10 Cheap Car Insurance Companies That Only Look Back 3 Years in 2026 [Top Low-Cost Providers]

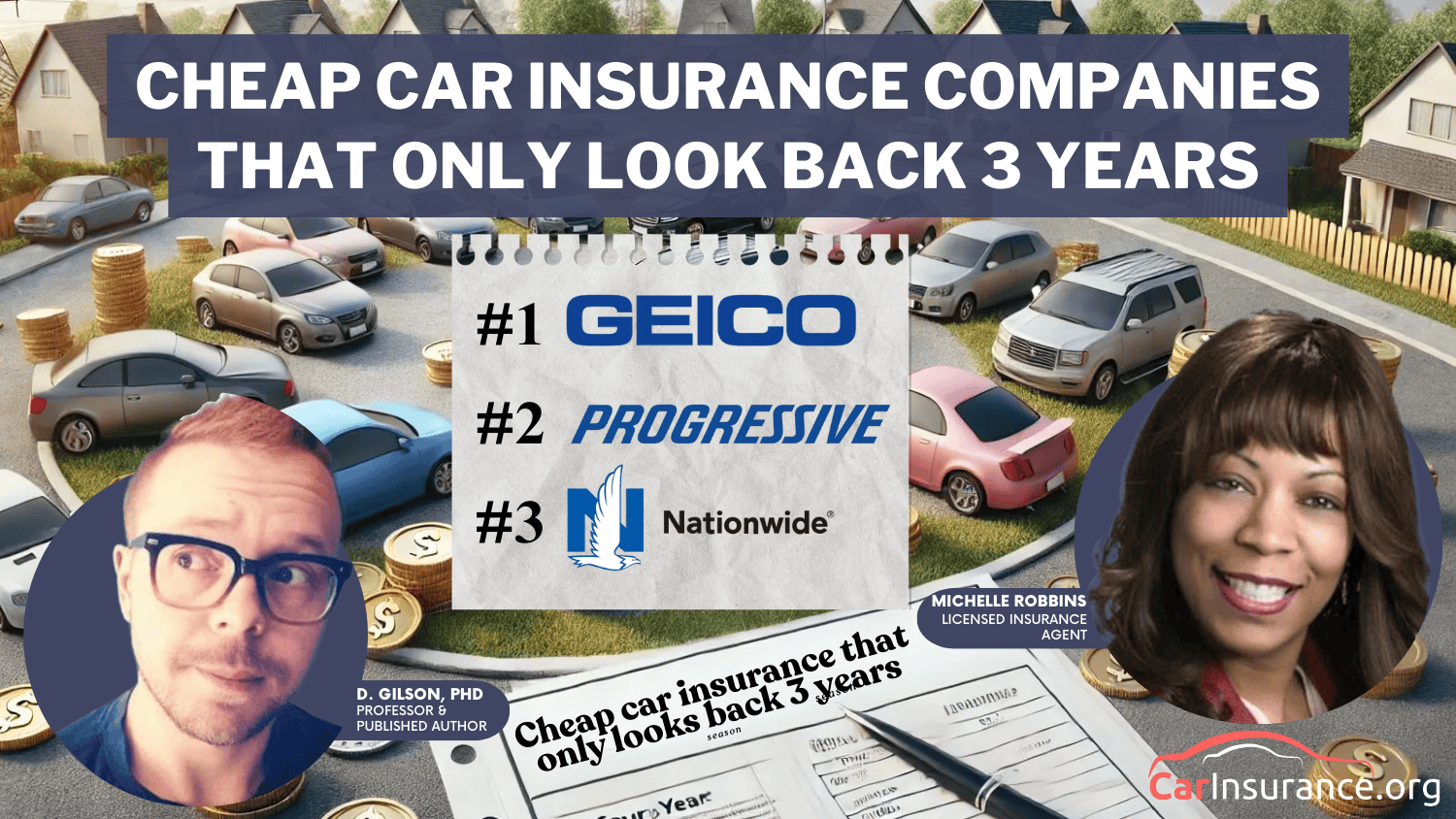

Geico, Progressive, and Nationwide are cheap car insurance companies that only look back 3 years. Geico is the top overall pick, with rates as low as $75/mo. Progressive is best for customizable coverage, while Nationwide stands out for its local focus. Discover how far back major providers look at your driving record.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Managing Editor

Laura Kuhl holds a Master’s Degree in Professional Writing from the University of North Carolina at Wilmington. Her career began in healthcare and wellness, creating lifestyle content for doctors, dentists, and other healthcare and holistic professionals. She curated news articles and insider interviews with investors and small business owners, leading to conversations with key players in the le...

Laura Kuhl

Licensed Insurance Agent

Eric Stauffer is an insurance agent and banker-turned-consumer advocate. His priority is educating individuals and families about the different types of insurance coverage. He is passionate about helping consumers find the best coverage for their budgets and personal needs. Eric is the CEO of C Street Media, a full-service marketing firm and the co-founder of ProperCents.com, a financial educat...

Eric Stauffer

Updated February 2025

13,285 reviews

13,285 reviewsCompany Facts

Min. Coverage 3-Year Look Back

A.M. Best Rating

Complaint Level

Pros & Cons

13,285 reviews3,071 reviewsCompany Facts

Min. Coverage 3-Year Look Back

A.M. Best Rating

Complaint Level

Pros & Cons

3,071 reviewsGeico, Progressive, and Nationwide are cheap car insurance companies that only look back 3 years,with monthly rates starting at $80. These companies focus on recent driving history, making them great for drivers with past incidents. If you need low-cost coverage without older accidents affecting your rate, these are the top choices.

Did you know some moving violations can remain on your driving record for more than five years? Don’t worry, we’re here to help.

Our Top 10 Picks: Cheap Car Insurance Companies That Only Look Back 3 Years

| Company | Rank | Monthly Rates | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | $75 | A++ | Affordable Premiums | Geico | |

| #2 | $80 | A+ | Customizable Coverage | Progressive |

| #3 | $85 | A+ | Local Focus | Nationwide | |

| #4 | $90 | B | Vanishing Deductible | Farm Bureau | |

| #5 | $95 | A | Strong Reputation | American Family | |

| #6 | $100 | A++ | Flexible Options | Travelers | |

| #7 | $105 | B | Accident Forgiveness | State Farm | |

| #8 | $110 | A | Diverse Discounts | Farmers |

| #9 | $115 | A | Customizable Policies | Liberty Mutual | |

| #10 | $120 | A+ | Comprehensive Coverage | Allstate |

Our car insurance guide explores which insurance companies look back three years and how to compare car insurance for high-risk drivers.

After learning everything about car insurance companies that only look back three years, enter your ZIP code to compare multiple insurance companies near you.

- Geico offers cheap car insurance rates starting at $75 per month

- Nationwide stands out with its local focus, offering tailored coverage options

- All three companies offer the cheapest car insurance with flexible policies

#1 – Geico: Top Overall Pick

Pros

- Affordable Rates: Geico is one the car insurance companies with a three-year look-back period, offering low rates at $75 a month.

- Top Choice: Geico offers cheap car insurance with minimal look-back. Learn all about it in our Geico Car Insurance Review.

- Easy Online Tools: Geico’s online tools make it simple to get quotes and manage your policy, helping you save even more.

Cons

- Limited Local Presence: Geico’s customer service may not be as personal as other companies that focus more on local needs.

- Fewer Coverage Options: While their rates are great, Geico may not offer as many coverage choices as some competitors.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#2– Progressive: Best for Customizable Coverage

Pros

- Customizable Plans: Geico offers flexible coverage options, making it a great choice among the cheap car insurance companies that only look back 3 years.

- Competitive Rates: Geico’s rates start at $80 per month for minimum coverage. Read more about its rates in this Progressive Car Insurance Review.

- Snapshot Discount: Geico’s Snapshot program lets you save more by tracking your driving habits, a feature many cheap car insurance companies offer.

Cons

- Limited Availability: Some discounts or features may not be available in every area, which could limit options with cheap car insurance companies for certain drivers.

- Higher Rates: If you’re considered a higher-risk driver, Geico’s rates might not be the cheapest from cheap car insurance companies.

#3 – Nationwide: Best for Local Focus

Pros

- Local Expertise: Nationwide is a great choice for drivers who want a company that knows the local area and can offer affordable car insurance with a three-year look-back.

- Competitive Pricing: With rates starting at just $85 a month, Nationwide has affordable car insurance.

- Personalized Service: They also offer excellent customer service tailored to your area, ensuring a more personal experience.

Cons

- Limited Online Tools: Nationwide doesn’t have as many easy-to-use online features as some other companies. Want more details? Check out our Nationwide Car Insurance Review.

- Full Coverage Costs More: While local focus is a strength, Nationwide’s complete coverage plans can be slightly more expensive.

#4 – Farm Bureau: Best for Vanishing Deductible

Pros

- Vanishing Deductible: The vanishing deductible program helps you lower your rates over time, making it on our list of the top cheap car insurance companies that only look back 3 years.

- Low Initial Rates: With a starting rate of $90 per month, Farm Bureau offers affordable coverage for many types of drivers.

- Local Focus: Like Nationwide, Farm Bureau provides excellent local service with a focus on regional needs. Find everything you need in our Farm Bureau Car Insurance Review.

Cons

- Limited National Availability: Farm Bureau’s availability is limited to certain states, which may restrict access for some drivers.

- Costly Comprehensive Coverage: Full coverage options may be more expensive compared to other providers.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#5 – American Family: Best for Strong Reputation

Pros

- Affordable Rates: Plans start at just $95 a month, so you can save while getting reliable coverage that suits you. For more info, check out our American Family Car Insurance Review.

- Great Coverage Options: Whether you need just the basics or want some extra features, they’ve got plans to keep you covered wherever you go.

- Reliable Protection: With a range of coverage options, you can drive confidently, knowing you’re fully protected no matter what.

Cons

- Higher Premiums for Customization: Customizing your coverage can increase your premiums, which might not be great if you’re trying to stick to a budget.

- Limited Discounts: American Family may not offer as many discounts as other insurers or cheap car insurance companies, but they still provide quality coverage options.

#6 – Travelers: Best for Flexible Options

Pros

- Competitive Rates: Starting at just $100 a month, Travelers is one of the cheap car insurance companies that look only 3 years back. Find more in our Travelers Car Insurance Review.

- Great Discounts: Travelers provides discounts that help keep premiums low when buying car insurance from cheap car insurance companies that look only 3 years back.

- Flexible Coverage: They offer flexible coverage options that fit different needs, especially for those looking for affordable car insurance that only looks at the past three years.

Cons

- Limited Customer Support: Travelers might not offer as strong customer support as some other companies, which could lead to slower response times.

- Younger Drivers and Costs: Younger drivers often pay higher insurance costs due to inexperience, but cheap car insurance companies that only look back three years can help.

#7 – State Farm: Best for Accident Forgiveness

Pros

- Competitive Rates: Starting at just $105 a month, State Farm offers affordable car insurance that won’t cost you a fortune.

- Great Customer Service: State Farm’s awesome customer service ensures that your claims are taken care of quickly and without hassle.

- Accident Forgiveness: Its accident forgiveness program makes it one of the cheap car insurance companies that only look back 3 years after your first at-fault accident.

Cons

- Limited Customization: State Farm’s coverage options might not be as customizable as some other companies. For more details, check out our State Farm Car Insurance Review.

- Higher Premiums for Drivers: Drivers with a less-than-perfect driving history might pay more for their premiums.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#8 – Farmers: Best for Diverse Discounts

Pros

- Wide Range of Discounts: Farmers offer many discounts, making it one of those cheap car insurance companies that only look back three years.

- Affordable Rates: Farmer’s car insurance rates are competitive, starting at $110 per month for minimum coverage.

- Good Customer Service: Farmers is known for having reliable customer service and claims representatives. Get expert insights in our Farmers Car Insurance Review.

Cons

- Fewer Coverage Options: Farmers may not have as many specialized coverage options as some other cheap car insurance companies.

- Growing Costs for Drivers: Young drivers might pay more with Farmers than other cheap car insurance companies.

#9 – Liberty Mutual: Best for Customizable Policies

Pros

- Customizable Policies: Liberty Mutual stands out by offering flexible policies that can be tailored to fit the needs of car insurance companies with a three-year look-back.

- Bundle Discounts: Liberty Mutual gives big discounts when you bundle your auto insurance with other policies, offering affordable car insurance.

- Competitive Rates: With rates starting at $115 a month, Liberty Mutual is an affordable car insurance option. Our Liberty Mutual Car Insurance Review has got you covered.

Cons

- Expensive Full Coverage Options: Full coverage plans with Liberty Mutual can be more expensive compared to other cheap car insurance companies.

- Limited Local Service: Liberty Mutual might not have the same level of local service as some regional cheap car insurance companies.

#10 – Allstate: Best for Comprehensive Coverage

Pros

- Comprehensive Coverage: Allstate is last on our list of cheap car insurance companies that only look back three years, offering comprehensive coverage options.

- Trusted Provider: Allstate is known for its reliability and reputation in the insurance industry. Use our Allstate Car Insurance Review for more details.

- Great Pricing on Coverage: Allstate offers competitive rates starting at just $120, making it a great choice for budget-friendly car insurance.

Cons

- Insurance Costs: Allstate’s rate may be higher for drivers or those with less experience behind the wheel.

- Limited Discount Opportunities: Some drivers may find Allstate’s discount offerings to be more limited than those of other providers.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Companies Offering Car Insurance With a Three-Year Lookback

Progressive and State Farm typically review driving and insurance records from the past two to three years when assessing risk, setting rates, or determining eligibility for coverage. Recent accidents, traffic violations, and insurance lapses may impact your premium or policy approval.

However, serious infractions, such as DUIs, may stay on record longer and have a more lasting effect. Each company has its underwriting guidelines, so specific policies may vary. Most car insurance companies look back three years. Here’s a list of the best car insurance companies that look back three years or less.

- Allstate

- American Family

- Farmers

- Geico

- Liberty Mutual

- Nationwide

- Travelers

- USAA

What about insurance companies that accept bad driving records and don’t look back three years? State statutes may limit car insurance companies that don’t look back three years

Read more:

- Allstate vs. Nationwide Car Insurance

- Allstate vs. USAA Car Insurance

- American Family vs. Liberty Mutual Car Insurance

- American Family vs. State Farm Car Insurance

Your Past Three Years Matter for Car Insurance

Traffic infractions can last more than three years on your driving record. For example, some states keep speeding violations on your driving history for more than five years. In some states, car insurance companies look back more than three years. States like Maine, Mississippi, New Mexico, and Pennsylvania hold on to speeding violations for one year.

Car Insurance Monthly Rates by Provider & Coverage Level From Companies That Only Look Back 3 Years

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $120 | $195 | |

| $95 | $170 | |

| $90 | $165 | |

|

| $110 | $185 |

| $75 | $140 | |

| $115 | $190 | |

| $85 | $160 | |

|

| $80 | $150 |

| $105 | $180 | |

| $100 | $175 |

However, insurance companies want to check for serious driving violations, such as at-fault accidents and DUI convictions. Therefore, most companies may look back five years or more when determining rates for cheap car insurance with points.

Read more:

- Arkansas

- Delaware

- Iowa

- Kansas

- Maine

- Minnesota

- Mississippi

- Nebraska

- Nevada

- North Dakota

- Oklahoma

- South Carolina

- Tennessee Car Insurance

- Texas

- Utah

- West Virginia

The Difference Between Driving History and Car Insurance History

The short answer is yes. But your insurance record is just as important as your driving history. According to the Consumer Financial Protection Bureau, the Comprehensive Loss Underwriting Exchange (CLUE) catalogs your insurance history in its database, which can impact your ability to find the cheapest insurance with tickets on your record.

Cheap car insurance companies that only look back 3 years often offer accident forgiveness, helping drivers avoid rate hikes after their first accident.Jeffrey Manola Licensed Insurance Agent

Your car insurance history can affect your premiums, coverage options, and even eligibility with some companies. A list of auto insurance companies may show that insurers offer discounts for having a clean insurance record, just as they might for safe driving habits.

Car Insurance Discounts From the Top Providers That Only Look Back Three Years

| Insurance Company | Available Discounts |

|---|---|

| Bundling, Safe Driver, Good Student, New Vehicle, Easy Pay Plan | |

| Bundling, Safe Driver, Teen Driver, Loyalty | |

| Bundling, Good Student, Homeowners, Safety Course | |

|

| Bundling, Good Student, Homeowners, Safety Course |

| Good Driver, Bundling, Military, Federal Employee, New Vehicle | |

| Bundling, Safe Driving, New Car, Homeowners | |

| Bundling, Accident-Free, Good Student, Safe Driver | |

|

| Snapshot Program, Bundling, Safe Driver, Homeowners, Continuous Coverage |

| Bundling, Safe Driver, Good Student, Drive Safe & Save | |

| Bundling, Safe Driver, Good Student, Homeowners, Hybrid/Electric Vehicle |

So, both your driving behavior and your claims history play a role in determining your insurance rates. In fact, insurance companies look at 3-year history, which shows that a strong insurance record can even help you secure better coverage at a lower cost.

The Role of Your Driving History in Car Insurance

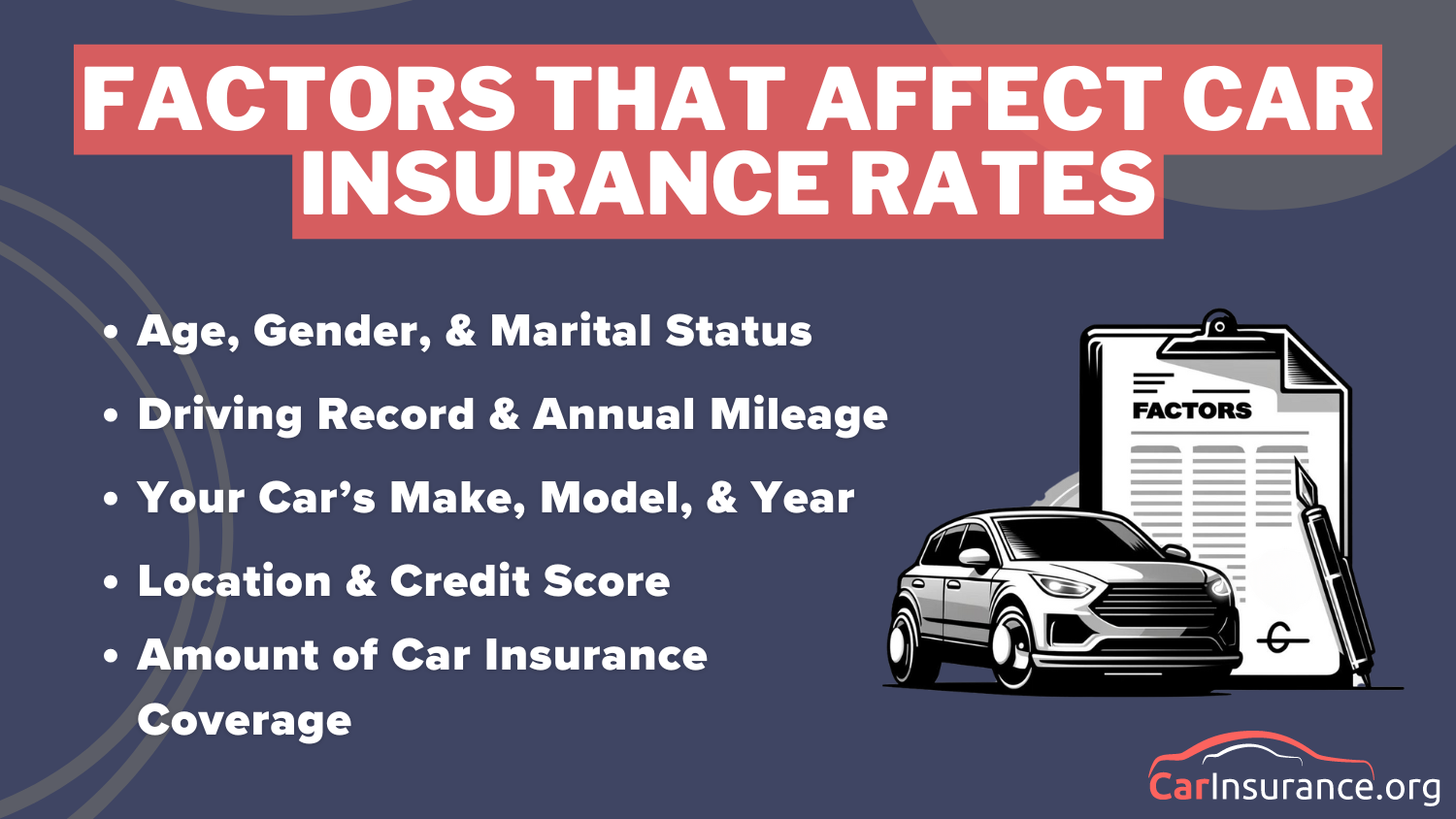

Your driving record correlates to risk. For example, a clean driving record shows that you’re less likely to file an insurance claim. Any traffic violations on your driving record correlate to higher chances of filing a car insurance claim. Most driving infractions have an impact on car insurance rates. For example, DUIs drive up your insurance rates by 72%.

Each state handles DUI differently, but car insurance companies across the United States increase car insurance rates if you have a DUI on your driving record. Expect your insurance rates to look similar when you have multiple speeding tickets, reckless driving violations, and accidents. Drivers with too many infractions are considered high-risk.

Read More:

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Common Traits of High-Risk Drivers

Too many driving violations or accidents place you in a high-risk pool. Some states require you to get an SR-22 (SR-50 in Indiana) when you are listed as a high-risk driver. If you need car insurance with a claims history, Florida and Virginia, both have FR-44 for high-risk drivers who have been convicted of a DUI.

An easy way to save money? Customize with Liberty Mutual. Plus, 13 other tips for lowering your car insurance. https://t.co/Fi4LjmDXye pic.twitter.com/W8CifJuAVP

— Liberty Mutual (@LibertyMutual) July 19, 2023

Your high-risk driving status can last up to three years under SR-22. If you’re still considered a high-risk driver after that, you’ll have to reapply for SR-22 certification. Drivers who don’t get SR-22 certified could lose their car insurance coverage, and the insurance company can report their uninsured status to the state DMV.

Read more: How the States Rank on Uninsured Drivers

Case Studies: Finding Coverage From Cheap Car Insurance Companies That Only Look Back 3 Years

In this section, we’ll take a look at three drivers who found affordable car insurance with the cheapest car insurance companies that only check the past three years. Each story shows how these companies met different needs and helped them get great coverage at a good price.

Case Study 1: Danny’s Experience with Geico

Danny was looking for affordable car insurance after a minor accident. Geico offered him a great deal with their accident forgiveness program, ensuring his rates stayed the same despite his first at-fault accident. With a starting monthly payment of only $75, Geico turned out to be the best option for him.

Case Study 2: Louie’s Success with Progressive

Louie needed more flexibility with his coverage, so he chose Progressive. Their customizable options let him tweak his policy to match his driving habits and get the best rates. Plus, with their three-year look-back, Louie found a plan that fit his budget and lifestyle perfectly.

Case Study 3: Warren’s Local Focus with Nationwide

Warren needed an insurance company that understood the local area and could offer him personalized service. Nationwide stood out because it focused on the region and had coverage that fit his needs. With its rates and three-year look-back period, Warren was able to easily find affordable car insurance.

These examples show how affordable car insurance companies that only look at the past three years can offer coverage that works for different needs while keeping prices down. By focusing on a shorter history, they make it easier for drivers to get the coverage they need without paying extra.

Key Insights on Car Insurance Companies With a 3-Year Lookback

Geico, Progressive, and Nationwide are some of the best car insurance companies that only look back three years. But that could change depending on the state where you live. Car insurance with a three-year accident history is more expensive than average, and it could take longer to receive more affordable rates.

Now that you know more about the cheap car insurance companies that only look back 3 years, use our free online quote tool to compare multiple insurance companies near you.

Frequently Asked Questions

How far back does car insurance look?

Car insurance companies typically check your driving record for the last 3 to 5 years. They want to know about past accidents, violations, and claims. This helps them decide on your premiums and coverage.

Are there insurance companies that don’t check driving records?

Some insurance companies may not check your driving record at all. However, most companies will review it to determine risk. It’s essential to compare policies to find one that suits you. Finding cheap car insurance quotes is easy. Just enter your ZIP code into our free comparison tool to instantly compare quotes near you.

How far back does Geico look at your driving record?

Geico usually looks at your driving record for the last 3 to 5 years. They check for accidents and violations to calculate your insurance rate. This helps them assess the level of risk they’re taking on.

Read more: How Much Insurance Do I Need for My Car?

What’s better: American Family vs Nationwide?

When comparing American Family vs Nationwide, it depends on your specific needs. American Family offers more tailored options, while Nationwide might be better for those with a driving record that includes claims. Both companies have unique benefits and coverage options.

Can I get car insurance with no insurance history?

Yes, you can get car insurance with no insurance history, but it may be more expensive. Some insurance companies specialize in providing coverage for drivers without previous insurance. Expect to pay higher rates as there’s more risk involved.

What about the American Family vs Progressive, which company is better?

When comparing American Family vs Progressive, Progressive is often the best option for those with a bad driving history. American families may offer more discounts for safer drivers. It’s good to compare their coverage options to find the right fit. Compare car insurance rates by state.

Can I get auto insurance quotes with a bad driving record?

Yes, you can get auto insurance quotes for bad driving records. Some insurance companies specialize in offering policies to high-risk drivers. However, expect higher rates for your coverage.

What’s the best car insurance for accident history?

If you have an accident history, the best car insurance will be from companies specializing in higher-risk drivers. Look for car insurance with an accident history that offers reasonable premiums. Some providers may even accept a bad driving history insurance policy. Find the best comprehensive car insurance quotes by entering your ZIP code into our free comparison tool today.

Will car insurance check my claims history?

Yes, car insurance companies typically check your claims history. This helps them assess your level of risk as a driver. If you have past claims, be prepared for potentially higher premiums. For further reading, check out: Do I need full coverage on a financed car?

How often does State Farm check driving records?

State Farm typically checks your driving record when you first apply for insurance and when your policy renews. They use your auto insurance history and any car insurance history check to assess your risk level. This helps them determine your premium and decide if any adjustments are needed for your coverage.

Related Articles

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.