Best Car Insurance in Vermont for 2026 [Your Guide to the Top 10 Companies]

Progressive, Allstate, and Liberty Mutual offer the best car insurance in Vermont, with rates starting at $12/mo. Progressive stands out for its technology integration and 10% bundling discount. Allstate has a renowned accident forgiveness program while Liberty Mutual has customizable discounts of up to 30%.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Insurance Feature Writer

Rachel Bodine graduated from college with a BA in English. She has since worked as a Feature Writer in the insurance industry and gained a deep knowledge of state and countrywide insurance laws and rates. Her research and writing focus on helping readers understand their insurance coverage and how to find savings. Her expert advice on insurance has been featured on sites like PhotoEnforced, All...

Rachel Bodine

Licensed Insurance Agent

Daniel Walker graduated with a BS in Administrative Management in 2005 and has run his family’s insurance agency, FCI Agency, for over 15 years (BBB A+). He is licensed as an insurance agent to write property and casualty insurance, including home, life, auto, umbrella, and dwelling fire insurance. He’s also been featured on sites like Reviews.com and Safeco. To ensure our content is accura...

Daniel Walker

Updated February 2025

13,285 reviewsCompany Facts

Full Coverage in Vermont

A.M. Best Rating

Complaint Level

Pros & Cons

13,285 reviews11,640 reviewsCompany Facts

Full Coverage in Vermont

A.M. Best Rating

Complaint Level

Pros & Cons

11,640 reviews 3,792 reviews

3,792 reviewsCompany Facts

Full Coverage in Vermont

A.M. Best Rating

Complaint Level

Pros & Cons

3,792 reviewsProgressive, Allstate, and Liberty Mutual offer the best car insurance in Vermont.

Progressive is the top overall for its budget-friendly rates of $58 a month and wide coverage options. Allstate offers competitive discounts like 40% off with the Drivewise program. Lastly, Liberty Mutual is known for its customizable policies to fit your unique needs.

As you read this Vermont auto insurance guide, you’ll learn about the car insurance coverage rates and options in Vermont and all the in-between. So, let’s start off with the top 10 car insurance companies in Vermont.

Our Top 10 Company Picks: Best Car Insurance in Vermont

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 10% | A+ | Technology Integration | Progressive |

| #2 | 25% | A+ | Comprehensive Coverage | Allstate | |

| #3 | 25% | A | Customizable Policies | Liberty Mutual | |

| #4 | 20% | A | Customer Satisfaction | Farmers |

| #5 | 13% | A++ | Innovative Discounts | Travelers | |

| #6 | 17% | B | Wide Availability | State Farm | |

| #7 | 20% | A+ | Strong Financials | Nationwide | |

| #8 | 25% | A | Family Focus | American Family | |

| #9 | 10% | A++ | Military Focus | USAA | |

| #10 | 25% | A++ | Competitive Pricing | Geico |

You can get car insurance quotes in Vermont today by simply entering your ZIP code.

- Progressive offers gap insurance and accident forgiveness

- Bundling discount generally saves 10% to 25% on premiums

- Full coverage car insurance rates range from $38 to $181 monthly

#1 – Progressive: Top Overall Pick

Pros

- Robust Coverage Options & Customer Support: Progressive offers a range of coverage options, such as gap insurance and accident forgiveness and 24/7 claims service.

- Affordable Rates & Discounts: Progressive’s car insurance review helps VT drivers learn how to get competitive rates and discounts, including safe driver and multi-policy of 10%.

- Convenient Online Tools & Mobile App: Progressive’s mobile app and website make it easy for drivers to manage policies, obtain quotes, and submit claims.

Cons

- High Penalties for Risky Profiles: Compared to other insurers, drivers with accidents, DUIs, or bad credit may pay far higher premiums.

- Service Hiccups and Delays: In urgent situations, clients may find it upsetting to receive inconsistent service and slower-than-expected claims processing.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#2 – Allstate: Best for Comprehensive Coverage

Pros

- Generous Discounts: According to our Allstate car insurance review, it offers a 25% bundling discount and up to 40% off when using its Drivewise program.

- Reliable Accident Forgiveness: Drivers save money over time by guaranteeing that their rates won’t increase after their first at-fault collision.

- New Automobile Replacement Coverage: If the car is totaled in an accident and is two years old or younger, it can be replaced with a brand-new car of the same make and model.

Cons

- Higher Premiums Than Competitors: Allstate’s average monthly premium for full coverage is $142, which is more than the state average of about $100.

- Below-Average Customer Satisfaction: Power’s 815/1,000 customer satisfaction rating is behind those of its competitors.

#3 – Liberty Mutual: Best for Customizable Policies

Pros

- Customizable Discounts: Liberty Mutual provides discounts such as 10% off when buying a policy online, 25% bundle savings, and up to 30% off when using RightTrack.

- Accident Forgiveness: According to our Liberty Mutual car insurance review, drivers can avoid unexpected rate increases after the first at-fault collision.

- Better Car Replacement: Liberty Mutual will replace your automobile with a newer model, not merely one from the same year, and make it if it is totaled and less than a year old.

Cons

- Higher-Than-Average Premiums: Minimum and full coverage ranges from $42 to $100 per month.

- Lower Customer Satisfaction: Liberty Mutual has Power’s customer satisfaction rating of 805/1,000 is worse than that of many of its top competitors.

#4 – Farmers: Best for Customer Satisfaction

Pros

- Generous Savings Opportunities: Farmers offer various savings, including up to 20% for bundling insurance and up to 20% for safe drivers through the Signal program.

- New Car Replacement: If your car is less than two years old and totaled, Farmers will replace it with a brand-new vehicle of the same make and model.

- Great Customer Satisfaction: Farmers car insurance reviews show it has a J.D. Power score of 816/1,000, reflecting positive claims handling and customer service experience.

Cons

- Above-Average Insurance Costs: Farmers’ monthly premiums can range from $33 to $103, more than the state average of about $100.

- Limited Customization Options: Farmers provide less flexible coverage add-ons than some competitors, which might not satisfy drivers seeking highly customized insurance.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#5 – Travelers: Best for Innovative Discounts

Pros

- Innovative Discounts: Travelers offers up to 30% savings through its IntelliDrive program for safe driving and up to 23% off when combining home and auto insurance.

- Strong Financial Stability: Travelers has an A++ rating from A.M. Best, making it the most financially stable insurer. It guarantees claims payments.

- Intensive Customizable Coverage: Our Travelers car insurance review covers a variety of coverages, including gap, rideshare, and accident forgiveness coverage.

Cons

- Additional Costs for Some Drivers: The monthly premiums for Travelers policies can range from $24 to $75.

- Limited Local Agent Availability: Travelers have fewer local agents in Vermont than some of its competitors.

#6 – State Farm: Best for Wide Availability

Pros

- Reasonable Pricing: As per our State Farm car insurance review, full coverage plans cost $87 monthly.

- Wide Availability: State Farm operates in all 50 states, including Vermont, and has a huge network of local agents for in-person assistance.

- Huge Savings: The Drive Safe & Save program allows drivers to save up to 25% on their premiums.

Cons

- Higher Costs for High-Risk Drivers: Drivers with accidents may see premiums increase over time.

- Limited Policy Customization: Other big insurers offer specific add-ons that State Farm does not, such as gap insurance or new car replacement.

#7 – Nationwide: Best for Financial Stability

Pros

- Cost-Effective Premiums: Nationwide has competitive rates, with comprehensive coverage costing around $120 monthly.

- Huge Discounts: Our Nationwide car insurance review highlights discounts of up to 40% with its SmartRide program for safe driving and up to 20% for bundling insurance.

- Strong Financial Stability: A.M. Best has given Nationwide an A+ rating, indicating its financial stability and consistent ability to pay claims.

Cons

- Increased Pricing for High-Risk Drivers: Drivers with a history of collisions may pay $130 to $160 monthly.

- Limited Local Agent Availability: Fewer local agents are available in VT, which may restrict access to in-person assistance and individualized care.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#8 – American Family: Best for Family Focus

Pros

- Family-Focused Coverage: Family-friendly plans include teen driver discounts, loyalty awards, and customized coverage options for homes with multiple cars.

- Competitive Pricing: The American Family car insurance review shows that it is a reasonable choice in Vermont, with full coverage policies costing $85 per month.

- Stable Discount Plans: Drivers can save up to 30% with the KnowYourDrive program for safe driving practices and up to 25% with bundling discounts.

Cons

- Selective Market Presence: It has a smaller local agent network than its competitors, such as State Farm and Geico, which can restrict in-person assistance.

- Expensive Premiums for Less-Than-Perfect Records: The monthly premiums for drivers with accidents or poor credit can reach $130 to $160, more than the state average of $100.

#9 – USAA: Best for Military Benefits

Pros

- Incredibly Low Rates: USAA car insurance reviews show that the company offers the lowest monthly premiums at just $14.

- Top-Rated Customer Satisfaction: Continuously ranks first for customer experience. The most significant power score is 884/1,000.

- Significant Savings: Members can save up to 10% when parking their vehicle on a military base and up to 30% when using USAA’s SafePilot telematics program.

Cons

- Restricted Eligibility: Many Vermont drivers are not eligible for USAA because it is only offered to active military personnel, veterans, and their families.

- Limited Physical Branches: USAA does not have many physical offices in VT, a drawback for people who prefer claims and policy administration in person.

#10 – Geico: Best for Competitive Pricing

Pros

- Reasonable Premiums: Geico’s car insurance review highlights its affordable options in Vermont due to its competitive rates, which average between $12 and $38 per month.

- Comprehensive Windshield Coverage: Simple glass repair services with no out-of-pocket expenses and a waiver of the deductible for windshield repairs.

- Huge Savings: Through the DriveEasy safe driving program, drivers can save up to 40%, and with multi-policy bundling, up to 25%.

Cons

- Limited Support for Local Agents: Geico mainly does business online and over the phone. The company has very few physical offices in Vermont.

- Increased Rates for High-Risk Drivers: Premiums for drivers with accidents, DUIs, or bad credit may rise to $140 to $170 monthly, higher than the state average.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Factors That Affect the Best Car Insurance Rates in Vermont

Your age and gender can determine what you pay for car insurance. We’ve collected some Vermont car insurance coverage data and compared it by age, gender, and marital status.

Young, single males pay much more than males who are 35 years old and married. Females pay lower coverage rates. Married males and females pay the same rates at some companies.

Car Insurance Monthly Rates in Vermont by Provider, Age, & Gender

| Insurance Company | Age: 17 Female | Age: 17 Male | Age: 25 Female | Age: 25 Male | Age: 35 Female | Age: 35 Male | Age: 60 Female | Age: 60 Male |

|---|---|---|---|---|---|---|---|---|

| $430 | $567 | $204 | $224 | $180 | $180 | $171 | $171 | |

| $390 | $530 | $195 | $215 | $170 | $175 | $160 | $165 | |

|

| $420 | $560 | $220 | $240 | $190 | $200 | $180 | $190 |

| $321 | $374 | $118 | $116 | $140 | $131 | $138 | $126 | |

| $670 | $745 | $181 | $192 | $158 | $171 | $140 | $157 | |

| $293 | $373 | $138 | $149 | $121 | $123 | $108 | $114 | |

|

| $869 | $951 | $287 | $306 | $281 | $279 | $252 | $253 |

| $670 | $861 | $253 | $281 | $227 | $227 | $202 | $202 | |

| $390 | $530 | $195 | $215 | $170 | $175 | $160 | $165 | |

| $309 | $323 | $131 | $136 | $95 | $96 | $89 | $89 |

The higher the rates, the younger the driver. This is because younger drivers have less experience and are prone to risks. The table below contains all the other factors that impact your premium cost.

Car Insurance Factors Affecting Rates in Vermont

| Factor | Explanation |

|---|---|

| Age | Younger and older drivers face higher rates. |

| Gender | Males generally pay higher rates. |

| Driving Record | Clean records result in lower rates. |

| Vehicle Type | Luxury and sports cars have higher premiums. |

| Location | Urban areas have higher rates than rural ones. |

| Credit Score | Poor credit can lead to higher premiums. |

| Coverage Level | More coverage increases premiums. |

| Deductible Amount | Higher deductible lowers premiums. |

| Claims History | Frequent claims raise premiums. |

| Marital Status | Married drivers often pay less. |

Check this guide for more details about the factors that affect your car insurance rates.

Best Auto Insurance Companies in Vermont

You can definitely choose from different types of Vermont car insurance coverage. Check out the table below.

Car Insurance Monthly Rates in Vermont by Coverage Type

| Coverage | Vermont | U.S. Average |

|---|---|---|

| Liability | $28 | $43 |

| Collision | $23 | $25 |

| Comprehensive | $10 | $12 |

| Combined (Full) | $62 | $80 |

Vermont motorists can add collision and comprehensive to their policy, but it would increase the monthly premium. Compared to the national average, Vermont’s annual car insurance rates are almost $100 cheaper.

Collision covers damage from accidents, while comprehensive protects against non-collision situations. For complete protection, you must carry both.Michael Leotta Insurance Operations Specialist

The following table shows the best car insurance rates in Vermont. The state assigns grades to many aspects that affect insurance prices. Traffic density has the lowest rating (C), while Vermont has a high vehicle theft rate (A), moderate risks of weather-related mishaps (B), average claim size (B+), and uninsured drivers (C+).

Vermont Report Card: Auto Insurance Premiums

| Category | Grade | Explanation |

|---|---|---|

| Vehicle Theft Rate | A | Vermont has a relatively low vehicle theft rate compared to national averages, making it a safer place for vehicle owners. |

| Average Claim Size | B+ | Vermont sees moderate average claim sizes, primarily driven by weather-related incidents and collisions. |

| Weather-Related Risk | B | Vermont experiences moderate weather-related risks, with snow and ice impacting driving conditions in winter months. |

| Uninsured Drivers Rate | C+ | While lower than the national average, Vermont has a noticeable number of uninsured drivers on the road. |

| Traffic Density | C | Traffic density is lower compared to larger states, but congestion can be high in cities like Burlington. |

If you want to cover all your bases, opt for full coverage.

Minimum Coverage Requirements in Vermont

Understanding what coverage you need can be confusing, given all the car insurance companies you need to consider, but this guide will narrow down the essentials so you get what truly is best for you.

Check the table for car insurance monthly rates by coverage level and provider.

Car Insurance Monthly Rates in Vermont by Provider & Coverage Level

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $46 | $142 | |

| $27 | $85 | |

|

| $33 | $103 |

| $12 | $38 | |

| $32 | $100 | |

| $25 | $77 | |

|

| $58 | $181 |

| $28 | $87 | |

| $24 | $75 | |

| $14 | $42 |

Of course, as a consumer, you have always wanted to lower your bills and save. We have prepared a list of car insurance discounts in Vermont that you can take advantage of while still getting nothing less.

Car Insurance Discounts From the Top Providers in Vermont

| Insurance Company | Available Discounts |

|---|---|

| Multi-Policy Discount, Safe Driver Discount, Anti-Theft Device Discount, New Car Discount | |

| Multi-Policy Discount, Safe Driver Discount, Defensive Driving Course Discount, Good Student Discount | |

|

| Multi-Policy Discount, Safe Driver Discount, Good Student Discount, Alternative Fuel Discount |

| Multi-Policy Discount, Defensive Driving Discount, Good Student Discount, Military Discount | |

| Multi-Policy Discount, Good Student Discount, Anti-Theft Device Discount, New Car Discount | |

| Multi-Policy Discount, Safe Driver Discount, Accident-Free Discount, Defensive Driving Discount | |

|

| Multi-Policy Discount, Snapshot Discount, Good Student Discount, Homeowner Discount |

| Multi-Policy Discount, Safe Driver Discount, Defensive Driving Discount, Good Student Discount | |

| Multi-Policy Discount, Safe Driver Discount, Hybrid/Electric Vehicle Discount, New Car Discount | |

| Multi-Policy Discount, Safe Driver Discount, Good Student Discount, Military Discount |

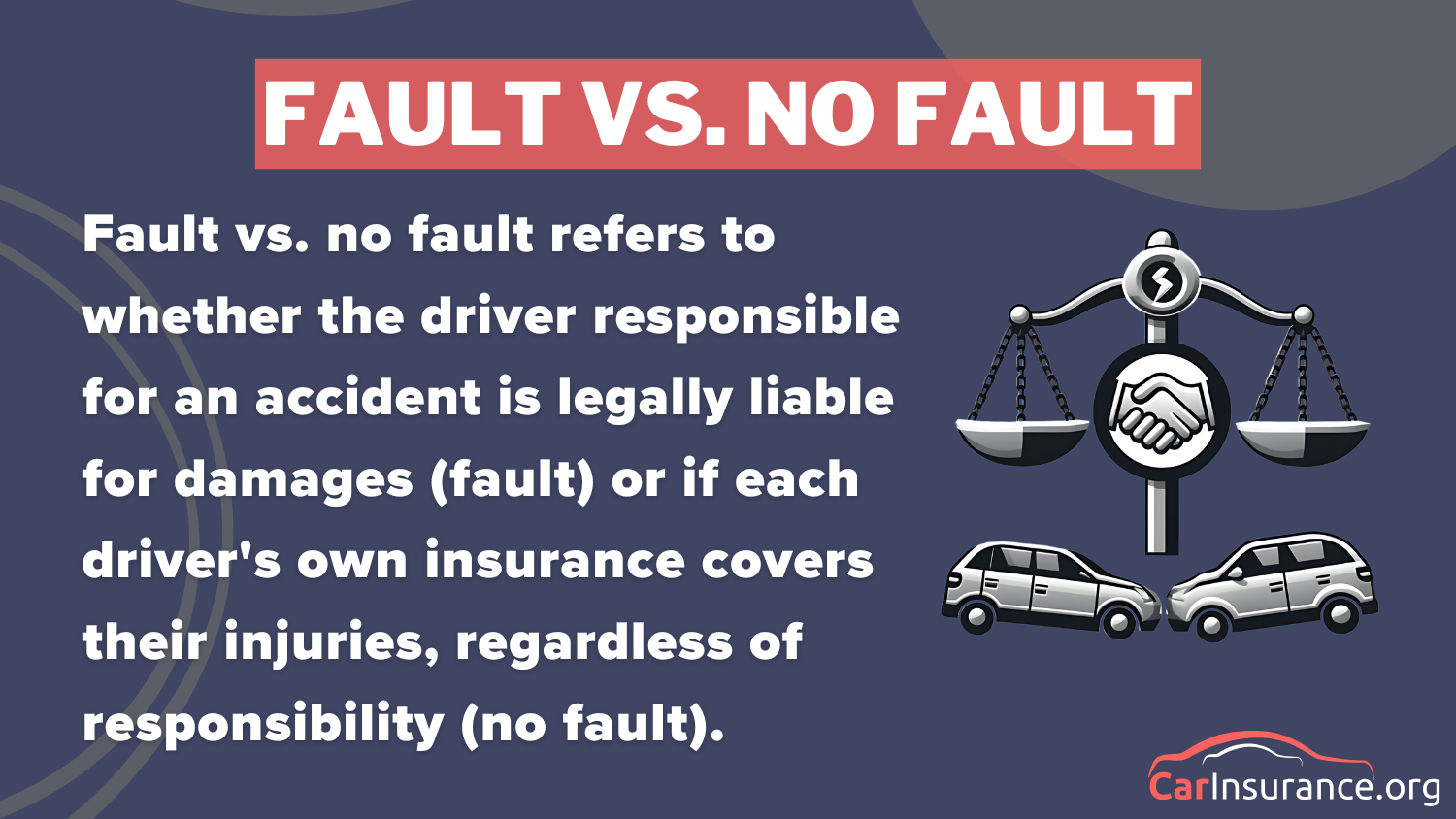

Vermont is an at-fault state. But what does at-fault mean?

According to Vermont’s modified comparative negligence rule, drivers are only entitled to compensation if they bear less than 51% of the blame for the collision.

To prepare yourself for unpredicted risks on the roads, ensure that you get coverage that does not just cover the minimum liability so your pocket won’t run dry. Here is the number of accidents that occur in a year in Vermont and the claim filed to the insurers.

Annual Accidents & Claims in Vermont by City

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Barre | 520 | 470 |

| Bennington | 490 | $450 |

| Brattleboro | 540 | $500 |

| Burlington | 1,250 | 1,100 |

| Essex | 700 | $650 |

| Middlebury | 370 | $330 |

| Montpelier | 430 | 390 |

| Rutland | 780 | 710 |

| South Burlington | 880 | $810 |

| St. Albans | 610 | $570 |

If you think getting more than the minimum could cost you so much, leave those worries. There are more ways to lower those rates and save while ensuring your future.

Car Insurance Discounts in Vermont

| Insurance Company | Anti-Theft | Bundling | Good Driver | Good Student | UBI |

|---|---|---|---|---|---|

| 15% | 28% | 20% | 15% | 10% | |

| 10% | 25% | 10% | 15% | 20% | |

|

| 15% | 25% | 10% | 15% | 10% |

| 23% | 22% | 22% | 15% | 10% | |

| 15% | 29% | 10% | 15% | 30% | |

| 10% | 20% | 10% | 15% | 10% | |

|

| 10% | 20% | 10% | 15% | 30% |

| 15% | 17% | 15% | 25% | 30% | |

| 10% | 15% | 10% | 15% | 20% | |

| 20% | 10% | 30% | 15% | 15% |

If you are eligible, you can take advantage of any of those or even more. One good way to save while guaranteeing your safety is through a 10-30% discount on your premium for safe driving, affording you cheap car insurance in Vermont.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Ratings of the Best Car Insurance Companies in Vermont

Through its study of financial ratings, A.M. Best is one way of determining the best car insurance companies in Vermont. We’ve compiled some ratings for some popular car insurance companies you may find in your area.

Car Insurance A.M. Best Financial Rankings in Vermont

| Insurance Company | AM Best | Direct Premiums Written | Market Share | Loss Ratio |

|---|---|---|---|---|

| A+ | $998,919 | 11.42% | 55.64% | |

| A+ | $1,153,856 | 13.19% | 64.93% | |

|

| A | $192,162 | 2.20% | 74.14% |

| A++ | $706,897 | 8.08% | 74.24% | |

| A | $424,106 | 4.85% | 61.06% | |

| A+ | $786,109 | 8.99% | 59.96% | |

|

| A+ | $875,579 | 10.01% | 58.55% |

| B | $1,779,915 | 20.35% | 63.70% | |

| A++ | $335,963 | 3.84% | 62.41% | |

| A++ | $299,488 | 3.42% | 72.05% |

Investopedia writer Adam Hayes states, “Market share represents the percentage of an industry, or a market’s total sales, that is earned by a particular company over a specified time.”

Market share is calculated by taking a company’s sales over time and dividing them by the industry’s total sales.

The role is to identify the top insurance companies. A company with a grade A shows strong financial standing, representing a company that guarantees consumer policies and keeps them secure. Most of the ratings in the table are grade A.

Let’s look at some more ratings. These ratings are from J.D. Power’s Customer Overall Satisfaction Study.

J.D. Power Overall Customer Satisfaction Index Ranking – New England Region

| Company name | Points (based on a 1,000-point scale) | Circle Ratings |

|---|---|---|

| 834 | 4 | |

| 879 | 5 | |

| 800 | 2 | |

| 827 | 3 | |

| 809 | 3 | |

| 811 | 3 | |

| 803 | 2 |

| 817 | 3 | |

| 804 | 2 | |

|

| 826 | 3 |

| 796 | 2 | |

| 813 | 3 | |

| 838 | 4 | |

| 795 | 2 | |

| 804 | 2 | |

| 893 | 5 | |

| 821 | 3 |

The ratings and scores are J.D. Power’s rating standards. These standards measure consumers’ or policyholders’ satisfaction with car insurance companies in their region.

How to Get the Cheapest Auto Insurance in Vermont

Shopping for cheap car insurance in Vermont while ensuring that service quality is not compromised is necessary. The table below lists some companies offering lower rates and quality that may fit your budget.

Car Insurance Monthly Rates in Vermont by Provider vs. U.S. Average

| Insurance Company | Monthly Rates | U.S. Average | Compared to U.S. Average by % |

|---|---|---|---|

| $320 | $290 | 10.34% | |

| $280 | $290 | -3.45% | |

|

| $300 | $290 | 3.45% |

| $250 | $290 | -13.79% | |

| $400 | $290 | 37.93% | |

| $270 | $290 | -6.90% | |

|

| $550 | $290 | 89.66% |

| $370 | $290 | 27.59% | |

| $300 | $290 | 3.45% | |

| $280 | $290 | -3.45% |

This comparison of monthly rates for car insurance from different companies to the $290 average for the United States. While Liberty Mutual and Progressive have far higher rates, Progressive is the most expensive at $550 per month, and Geico and Nationwide have prices that are below average.

Ultimately, the best choice for you as a motorist is a coverage rate that meets your budget and your motor vehicle needs. The most expensive auto insurance policy may not be in your best interest. However, policies like full coverage will help should you get into a car accident.

Do you need a second look at the best car insurance in Vermont car coverage rates? Enter your ZIP code in the free quote box below to get quick results.

Frequently Asked Questions

How much is car insurance in Vermont?

The average cost of car insurance in Vermont for full-coverage auto insurance is about $67. The average monthly cost for minimal liability coverage is about $26. Enter your ZIP code to compare car insurance quotes in Vermont.

What is Vermont’s car tax rate?

Vermont’s sales tax is 6% of the car’s purchase price. Depending on the car type, other costs, such as title and registration fees, can also apply.

What is the penalty for driving without registration in Vermont?

Operating a car without a legal registration is a traffic infraction in Vermont. The punishment for this infraction is a civil fine of up to $500. Check these safe driving tips to be guided.

Who needs SR-22 insurance in Vermont?

Drivers with major infractions, such as DUIs, reckless driving, driving without insurance, or numerous convictions, must have SR-22 insurance in Vermont. It is evidence of minimal coverage and is usually needed for three years; if not maintained, the license may be suspended.

Is Vermont a no-fault state?

To be clear, Vermont is not a no-fault state. In Vermont, drivers must have liability insurance; the at-fault motorist is usually liable for the damages in an accident. However, Vermont has a “modified comparative negligence” law, which means that if both parties are at fault, the amount of compensation may be lowered by the extent of responsibility.

Do you need car insurance in Vermont?

Yes, the minimum car insurance coverage in Vermont is 25/50/10 per person, per accident, and per property damage, respectively.

Does Geico cover Vermont?

Yes, Vermont is covered by Geico. They provide state residents with auto insurance policies.

Does AAA cover Vermont?

Indeed, AAA offers coverage in Vermont, providing citizens with auto insurance and other services.

What is the most popular car brand in Vermont?

Toyota, Ford, Subaru, Chevrolet, and Honda are the most well-known automakers in Vermont. To be more precise, the most popular car in the U.S. is the Toyota RAV4. The Ram 1500/2500/3500, Subaru Crosstrek, Toyota Tacoma, and Ford F-Series are other well-liked vehicles.

What is the average cost of auto insurance in Vermont?

In Vermont, full-coverage auto insurance typically costs between $1,200 and $1,400 annually. However, several variables, including age, driving record, and the type of coverage, might affect rates.

Related Articles

-

May 2025

Best Car Insurance in Montana for 2026 [MT Top 10 Company Ranking]

-

Apr 2025

Best Car Insurance in Wisconsin for 2026 [Check Out the Top 10 Companies]

-

Mar 2025

Best Car Insurance in Kentucky for 2026 [Find the Top 10 Companies Here]

-

Apr 2025

Best Car Insurance in Georgia for 2026 [Review the Top 10 Companies Here]

-

May 2025

Best Car Insurance in Minnesota for 2026 [MN’s Top 10 Companies]

-

Mar 2025

Best Car Insurance in Indiana for 2026 [Check Out the Top 10 Companies]

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.