Best Car Insurance in Oklahoma for 2026 [Check Out the Top 10 Companies]

State Farm, Geico, and Progressive offer the best car insurance in Oklahoma, with rates starting as low as $22 per month. State Farm is a great option for low-income drivers in Oklahoma. Geico earns an A++ rating for claims handling, while Progressive's digital tools make it easy to get car insurance quotes in Oklahoma.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Expert Insurance Writer

Merriya Valleri is a skilled insurance writer with over a decade of professional writing experience. Merriya has a strong desire to make understanding insurance an easy task while providing readers with accurate and up-to-date information. Merriya has written articles focusing on health, life, and auto insurance. She enjoys working in the insurance field, and is constantly learning in order to ...

Merriya Valleri

Licensed Insurance Agent

Daniel Walker graduated with a BS in Administrative Management in 2005 and has run his family’s insurance agency, FCI Agency, for over 15 years (BBB A+). He is licensed as an insurance agent to write property and casualty insurance, including home, life, auto, umbrella, and dwelling fire insurance. He’s also been featured on sites like Reviews.com and Safeco. To ensure our content is accura...

Daniel Walker

Updated May 2025

18,157 reviewsCompany Facts

Full Coverage in Oklahoma

A.M. Best Rating

Complaint Level

Pros & Cons

18,157 reviews19,116 reviewsCompany Facts

Full Coverage in Oklahoma

A.M. Best Rating

Complaint Level

Pros & Cons

19,116 reviews13,285 reviewsCompany Facts

Full Coverage in Oklahoma

A.M. Best Rating

Complaint Level

Pros & Cons

13,285 reviewsState Farm, Geico, and Progressive provide the best car insurance in Oklahoma, with monthly rates starting as low as $22 per month.

Discover what car insurance coverage options work best in Oklahoma with our comprehensive guide, which features minimum liability requirements, weather-related risks, and uninsured driver impacts.

Learn about Oklahoma’s 25/50/25 minimum requirements, common weather-related claims, available discounts up to 30%, and accident statistics across major cities like Oklahoma City and Tulsa for informed coverage decisions.

Our Top 10 Company Picks: Best Car Insurance in Oklahoma

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 17% | B | Overall Coverage | State Farm | |

| #2 | 25% | A++ | Affordable Rates | Geico | |

| #3 | 10% | A+ | Flexible Options | Progressive |

| #4 | 10% | A++ | Military Families | USAA | |

| #5 | 20% | A | Customizable Policies | Farmers |

| #6 | 25% | A+ | Accident Forgiveness | Allstate | |

| #7 | 25% | A | New Car Owners | Liberty Mutual | |

| #8 | 13% | A++ | Green Vehicles | Travelers | |

| #9 | 20% | A+ | Safe Drivers | Nationwide | |

| #10 | 25% | A | Customer Service | American Family |

Keep reading to discover how to find the best rates and coverage options tailored to your specific driving needs and budget.

- State Farm offers Oklahoma’s lowest full coverage at $91 monthly

- Geico stands out with $35 monthly minimum coverage and an A++ rating

- Progressive’s Name Your Price tool allows OK drivers to personalize coverage

Shop for the best liability-only car insurance with our free quote comparison tool. Enter your ZIP code to begin.

#1 – State Farm: Overall Top Pick

Pros

- Affordable Prices: Those looking for affordable car insurance in Oklahoma can enjoy State Farm plans starting at $29 per month.

- Generous Discounts: Drivers can bundle home and auto insurance to save even more, making it an affordable Oklahoma car insurance company.

- Exceptional Customer Service: State Farm stands out in claims reliability across cities like Tulsa and Oklahoma City. Check our State Farm car insurance review for more info.

Cons

- Limited Online Tools: State Farm lacks advanced digital features and online policy management options.

- Drivers Face Higher Rates: Compared to other affordable auto insurance companies in Oklahoma, rates tend to increase for drivers with past claims or traffic violations.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#2 – Geico: Best for Affordable Rates

Pros

- Low Premiums: Geico offers customers some of the cheapest car insurance rates in Oklahoma at $35 monthly. Learn more in our Geico car insurance review.

- Superior Claims Handling: Geico is known for its efficient claims process and has an A++ rating from A.M. Best.

- Easy-to-Use App: Geico’s top-tier mobile app makes it easy to file claims, update policies, and pay bills, which is ideal for tech-savvy drivers in OKC.

Cons

- Limited Local Agents: With most services online, Geico lacks in-person support in smaller Oklahoma communities.

- Fewer Customization Options: Geico’s policy add-ons are more limited than those of other large OK insurers.

#3 – Progressive: Best for Flexible Options

Pros

- Unique Pricing Tool: Progressive’s Name Your Price tool lets customers find coverage that fits their budget.

- Lots of Discounts: Progressive provides Oklahoma drivers multiple discounts, including good driver and Snapshot usage-based savings.

- Strong Digital Experience: It has a highly-rated mobile app and online tools for smooth transactions. Learn more in our Progressive car insurance review.

Cons

- Customer Service Complaints: Reports of mixed experiences with claims handling and responsiveness.

- Digital Interaction: Unlike other large insurance providers, Progressive relies mostly on web-based services instead of face-to-face agents.

#4 – USAA: Best for Military Families

Pros

- Customer Support: Top providers such as USAA are known for great customer support and are consistently ranked at the top.

- Competitive Rates: Eligible drivers can obtain the lowest car insurance rates in Oklahoma, at $22 per month. For more information on its products, check out our USAA car insurance review.

- Financial Stability: USAA ensures claim payout reliability, maintaining its superior financial ratings.

Cons

- Limited Offers: Only military members, veterans, and their immediate families can join, limiting availability to the general Oklahoma population.

- Few USAA Branches: USAA doesn’t operate physical branches in Oklahoma, relying mainly on online and phone-based services.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#5 – Farmers: Best for Customizable Policies

Pros

- Driver-Selectable Options: Farmers leads in Oklahoma with a range of policy add-ons, such as accident waivers and replacement options.

- Highly Rated Service: With a strong presence across Oklahoma, Farmers offers personalized service and support through its network of in-state agents.

- Innovative Usage Programs: Safe drivers can receive discounts on insurance premiums through an app that offers rewards.

Cons

- Unavailability in Some Areas: Some parts of Oklahoma may not have full access to Farmers’ policy options or agents.

- Discount Eligibility: Strict eligibility requirements make it harder for some drivers to get discounts. For more discounts, see our Farmers car insurance review.

#6 – Allstate: Best for Accident Forgiveness

Pros

- Unique Perks: Oklahoma drivers benefit from Allstate’s optional coverages like accident forgiveness and rideshare insurance. See more in our Allstate car insurance review.

- Multiple Discount Programs: Allstate offers savings through bundling, Drivewise, and safe driver programs, which help get the cheapest auto insurance in OKC.

- Drive Wise Program: Allstate maintains a strong presence in Oklahoma with agents who provide customized support and guidance.

Cons

- Mixed Customer Reports: Although most customers report satisfaction, others in Oklahoma have reported delays and inconsistencies in resolving claims.

- Drivewise Savings Vary: The Drivewise discount depends on how well one drives and doesn’t always translate into big savings.

#7 – Liberty Mutual: Best for New Car Owners

Pros

- Customizable Coverage: Oklahoma drivers can customize their policies with added features like accident forgiveness and new car replacement.

- RightTrack Telematics Discount: Safe drivers in Oklahoma can save up to 30% with Liberty Mutual’s RightTrack program.

- 24/7 Claims Assistance: Liberty Mutual provides round-the-clock customer support for claims and roadside assistance in Oklahoma.

Cons

- Mixed Customer Satisfaction: Some policyholders report delays and inconvenience with claims. Check more in our Liberty Mutual car insurance review.

- Program Limitations: Not all drivers can guarantee maximum savings, and some find telematics tracking uncomfortable.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#8 – Travelers: Best for Green Vehicles

Pros

- Discount Programs: Oklahoma customers can save with multi-policy, safe driver, and hybrid/electric vehicle discounts.

- Financial Strength: With an A++ rating from A.M. Best, Travelers is among the most financially secure insurers serving the Oklahoma market.

- IntelliDrive Telematics System: Travelers offers safe drivers discounts of up to 30% through the IntelliDrive program.

Cons

- Higher Rates: Top providers like Travelers offer more expensive full coverage, but can still provide good value. For more details, read our Travelers car insurance review.

- Limitations on Certain Coverages: Some discounts are limited to specific regions in Oklahoma, so customers may not enjoy them.

#9 – Nationwide: Best for Safe Drivers

Pros

- Special Perks: Nationwide offers Oklahoma drivers added features like a total loss deductible waiver. Learn more in our Nationwide car insurance review.

- Vast Discount Opportunities: Customers can save up to 20% by bundling policies, enrolling in innovative telematics programs, or being a good student.

- Excellent Customer Satisfaction: With high ratings for claims service and overall satisfaction, Nationwide is a reliable pick for many Oklahoma drivers.

Cons

- Limited Availability: Some advanced coverage features and discount programs may be restricted in rural or less-populated areas of Oklahoma.

- Increased Rates: Oklahoma drivers who don’t meet the safe driving criteria provided by Nationwide may receive higher premiums with SmartRide.

#10 – American Family: Best for Customer Service

Pros

- Complete Coverage: American Family offers diverse policies ideal for Oklahoma drivers, including diminishing deductibles and no-penalty accident coverage.

- Generous Offers: Customers in Oklahoma can save with American Family through bundling, loyalty discounts, and the KnowYourDrive telematics program.

- Flexible Local Agents: AmFam receives high ratings, and it’s known as one of the best car and home insurance companies in Oklahoma.

Cons

- Access Barriers: Drivers cannot avail coverage as it’s unavailable in all states.

- Expensive Premiums: Rates may be higher than budget insurers, especially for high-risk drivers. Check our American Family car insurance review for more details.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Oklahoma Car Insurance Rates

How much insurance do I need for my car? Below, you can find the best car insurance rates in Oklahoma by company and coverage level, enabling drivers to compare cheap choices like agreed value car insurance in Oklahoma City to minimum coverage.

Oklahoma Car Insurance Monthly Rates by Provider & Coverage Level

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $45 | $135 | |

| $38 | $118 | |

|

| $44 | $136 |

| $35 | $109 | |

| $60 | $184 | |

| $40 | $122 | |

|

| $36 | $110 |

| $29 | $91 | |

| $34 | $105 | |

| $22 | $68 |

State Farm and USAA offer the lowest monthly premiums for minimum and full coverage in Oklahoma, but every driver’s situation is different.

If you’re a student in Oklahoma or have one on your policy, USAA and State Farm offer up to 25% discount for achieving good grades.Scott W. Johnson Licensed Insurance Agent

Various risk factors drive what you’ll pay, such as claim frequency, theft rates, and weather-related activities. These directly impact how insurance providers price policies throughout the state.

Oklahoma Report Card: Car Insurance Premiums

| Category | Grade | Explanation |

|---|---|---|

| Average Claim Size | B | Higher payouts raise costs |

| Vehicle Theft Rate | B | Increases risk for insurers |

| Traffic Density | C | More vehicles, more accidents |

| Weather-Related Risks | C | Frequent storms cause damage |

| Uninsured Drivers Rate | D | Raises costs for insured drivers |

As you can see from the report card of the state, Oklahoma earns average to below-average grades in many categories that influence insurance pricing. In addition to state-level risks, your location also plays a major role in how much you’ll pay for coverage.

Oklahoma Accidents & Claims per Year by City

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Broken Arrow | 4,000 | 3,000 |

| Edmond | 3,500 | 2,625 |

| Norman | 5,000 | 3,750 |

| Oklahoma City | 17,000 | 12,000 |

| Tulsa | 15,000 | 10,500 |

Are you searching for Oklahoma’s top-rated car insurance without paying too much? In big cities like Oklahoma City or when searching for affordable car insurance in Tulsa, smart consumers are comparing rates from multiple providers.

Car Insurance Discounts in Oklahoma

Since you have to have car insurance in Oklahoma, you might as well get it from a company that rewards good driving. Below, we’ve reviewed the best car insurance in OKC and how they save you money.

Car Insurance Discounts From Top Oklahoma Providers

| Insurance Company | UBI | Good Driver | Bundling | Multi-Car | Good Student |

|---|---|---|---|---|---|

| 10% | 20% | 25% | 25% | 20% | |

| 15% | 20% | 20% | 20% | 25% | |

|

| 15% | 20% | 25% | 25% | 20% |

| 15% | 30% | 25% | 25% | 15% | |

| 10% | 30% | 20% | 20% | 20% | |

| 10% | 25% | 20% | 20% | 15% | |

|

| 15% | 30% | 25% | 25% | 20% |

| 10% | 20% | 20% | 20% | 25% | |

| 10% | 20% | 15% | 15% | 10% | |

| 10% | 25% | 15% | 15% | 25% |

Many of the best car insurance companies in Oklahoma offer discounts for being a good driver, bundling policies, or insuring multiple vehicles. Progressive, Geico, and Liberty Mutual offer up to 30% off for good drivers.

Every company will try to sell itself to customers. It is their job. We are going to take the guessing out of which ones would be a good fit and which ones you should avoid.

If you’re just looking for cheap car insurance, the lowest rates aren’t always from the same company. Insurers use complex algorithms to determine rates, and some of it depends on the individual underwriter.

If you’re new to the process or want to feel more confident when comparing options, take a minute to read how car insurance works so you can make the most informed decision.

Oklahoma’s Minimum Coverage for Auto Insurance

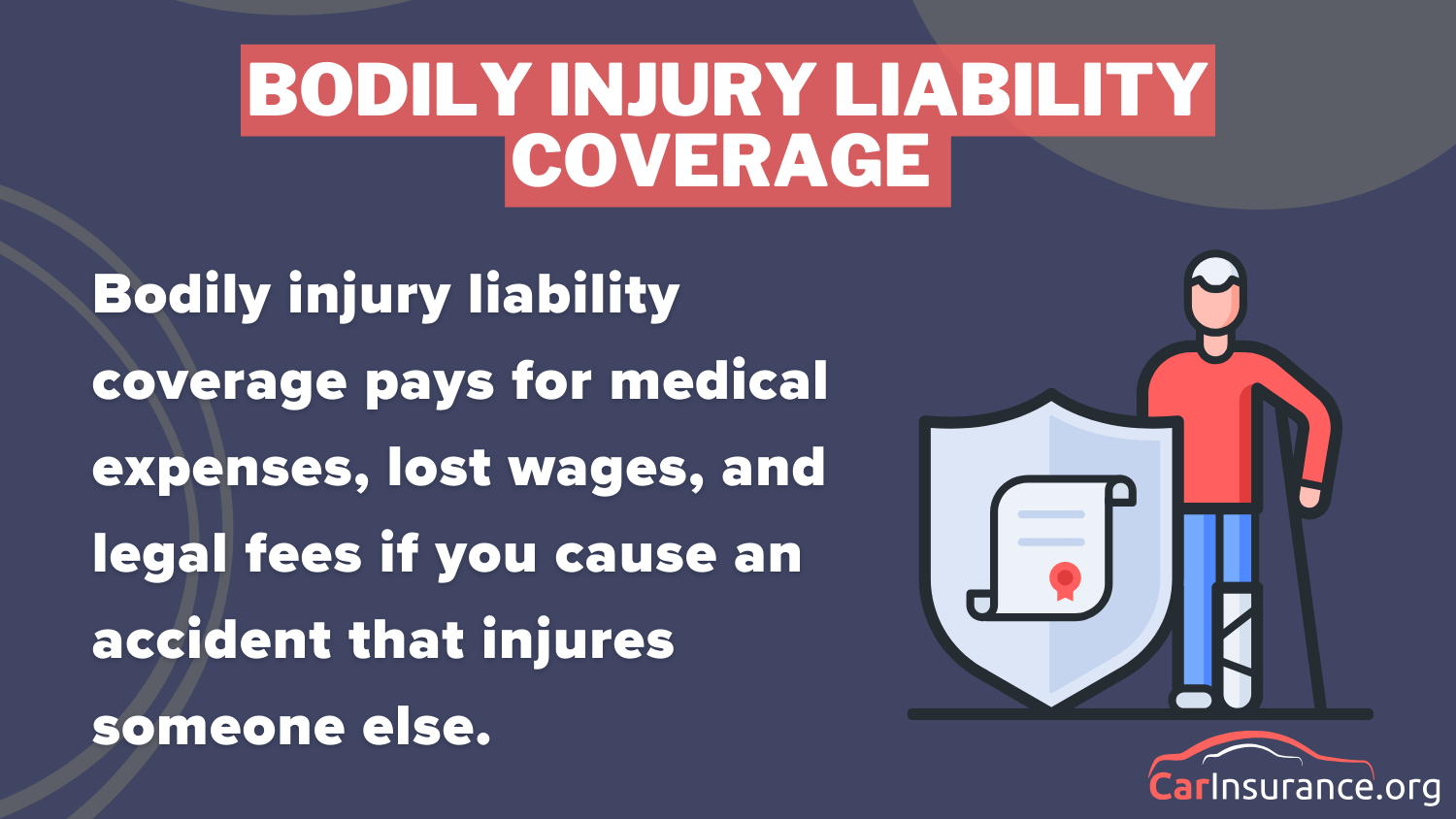

How much coverage do you need on your vehicle? Oklahoma has a minimum required amount. To legally drive in Oklahoma, you must carry at least the state minimum liability coverage:

- $25,000 for bodily injury per person

- $50,000 for bodily injury per accident

- $25,000 for property damage

These limits do not cover your own damages in an accident where you are at fault. You can add other coverages to your policy to cover you and your vehicle.

It is always wise to talk to your insurance agent. An agent can help you decide what you need, and then they can get quotes from different companies for that coverage.

5 Most Common Car Insurance Claims in Oklahoma

| Claim Type | Portion of Claims | Cost per Claim |

|---|---|---|

| Rear-End Collisions | 30% | $10,000 |

| Weather-Related Damage | 25% | $12,000 |

| Uninsured Motorist Claims | 15% | $25,000 |

| Animal Collisions | 15% | $8,000 |

| Parking Lot Accidents | 15% | $6,000 |

We will also examine the penalties for driving without the minimum insurance coverage. You must show proof of insurance, which you can do with a copy of your policy or ID card.

Read more: If my car breaks down, will insurance cover a rental?

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Keep Right & Move Over Laws in Oklahoma

Most drivers have felt the frustration of being behind a driver traveling under the speed limit in the left lane. In Oklahoma, this isn’t just frustrating — it’s against the law. Under state statute, slower-moving traffic must stay in the right lane, particularly on interstates and highways. This law decreases accidents from sudden lane movement and road rage.

Move-over laws are also crucial in keeping individuals safe. When approaching emergency responders, tow trucks, or road workers, Oklahoma motorists must move over a lane or reduce speed dramatically. Not doing so can lead to hefty fines or even more serious harm.

What are the Oklahoma car seat laws? Oklahoma car seat laws are designed to protect children by requiring age- and size-appropriate restraints.

Looking for the Right Insurance Company in Oklahoma

State Farm, Geico, and Progressive lead the best car insurance in Oklahoma with rates as low as $22 per month. Geico provides superior A++ rated claims handling, and Progressive delivers unique pricing tools for flexible coverage. In getting the best car insurance in Oklahoma, Reddit users reveal helpful tips and real experiences:

Comment

byu/shayshay8508 from discussion

inokc

When searching for affordable auto insurance, Oklahoma drivers can compare multiple quotes online, helping them find personalized coverage options that match their specific needs while balancing cost and protection. To help you find a policy that offers the coverage you need, visit our guide “Why You Need Car Insurance“.

By carefully reviewing each option, you can secure the best and cheapest car insurance in Oklahoma. Check if you’re getting the best deal on car insurance by entering your ZIP code here.

Frequently Asked Questions

How much is car insurance in Oklahoma?

The average Oklahoma car insurance cost is around $160 per month for full coverage and $42 per month for minimum coverage, though rates vary based on factors like driving history, location, and vehicle type.

What are the minimum Oklahoma car insurance laws?

Under Oklahoma car insurance laws, drivers must carry at least 25/50/25 liability coverage, which means $25,000 for bodily injury per person, $50,000 per accident, and $25,000 for property damage. Enter your ZIP code into our free comparison tool to get started.

Where can I find cheap Oklahoma auto insurance?

To find Oklahoma cheap auto insurance, compare rates from different Oklahoma car insurance companies and check for discounts based on driving habits, bundling, and low mileage. To get cheaper rates, read our car insurance basics.

What affects Oklahoma car insurance rates?

Oklahoma auto insurance rates depend on your driving record, credit score, vehicle type, and location. Oklahoma City car insurance is sometimes higher than in rural areas.

What discounts are available for Oklahoma City car insurance?

Discounts include safe driver, bundling, military, and good student incentives. Drivers in Oklahoma City can lower their rates by qualifying for multiple car insurance discounts.

Does Oklahoma offer low-income car insurance options?

While Oklahoma doesn’t have specific low-income car insurance in Oklahoma programs, drivers can lower costs by choosing minimum liability, usage-based policies, or seeking out low-cost auto insurance in Oklahoma providers.

Read More: Car Maintenance Expenses

What are my options for affordable car insurance in Tulsa, OK?

To find affordable car insurance in Tulsa, OK, compare rates online, seek bundling discounts, and consider minimum coverage plans if eligible. Tulsa residents often save by comparing local insurer deals.

Is there affordable auto insurance in Tulsa for low-mileage drivers?

Yes, many providers offer affordable auto insurance in Tulsa for drivers with low annual mileage. Usage-based insurance is ideal for saving on premiums if you drive less frequently.

What discounts are available for Oklahoma City car insurance?

Many insurers offer Oklahoma City car insurance discounts for safe driving, bundling policies, military service, and good student discounts, which can help lower your Oklahoma car insurance rates.

What’s the best car insurance in Oklahoma for seniors?

The best car insurance in Oklahoma for seniors often includes senior discounts, accident forgiveness, and low-mileage savings. Companies like The Hartford and Geico offer tailored senior coverage.

Related Articles

-

Mar 2025

Safety Car Insurance Review in 2026 [See if They’re a Good Fit]

-

Mar 2025

American Family vs. Liberty Mutual Car Insurance in 2026 [Head-to-Head Review]

-

Mar 2025

Root Car Insurance Review for 2026 [Expert Evaluation]

-

Mar 2025

Metromile Car Insurance Review for 2026 (Rates & Discounts Analyzed)

-

Jun 2025

Clearcover Car Insurance Review for 2026 [What You Need to Know]

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.