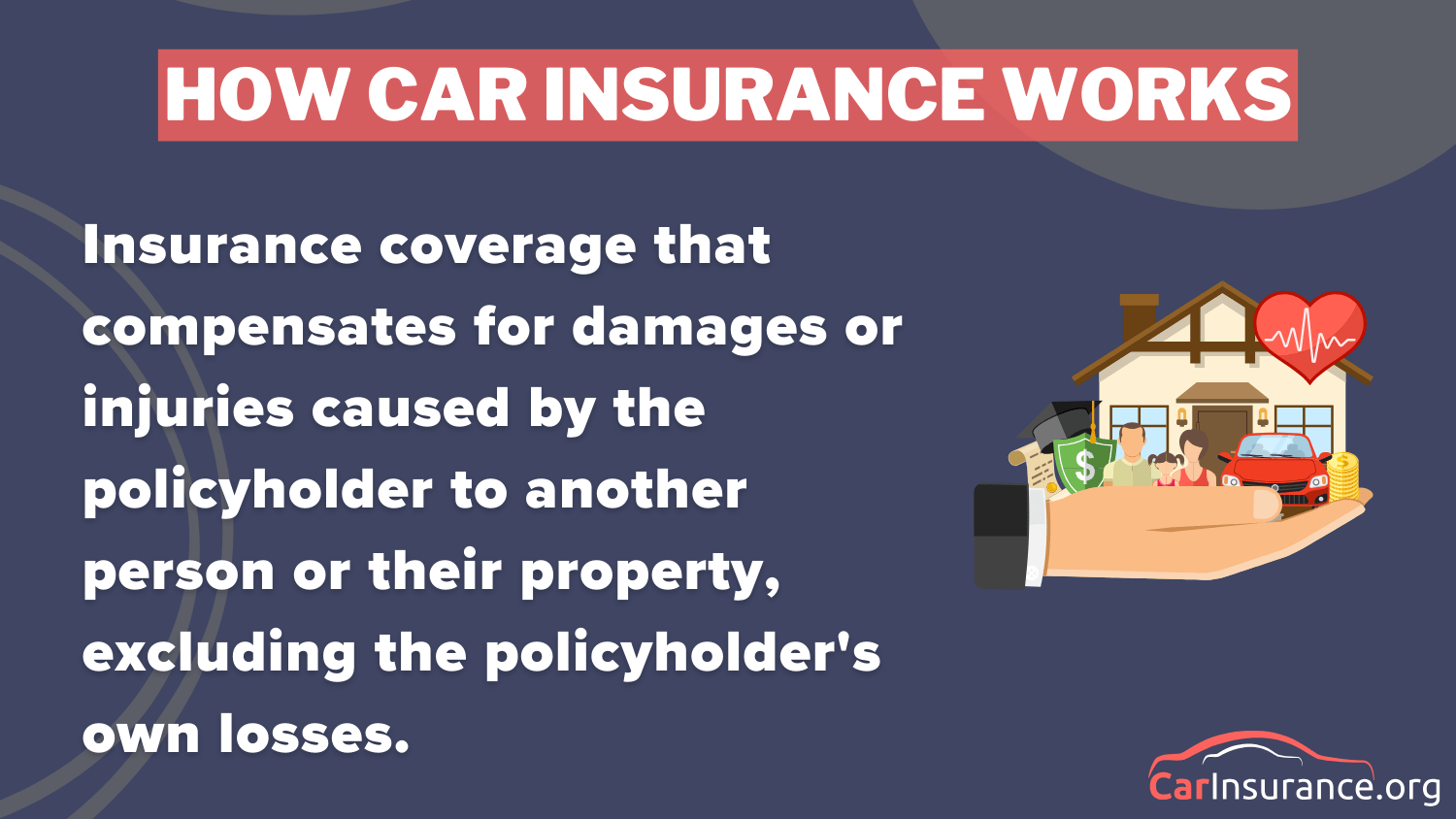

Understanding how car insurance works is key for Hawaii drivers. Liability insurance covers damages and injuries you cause to others but not your own vehicle. Full coverage adds collision and comprehensive insurance, protecting against accidents and theft.

Hawaii Car Insurance Monthly Rates by Provider & Coverage Level

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $43 | $118 | |

| $30 | $82 | |

|

| $36 | $99 |

| $22 | $59 | |

| $47 | $128 | |

| $31 | $84 | |

|

| $29 | $78 |

| $23 | $64 | |

| $27 | $72 | |

| $16 | $44 |

Compare RatesStart Now →

Car insurance rates in Hawaii vary by provider. Minimum coverage ranges from $16 to $47 per month, while full coverage costs between $44 and $128. Comparing policies from different Hawaii car insurance companies helps you find the best coverage at an affordable price.

Consider service, claims experience, and discounts in addition to price. Discounts for policy bundling or safe driving are available from a number of Hawaii auto insurance companies. Because Hawaii is a no-fault jurisdiction, medical bills will be covered by your policy regardless of who is at blame.

Hawaii Car Insurance Discounts

In Hawaii, motorists can get discounts such as bundling policies, good student discounts, and safe driving discounts. Insurers like Allstate, Geico, and State Farm also have environmental-friendly discounts, which bring down the average car insurance costs in Hawaii.

Car Insurance Discounts From the Top Providers in Hawaii

| Insurance Company | Available Discounts |

|---|---|

| Multi-policy, early signing, new car, good student, safe driver, anti-theft devices | |

| Multi-vehicle, early bird, good student, safe driving, loyalty, generational | |

|

| Multi-vehicle, good driver, alternative energy, good student, home and auto bundling |

| Multi-policy, safe driver, vehicle equipment, military, good student, emergency deployment | |

| Bundling, right track (telematics), low-mileage driver, newly married, good student | |

| Multi-policy, SmartRide (telematics), accident-free, good student, defensive driving | |

|

| Snapshot (telematics), multi-policy, continuous insurance, safe driver, home and auto bundling |

| Accident-free, defensive driving, good student, multi-line, safe vehicle | |

| Safe driver, bundling, hybrid/electric vehicle, new car replacement, home and auto bundling | |

| Military, good student, vehicle storage, safe driver, multi-vehicle |

Compare RatesStart Now →

Discounts for anti-theft equipment and car insurance with telematics programs also reduce rates further. USAA and State Farm give discounts as high as 25 percent, while the utilization of telematics gives as high as 18 percent, drastically reducing the price of car insurance.

Hawaii Auto Insurance Discounts

| Insurance Company | Anti-Theft | Bundling | Good Driver | Good Student | UBI |

|---|---|---|---|---|---|

| 10% | 25% | 20% | 10% | 15% | |

| 12% | 20% | 22% | 12% | 14% | |

|

| 10% | 22% | 21% | 10% | 16% |

| 15% | 15% | 22% | 12% | 18% | |

| 10% | 20% | 20% | 10% | 15% | |

| 12% | 20% | 22% | 12% | 14% | |

|

| 12% | 20% | 21% | 10% | 16% |

| 15% | 25% | 20% | 12% | 17% | |

| 10% | 20% | 20% | 8% | 13% | |

| 15% | 25% | 25% | 12% | 18% |

Compare RatesStart Now →

When selecting car insurance in Hawaii, look at discounts you are eligible for, including good student, military, or telematics-based discounts. These choices can assist in lowering the average car insurance costs in Hawaii so that you get a policy that suits you.

Hawaii Car Insurance Accident and Claims

In Hawaii, car accidents & claims are common, with collision claims making up 30% of all claims, costing around $3,500. This impacts overall car insurance rates in Hawaii.

5 Most Common Auto Insurance Claims in Hawaii

| Claim Type | Portion of Claims (%) | Cost per Claim ($) |

|---|---|---|

| Collision | 30% | $3,500 |

| Comprehensive | 25% | $2,800 |

| Uninsured Motorist | 20% | $4,200 |

| Bodily Injury | 15% | $15,000 |

| Property Damage | 10% | $5,000 |

Compare RatesStart Now →

Comprehensive claims follow at 25%, with an average cost of $2,800. Uninsured motorist claims make up 20% and tend to be more expensive, averaging $4,200 per claim.

15% of total claims are for physical injuries, and they generally cost $15,000. Ten percent of claims are for property damage, and they generally cost $5,000 each.

Hawaii Accidents & Claims per Year by City

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Hilo | 2,500 | 2,000 |

| Honolulu | 10,000 | 8,000 |

| Kahului | 1,500 | 1,200 |

| Kailua | 3,000 | 2,500 |

| Kapolei | 2,000 | 1,800 |

Compare RatesStart Now →

Honolulu has the most accidents in Hawaii, with 10,000 per year. This accounts for 8,000 claims, which has a huge impact on auto insurance costs in Hawaii in urban areas.

Hilo, on the other hand, experiences 2,500 accidents annually and 2,000 claims. Smaller cities experience fewer accidents, which affects the car insurance premiums in Hawaii drivers pay.

Hawaii Fatal Accidents

| Category | Count |

|---|---|

| Fatal accident count | 120 |

| Vehicles involved in fatal crashes | 180 |

| Fatal crashes involving drunk persons | 40 |

| Fatalities | 130 |

| Persons involved in fatal crashes | 200 |

Compare RatesStart Now →

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Minimum Car Insurance Coverage Requirements in Hawaii

Hawaii mandates that all drivers carry a minimum of $20,000 bodily injury coverage per person for injuries. When more than one person is injured, you must carry $40,000 total bodily injury coverage.

Along with physical injury, Hawaii requires $10,000 in personal injury protection (PIP) to pay for your own medical bills and lost wages and $10,000 in property damage liability, which pays for damage to other people’s property.

Geico excels with a streamlined claims process and personalized service, helping drivers easily navigate Hawaii's unique insurance requirements and coverage needs.Jeff Root Licensed Insurance Agent

While these minimums offer basic protection, they may not cover all costs in a serious accident. The average car insurance cost in Hawaii reflects the need for higher coverage to avoid paying out-of-pocket for expenses exceeding the minimum limits.

Factors Affecting Monthly Car Insurance Rates in Hawaii

Demographics can make a big difference in your car insurance rates by state. Your age, gender, ZIP code, and city, specifically, can influence the cost of your policy. Read the information below to learn more about how it influences your expenses.

Hawaii Auto Insurance Monthly Rates by Provider, Age, & Gender

| Insurance Company | Age: 17 Female | Age: 17 Male | Age: 25 Female | Age: 25 Male | Age: 35 Female | Age: 35 Male | Age: 60 Female | Age: 60 Male |

|---|---|---|---|---|---|---|---|---|

| $250 | $270 | $150 | $170 | $120 | $130 | $110 | $120 | |

| $240 | $260 | $145 | $165 | $115 | $125 | $105 | $115 | |

|

| $245 | $265 | $148 | $168 | $118 | $128 | $108 | $118 |

| $200 | $220 | $130 | $150 | $95 | $105 | $85 | $95 | |

| $260 | $280 | $155 | $175 | $125 | $135 | $115 | $125 | |

| $230 | $250 | $140 | $160 | $110 | $120 | $100 | $110 | |

|

| $220 | $240 | $135 | $155 | $100 | $110 | $90 | $100 |

| $210 | $230 | $130 | $150 | $90 | $100 | $80 | $90 | |

| $235 | $255 | $140 | $160 | $110 | $120 | $100 | $110 | |

| $195 | $215 | $125 | $145 | $85 | $95 | $75 | $85 |

Compare RatesStart Now →

A few insurers raise their premium moderately for one driver (17 and 25-year-olds), like Farmers Ins HI Standard. Others charge the same premium to everyone, like Allstate, Geico Govt Employees, and State Farm Mutual Auto.

Hawaii Auto Insurance by ZIP Code

| ZIP Code | Rates |

|---|---|

| 96701 | $120 |

| 96703 | $96 |

| 96706 | $110 |

| 96720 | $115 |

| 96740 | $125 |

| 96744 | $118 |

| 96746 | $105 |

| 96753 | $130 |

| 96760 | $112 |

| 96817 | $140 |

Compare RatesStart Now →

Keep in mind that you can save a lot of money by inquiring about auto insurance discounts. This is particularly useful if you have a teenager on your policy.

Hawaii Auto Insurance Monthly Rates by Vehicle & Coverage Level

| Make & Model | Minimum Coverage | Full Coverage |

|---|---|---|

| 2024 Buick Envision | $115 | $180 |

| 2024 Chevrolet Trailblazer | $110 | $170 |

| 2024 Ford Bronco Sport | $120 | $190 |

| 2024 Honda Passport | $125 | $200 |

| 2024 Hyundai Venue | $105 | $160 |

| 2024 Kia Soul | $100 | $155 |

| 2024 Mazda CX-5 | $115 | $175 |

| 2024 Nissan Kicks | $110 | $165 |

| 2024 Subaru Crosstrek | $115 | $180 |

| 2024 Toyota Corolla Cross | $105 | $160 |

Compare RatesStart Now →

Most major insurers offer bundling discounts if you choose to buy an auto policy along with a life insurance or homeowners insurance policy.

How to Find the Best Car Insurance in Hawaii

Getting the appropriate car insurance in Hawaii can be overwhelming, but it is important to cover yourself and your vehicle in the event of an accident or unexpected situations.

To help you navigate the process, we’ve outlined a straightforward 5-step guide to securing the best car insurance policy in Hawaii.

- Compare Rates: Compare rates and shop around for the lowest, with options such as Geico Insurance in Hawaii, which provides cheap policies.

- Consider Coverage Options: Select coverage that suits your needs, with Geico for basic coverage and Allstate for extensive plans.

- Look for the Best Discounts: Inquire about discounts. Allstate and Geico Insurance in Hawaii provide discounts for safe driving and bundling.

- Understand Claims and Customer Service: Verify the provider’s customer service and claims handling reputation.

- Evaluate Additional Benefits: Look for extra perks, like roadside assistance, with Allstate roadside assistance review highlighting useful services.

By comparing rates, coverage, discounts, and customer service, you can get the best car insurance in Hawaii. Whether you choose Geico or Allstate, this guide will help you get the right policy.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Top Car Insurance Providers in Hawaii

Find the best car insurance in Hawaii and compare rates from industry leaders like Geico, State Farm, and Allstate. Geico is one of the 10 cheapest car insurance companies, with premiums beginning at $16 per month.

For individuals seeking cheap Hawaii auto insurance, these companies also have multiple discounts, including safe-driver rewards and bundling, which enable you to save money while still having solid coverage.

Ready to find cheaper car insurance coverage? Enter your ZIP code to begin.

Frequently Asked Questions

Why Geico, State Farm, and Allstate are the best car insurance companies in Hawaii?

They offer affordable rates, great customer service, and comprehensive coverage options in Hawaii cheap car insurance. Look at the factors that affect the price of car insurance.

What are the minimum coverage levels for auto insurance in Hawaii?

Hawaii mandates bodily injury liability, property damage liability, and personal injury protection to secure financial stability following accidents. Ready to find affordable car insurance? Use our free comparison tool to get started.

Why is USAA the best choice for military families?

USAA offers lower rates and specialized coverage for military families, but eligibility is limited to military members and their families.

What other coverage options are available to Hawaii drivers?

MedPay and uninsured/underinsured motorist coverage offer extra protection for medical and accident costs. To gain a deeper insight, dive into how the states rank on uninsured drivers.

How does combining insurance policies save policyholders money?

Bundling policies can lead to multi-policy discounts, reducing overall insurance costs.

What are the advantages and disadvantages of using a local insurance agency over a direct supplier?

Local agents offer personalized service, while direct providers like Geico offer lower rates and convenience.

Which insurance companies in Hawaii provide the highest discounts?

Top insurers offer discounts for bundling, safe driving, and military service, among others. Explore our safe driving tips: How to keep your insurance and car safe for more insights.

Why is Hawaii’s legal minimum coverage frequently insufficient?

Minimum coverage may not cover high medical and repair costs, so additional coverage is recommended.

How do A.M. Best ratings and complaint levels affect insurance company rankings?

Ratings and complaint levels reflect financial stability and service quality, influencing provider rankings.

Why is USAA the best choice for military families, and are there particular eligibility requirements?

USAA offers lower rates and specialized coverage for military families, but eligibility is limited to military members and their families. See if you’re getting the best deal on car insurance by entering your ZIP code here.

How do demographic characteristics affect car insurance premiums in Hawaii?

Related Articles

-

Apr 2025

Best Car Insurance in Wisconsin for 2026 [Check Out the Top 10 Companies]

-

Mar 2025

Best Car Insurance in Delaware for 2026 [Check Out the Top 10 Companies]

-

Feb 2025

Best Car Insurance in Vermont for 2026 [Your Guide to the Top 10 Companies]

-

Apr 2025

Best Car Insurance in Arkansas for 2026 [Review the Top 10 Companies Here]

-

Apr 2025

Best Car Insurance in Georgia for 2026 [Review the Top 10 Companies Here]

-

Mar 2025

Best Car Insurance in Indiana for 2026 [Check Out the Top 10 Companies]

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.