Best Car Insurance in Minnesota for 2026 [MN’s Top 10 Companies]

Get the best car insurance in Minnesota from State Farm, Progressive, and Geico with rates as low as $27 per month. State Farm stands out as MN's best car insurance pick. Progressive offers Minnesota motorists customizable coverage. Geico provides Minnesota residents bundling savings for winter driving protection.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Expert Insurance Writer

Merriya Valleri is a skilled insurance writer with over a decade of professional writing experience. Merriya has a strong desire to make understanding insurance an easy task while providing readers with accurate and up-to-date information. Merriya has written articles focusing on health, life, and auto insurance. She enjoys working in the insurance field, and is constantly learning in order to ...

Merriya Valleri

Licensed Insurance Agent

Jeff is a well-known speaker and expert in insurance and financial planning. He has spoken at top insurance conferences around the U.S., including the InsuranceNewsNet Super Conference, the 8% Nation Insurance Wealth Conference, and the Digital Life Insurance Agent Mastermind. He has been featured and quoted in Nerdwallet, Bloomberg, Forbes, U.S. News & Money, USA Today, and other leading fina...

Jeff Root

Updated May 2025

18,157 reviewsCompany Facts

Full Coverage in Minnesota

A.M. Best Rating

Complaint Level

Pros & Cons

18,157 reviews13,285 reviewsCompany Facts

Full Coverage in Minnesota

A.M. Best Rating

Complaint Level

Pros & Cons

13,285 reviews19,116 reviewsCompany Facts

Full Coverage in Minnesota

A.M. Best Rating

Complaint Level

Pros & Cons

19,116 reviewsState Farm, Progressive, and Geico offer the best car insurance in Minnesota, starting at $27 monthly.

State Farm offers Minnesota drivers financial security, an A++ A.M. Best rating, and a large agent network for personalized service.

Progressive has customizable coverage options with multiple discount programs to lower premiums for safe and high-risk Minnesota drivers. Geico has cheap rates and up to 25% savings with bundling discounts.

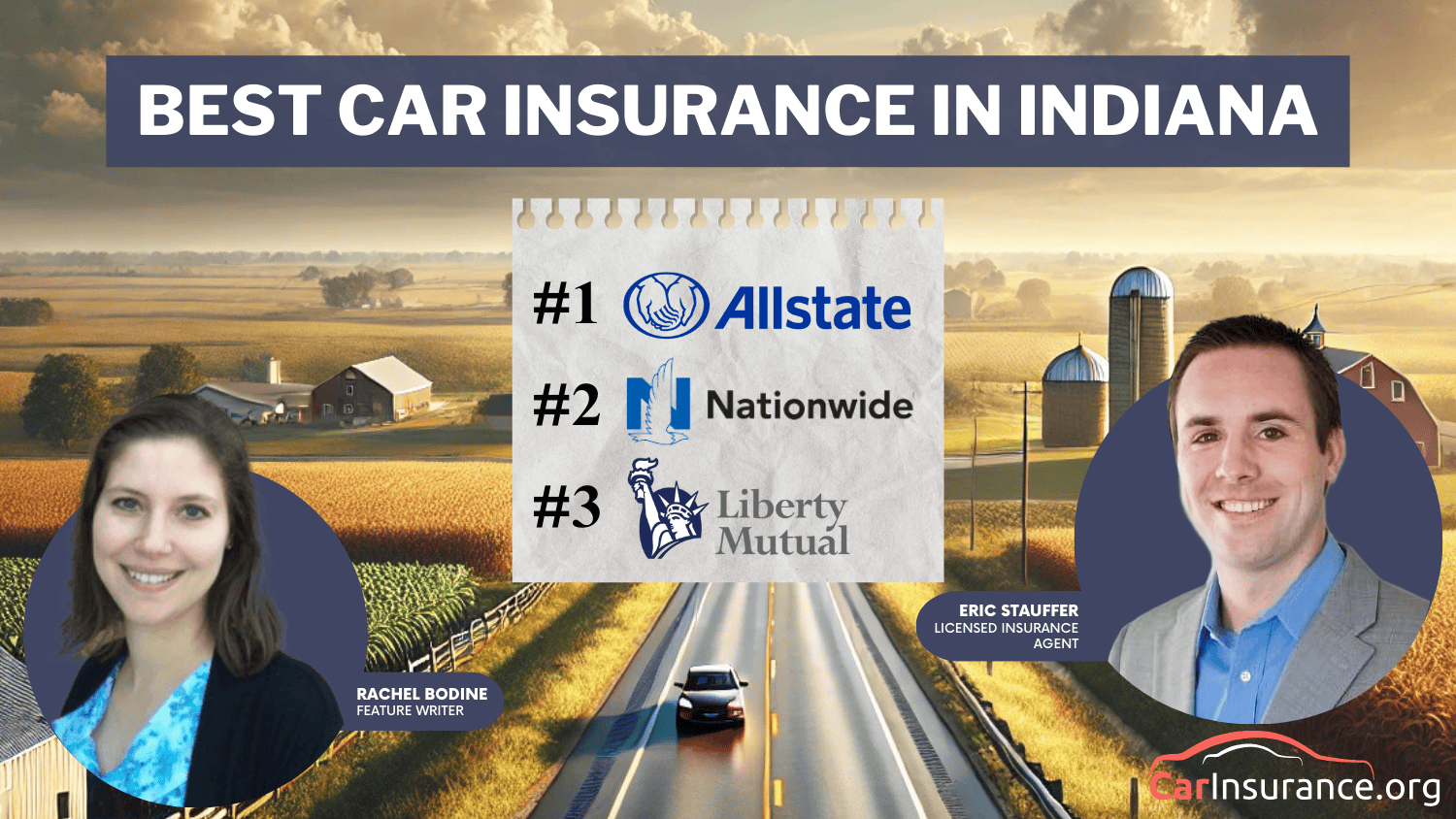

Our Top 10 Company Picks: Best Car Insurance in Minnesota

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 17% | A++ | Reliable Coverage | State Farm | |

| #2 | 10% | A+ | Competitive Rates | Progressive |

| #3 | 25% | A++ | Many Discounts | Geico | |

| #4 | 10% | A++ | Military Families | USAA | |

| #5 | 25% | A+ | Comprehensive Options | Allstate | |

| #6 | 13% | A++ | Customizable Policies | Travelers | |

| #7 | 20% | A | Local Agents | Farmers |

| #8 | 25% | A | Family Discounts | American Family | |

| #9 | 25% | A | Flexible Coverage | Liberty Mutual | |

| #10 | 20% | A+ | Claims Satisfaction | Nationwide |

Minnesota requires 30/60/10 liability plus personal injury protection and uninsured/underinsured motorist coverage, but most drivers need to understand the different types of car insurance coverage to know which coverage they need.

- State Farm has the best car insurance rates and discounts in MN

- Geico offers up to 25% discounts and has an A++ A.M. Best rating

- Bundling discounts may help you save 10% to 25% off your premiums

Read more about the top 10 providers for the best auto insurance in MN. Our free online comparison tool allows you to compare cheap car insurance quotes in Minnesota instantly — just enter your ZIP code to get started.

#1 – State Farm: Top Pick Overall

Pros

- Large Agent Network: State Farm’s agents can help you find the best car insurance rates in Minnesota. Check more in our State Farm car insurance review.

- Financial Security & Claims Experience: State Farm has an A++ A.M. Best rating, which supports its strong financial and claims experience.

- Efficient Claims & High Satisfaction: State Farm’s reliable claims process offers 24/7 support through a convenient app, making it the best option for car insurance in Minnesota.

Cons

- Higher Premiums for High-Risk Drivers: Driving history is a factor in getting MN’s cheap car insurance from State Farm, so review different options to find the best deal.

- Limited Coverage Customization: Customers receive standard coverage from State Farm, but the company provides fewer customization choices than its competitors.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#2 – Progressive: Best for Customizable Coverage

Pros

- Extensive Discounts Available: Offers Minnesota drivers a premium level by offering multiple discount options. Read more in our Progressive car insurance review.

- Usage-Based Insurance Programs: It has innovative programs like Snapshot that track driving habits, helping Minnesota motorists earn personalized rate reductions.

- Flexible Coverage Options: The company provides customizable policy features and add-ons that allow MN residents to tailor their coverage to meet state requirements.

Cons

- Higher Premiums for Low-Risk Drivers: Progressive’s premium rates often become higher for drivers who maintain a safe driving record.

- Limited Local Agent Support: Operations focus on online services, which reduces the number of local agent locations in the state.

#3 – Geico: Best for Budget-Friendly Rates

Pros

- Affordable Premiums: Geico, one of the best car insurance options in Minnesota, offers affordable premiums. With bundling discounts, you can save up to 25%.

- Digital Experience: It provides an easy-to-use digital platform and mobile app features that support policy management. See more in our Geico car insurance review.

- Strong Finances: Proven finances guarantee timely payment of claims, making them the best car insurance provider in Minnesota.

Cons

- Limited Local Agent: The online and phone-based operations limit local drivers’ access to in-person agent services.

- Higher Rates for High-Risk Drivers: Geico’s rates rise significantly for drivers with accidents, DUIs, or poor credit.

#4 – USAA: Best for Military Families

Pros

- Exceptional Customer Service: USAA, the top car insurance company in Minnesota, offers exceptional claims satisfaction and speedy, professional help.

- Competitive Military Rates: USAA’s car insurance review provides rate breakdowns for lower premiums and exclusive discounts for military families.

- Military-Friendly Coverage: USAA offers accident forgiveness, roadside assistance, and customizable coverage options in Minnesota.

Cons

- Limited Eligibility: Inaccessible to most residents in Minnesota due to USAA’s military-only membership.

- No Local Offices: USAA operates online and by phone, with no physical offices in Minnesota, despite being one of the best car insurance companies in the state.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#5 – Allstate: Best for Comprehensive Options

Pros

- Strong Local Agent Network: Its reliable network of agents provides personalized help with Minnesota insurance policies. For more details, see our Allstate car insurance review.

- Comprehensive Options: As the best car insurance option in Minnesota, it offers liability to full coverage, accident forgiveness, and roadside assistance.

- Competitive Discounts: Discounts for safe driving and bundling can save you up to 25% off on car insurance in Minnesota.

Cons

- Higher Premiums: Allstate may have higher rates for some drivers, especially those with violations on their records.

- Customer Service Variability: Service quality varies across provider network locations, with customers finding exceptional agents but also facing issues with claims or billing.

#6 – Travelers: Best for Customizable Policies

Pros

- Customizable Options: According to Travelers’ car insurance review, they offer accident forgiveness, new car replacement, and gap insurance, ideal for premium coverage.

- Great Discounts: They provide discounts for safe driving, hybrid cars, and combining policies, attractive to drivers looking for the best Minnesota insurance.

- Financial Strength: It has an A++ A.M. Best rating, which ensures a reliable claims process and reinforces its status as the best insurance provider in Minnesota.

Cons

- Higher Premiums: Rates may be higher for young or high-risk drivers, which is something to consider when seeking the best insurance companies in Minnesota.

- Limited Local Agents: Travelers have fewer local agents in Minnesota, which might disadvantage those who prefer in-person service.

#7 – Farmers: Best for Local Agents

Pros

- Strong Local Agent Network: Farmers Insurance has a zero-complaint ratio, and its agents offer personalized support, making it one of the best car insurance providers in Minnesota.

- Excellent Coverage Options: Tailored policies, including accident forgiveness and rideshare coverage, contribute to its reputation as the best car insurance in Minnesota.

- Solid Discounts for Savings: Farmers Insurance offers discounts for bundling home and auto insurance, as well as for safe driving. Read this Farmers car insurance review for more.

Cons

- Higher Premiums: Premiums are higher unless multiple discounts are applied.

- Limited Online Policy Management: The digital policy management system is functional but lacks the seamless experience of fully digital providers.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#8 – American Family: Best for Family Discounts

Pros

- Strong Local Presence: Offers customized policies and services, making it one of the best car insurance options in the state. See more in our American Family car insurance review.

- Generous Discounts: Check out safe driving tips to earn up to a 25% discount, making American Family a top choice for the best car insurance in Minnesota.

- Superior Customer Satisfaction: It is reputed for quick claims and superior service, earning it the title of the best auto insurance company in Minnesota.

Cons

- Higher Premiums for Some Drivers: Not ideal for younger or high-risk drivers, resulting in higher premiums.

- Limited Online Servicing Options: Some customers find online servicing options limited and require face-to-face assistance from an agent.

#9 – Liberty Mutual: Best for Flexible Coverage

Pros

- Strong Local Presence: Minnesota drivers receive the best car insurance through state-specific policies that address local winter driving needs.

- Customizable Coverage Options: Drivers can manage their insurance better by adding accident forgiveness and new car replacement options.

- Competitive Discounts: Our Liberty Mutual car insurance review highlights discounts of up to 25% for bundling, making it one of the best car insurance options in Minnesota.

Cons

- Higher Premiums for Some Drivers: Offers excellent Minnesota car insurance, but prices are often high for young and risky drivers, which may deter budget-conscious customers.

- Mixed Customer Service Reviews: Liberty Mutual’s car insurance in Minnesota earns mixed reviews, with praise for coverage but complaints about claims delays.

#10 – Nationwide: Best for Claims Satisfaction

Pros

- Strong Coverage Options: The Nationwide car insurance review highlights coverage benefits like accident forgiveness, total loss replacement, and vanishing deductibles.

- Competitive Discounts: Offers multiple savings discounts of up to 40% through their multi-policy, safe driving, and defensive driving course initiatives.

- Reliable Claims Process: Minnesota drivers receive 24/7 claims help and access to approved repair shops.

Cons

- Higher Than Average Premiums: Nationwide offers reliable policies, but its prices are higher than those of other providers.

- Limited Local Agent Availability: Customers may experience difficulty locating local agents, especially in rural regions.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Average Monthly Car Insurance Rates in MN

How much is car insurance in Minnesota? This comparison chart displays rates from leading insurers such as State Farm, Geico, and Progressive. At just $27 a month for minimum coverage from State Farm, you can get cheap protection that satisfies Minnesota’s mandates without blowing your budget.

Minnesota Car Insurance Monthly Rates by Provider & Coverage Level

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $65 | $160 | |

| $38 | $93 | |

|

| $44 | $108 |

| $37 | $90 | |

| $153 | $375 | |

| $35 | $87 | |

|

| $41 | $101 |

| $27 | $67 | |

| $38 | $94 | |

| $28 | $68 |

Finding out how to get the most for your money when shopping for a car insurance policy means understanding what is required of you as a vehicle owner in Minnesota.

Because rates can sometimes fluctuate, it’s a good idea to shop around for your car insurance policy to get cheap full coverage car insurance in Minnesota. Part of this process is becoming a well-informed consumer by reading our car insurance guide.

Minnesota’s Car Insurance Coverage and Discounts

Minnesota is a great place to live. The North Star State also cares about the safety and security of its residents, which is why it has passed legislation to ensure that all drivers in the Land of 10,000 Lakes are protected. Knowing these requirements and who is offering you the best price for them can be tricky, though. That is where we come in.

Car Insurance Discounts from Top Minnesota Providers

| Insurance Company | Anti-Theft | Bundling | Good Driver | Good Student | UBI |

|---|---|---|---|---|---|

| 10% | 25% | 25% | 20% | 30% | |

| 25% | 25% | 25% | 20% | 30% | |

|

| 10% | 20% | 30% | 15% | 30% |

| 25% | 25% | 26% | 15% | 25% | |

| 35% | 25% | 20% | 15% | 30% | |

| 5% | 20% | 40% | 15% | 40% | |

|

| 25% | 10% | 30% | 10% | $231/yr |

| 15% | 17% | 25% | 25% | 30% | |

| 15% | 13% | 10% | 8% | 30% | |

| 15% | 10% | 30% | 10% | 30% |

If you are wondering how much does car insurance cost in Minnesota and what does car insurance cover? We’re here to help you sort through the confusion by providing insight into all the data you need to make an informed decision about your car insurance provider and policy.

Minnesota Minimum Coverage Requirements

| Coverage Type | Typical Requirement |

|---|---|

| Bodily Injury Liability | $30,000 per person $60,000 per accident |

| Property Damage Liability | $10,000 per accident |

| Personal Injury Protection (PIP) | $40,000 total ($20,000 for medical expenses, $20,000 for non-medical expenses) |

| Uninsured/Underinsured Motorist Bodily Injury | $25,000 per person $50,000 per accident |

From the Minnesota Marine Art Museum to Minnesota’s North Shore Scenic Drive, there is a lot to see and do in the North Star State. This explains why there are approximately 5 million registered vehicles on the road in Minnesota. That is almost one car for every resident.

Uninsured Motorists 11.5

With so many cars on the road, there are bound to be some accidents. This could leave you with a massive headache if you are forced to navigate the claims process and car insurance premium laws on your own. Having the right car insurance provider on your side can help you cut through all the red tape and get things back to normal quickly, though.

How do you know that you have chosen the right provider? Keep reading to find out about some simple tips that can help you determine your car insurance provider with confidence.

Free Car Insurance Comparison

Compare Quotes From Top Companies and Save

Minnesota’s Car Culture

In the North Star State, the “Minnesota Nice” extends beyond the office or supermarket, and it is one of America’s safest driving cities. This is why many tourists and newcomers to the Minnesota car culture often remark about the lack of aggression displayed on Minnesota roadways.

Just because most Minnesotans aren’t as vocal as drivers in other states doesn’t mean that they aren’t silently judging your lack of driving ability, though. All jokes aside, residents of the North Star State are great people who desire to share the road and get from point A to point B with as little conflict or incident as possible.

Ensuring drivers in our state are licensed and carry insurance makes the roads safer for all Minnesotans. As a longtime supporter of Driver’s Licenses for All, I’ll be proud to sign this into law once it reaches my desk. https://t.co/8OxRkhfrUe

— Governor Tim Walz (@GovTimWalz) February 22, 2023

Harsh Minnesota winters can sometimes make this a near-impossible endeavor, but the Minnesota spirit is more complicated than anything that Mother Nature can throw at it. This hardy spirit has made residents of the North Star State savvy shoppers who want to get the most out of every dollar they spend.

This is why we’ve collected all the information you need in one place, so you can make the best decision for yourself and your loved ones when it’s time to purchase your car insurance policy.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Minnesota’s Minimum Coverage Requirements

Because driving conditions on the roads in Minnesota can sometimes be more hazardous than those in other places across the United States, the Minnesota Department of Public Safety (DPS), Minnesota Driver and Vehicle Service (DVS), and the state legislature have worked together to create the minimum car insurance requirements for drivers in the North Star State.

If you are wondering, how much insurance do I need for my car in Minnesota? These minimum mandatory requirements for liability coverage are as follows:

- $30,000 in bodily injury liability coverage for one person injured in an accident.

- $60,000 in bodily injury liability coverage for two or more people injured in an accident.

- $10,000 for property damages occurring as a result of an accident.

Minnesota also requires that you carry the following Personal Injury Protection coverage:

- $40,000 per person per accident

- $20,000 for medical expenses

- $20,000 to cover any other costs, such as lost wages that were incurred due to a car accident

The North Star State requirements don’t stop there. As a driver in Minnesota, you are also required to carry the following amounts in Uninsured and Underinsured Motorist Coverage:

- $25,000 to cover injuries to one person for both UM and UMI

- $50,000 to cover injuries to two or more people for UM and UMI

With so much coverage required by the North Star State, you will want to ensure that you are getting the most for your money when you purchase your car insurance policy. You will also want to ensure that you have the proper forms of financial responsibility in case you get pulled over or are involved in an accident.

Form of Financial Responsibility

The Minnesota Legislature has mandated that:

No motor carrier and no interstate carrier shall operate a vehicle until it has obtained and has in effect the minimum amount of financial responsibility required.

This is part of the statutes that define Minnesota’s financial responsibility laws. Simply put, the financial responsibility laws in the North Star State require all drivers to carry the minimum amount of coverage mandated by law and to have proof of insurance to demonstrate compliance. This is why forms of financial responsibility are often referred to as proof of insurance.

Read More: Why You Need Car Insurance

Drivers use them to prove that they have a valid car insurance policy or surety bond. A surety bond is also referred to as an SR-22 insurance form, and it may be required if you have an accident or other driving offenses on your record. If asked to provide proof of insurance in the North Star State, you can always present your physical policy, which will tell the demanding part that your policy is valid.

In the Land of 10,000 Lakes, you also have two other ways that you can prove that you are within the letter of the law, which are:

- An e-insurance card that can be accessed through your auto insurance provider’s app on your smartphone, laptop, tablet, or other electronic devices.

- A printed copy of your Insurance ID Card is usually mailed to you shortly after you purchase your policy, or it can be emailed to you so that you can print it out at your convenience.

Be aware that Minnesota does have penalties if you fail to present the proper proof of insurance. Some of these penalties may include:

- A misdemeanor charge

- A $200 fine

- Community service

Why would you risk it, though, when modern-day conveniences have made proving your financial responsibility so easy?

Percentage of Income Spent on Premiums

Now that you know what is expected of you as a driver on Minnesota’s roadways, it is time to start crunching numbers. According to Business Insider, Minnesota ranks 19th in the nation in terms of the amount Americans pay for car insurance premiums annually. The Insurance Information Institute (III) also ranks the North Star State 39th nationally for average auto insurance expenditures.

Without car insurance, one mistake on the road can wreck both your car and your bank account.Jeff Root Licensed Insurance Agent

This is good news for residents of the North Star State, as it means that the overall cost of car insurance in Minnesota is below the national average. Car insurance rates have remained relatively consistent as a percentage of income over the last few years. On average, around 2.01 percent of every Minnesotan’s annual disposable income is spent on car insurance.

With a per capita disposable income of $42,516 per year earned by residents of the North Star State and $875.49 of that being spent to maintain insurance on your vehicle, this means that the average cost for a Minnesotan is around $73 of their $3,543 monthly budget to drive in the Land of 10,00 Lakes.

The price of car insurance is also higher than in Wisconsin and Iowa, where residents pay around $717 and $684 per year for car insurance coverage. This is why it’s essential to get the best car insurance rates by city when shopping for your car insurance policy in the North Star State.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Additional Car Insurance Coverage in Minnesota

When deciding which car insurance provider is right for you, core coverage is not the only consideration. Sometimes it pays to have more auto insurance coverage than just what the state requires. This is why insurers in the North Star State provide you with the following additional coverage options:

- Umbrella Insurance: This type of liability coverage protects you if you find yourself being sued as a result of an accident, and the underlying policy limits have been exhausted.

- Collision Coverage: This addition to your policy covers you if you hit another vehicle, your vehicle is hit by someone else, you hit a stationary object, or your vehicle rolls over unintentionally.

- Comprehensive Coverage: This type of coverage protects you from damage caused by vandalism, theft, natural disasters, or animal strikes.

Given that animal strikes are common at certain times of the year in the North Star State, it could prove helpful to invest in additional liability options.

When deciding on additional coverage options, it is always a good idea to consider the loss ratio of the companies with which you are considering doing business. Take a look at the table below to see the loss ratio trends for Minnesota.

Minnesota Car Insurance Loss Ratios (2022–2024)

| Loss Ratio | 2022 | 2023 | 2024 |

|---|---|---|---|

| Personal Injury Protection | 70% | 68% | 66% |

| Medical Payments (MedPay) | 50% | 48% | 46% |

| Uninsured/Underinsured Motorist | 56% | 55% | 56% |

As you can see, Minnesota had made a significant turnaround in its MedPay loss ratio. What does this mean to you? It implies that Minnesota car insurance companies are constantly amending their business practices to improve the market’s overall health. Looking at the loss ratio trends gives you an indication of how the car insurance market as a whole is performing in the North Star State.

- A High Loss Ratio (over 100 percent) means that companies are losing money because they are paying out too many claims compared to the amount of premium they collect, which may cause them financial trouble in the long term.

- A Low Loss Ratio indicates that these companies might have over-priced their auto insurance policies or overestimated the number and severity of claims they expected to receive.

The gains in MedPay are excellent news for the health of Minnesota’s overall insurance market. The loss ratios for uninsured/underinsured motorists (UM/UIM) are also good news, considering that 11.5 percent of all drivers in the North Star State are uninsured, ranking Minnesota 27th in the nation.

Read More: Do I need full coverage on a financed car?

Add-ons and Endorsements for Car Insurance

Minnesotans have more than just insurance options for additional liability coverage. When purchasing your car insurance policy in the North Star State, you also have a variety of add-ons and endorsements to choose from.

The options can help you pay for things like a mechanical breakdown or renting a car, and they can help you protect yourself in the case of a total loss. Some of the most popular add-ons and endorsement options in the North Star State include:

- Guaranteed Auto Protection (GAP): If your car is ever stolen or totaled in an accident, this add-on can help you cover the loss by paying off the lease or loan.

- Rental Reimbursement: This handy add-on will help if you ever need a rental car while your car is being repaired after an accident.

- Emergency Roadside Assistance: Getting caught on the side of the road is no fun. This type of add-on can help alleviate some of the pain of getting a flat or needing a tow if your car breaks down while you’re driving.

- Non-Owner Car Insurance: Don’t own a car, but still enjoy driving occasionally? This add-on is perfect for you, then, because it offers liability coverage even if the vehicle you’re driving isn’t registered in your name.

- Mechanical Breakdown Insurance: This type of coverage can help you make up the difference in the cost of repair bills should you ever need help.

- Classic Car Insurance: Classic cars need special care and special coverage. This type of add-on is perfect for protecting your prized possession.

- Modified Car Insurance: If you like to soup up your wheels, this type of coverage can help cover the cost of repairing the modifications you have made should they become damaged in a crash.

The type of car you drive or the possibility of a mechanical breakdown are not the only things that you should consider as you construct a car insurance policy that suits all of your needs. Sometimes, just being who you are can affect how much MN’s auto insurance is, which is why it’s best to shop around. Keep reading to find out how you can help keep your rates down, no matter who you are.

MN’s Car Insurance Rates by Demographics

No matter your age or gender, most of us will eventually need to buy car insurance. When it’s time to make a purchase, you’ll want to know how these things will affect you.

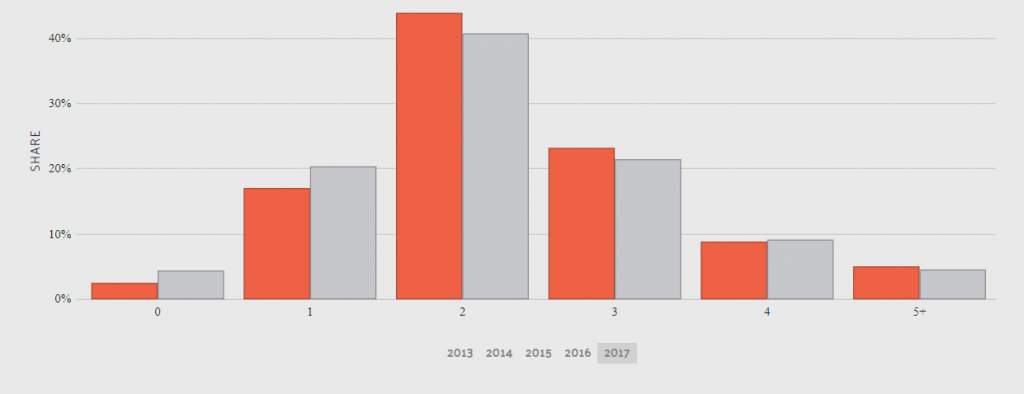

According to the Consumer Federation of America:

48 percent of Americans think auto insurers charge men more for coverage than women, while only 23 percent of mericans think that women are chargesd more.

The reality is that women are more likely to pay more, according to their 2017 study.

Minnesota Car Insurance Full Coverage Monthly Rates by Age & Gender

| Insurance Company | Age: 17 Female | Age: 17 Male | Age: 25 Female | Age: 25 Male | Age: 35 Female | Age: 35 Male | Age: 60 Female | Age: 60 Male |

|---|---|---|---|---|---|---|---|---|

| $574 | $831 | $356 | $372 | $252 | $252 | $272 | $272 |

| $507 | $734 | $170 | $196 | $186 | $186 | $149 | $149 | |

| $520 | $750 | $271 | $264 | $210 | $215 | $178 | $189 | |

| $462 | $587 | $200 | $216 | $222 | $220 | $155 | $147 | |

| $1,576 | $2,365 | $684 | $976 | $800 | $800 | $646 | $646 | |

| $510 | $745 | $192 | $199 | $190 | $195 | $134 | $144 | |

| $530 | $760 | $240 | $250 | $210 | $215 | $157 | $163 | |

| $278 | $342 | $143 | $118 | $129 | $129 | $104 | $104 | |

| $490 | $715 | $179 | $195 | $220 | $225 | $150 | $152 | |

| $420 | $460 | $167 | $176 | $158 | $157 | $109 | $108 |

As the table above shows, teenage drivers are still the most expensive people to insure, regardless of gender. The ability of MN’s car insurance companies to use gender as a factor for setting your rates is also a hotly debated issue among people, such as University of Minnesota Law School professor Daniel Schwarcz, who believes that:

If companies are not allowed to use “outdated stereotypes based on generalities” about men and women, the insurers will have to consider “more directly” such measures as the number if miles driven, the number of years customers have been driving, and where they live.

Many drivers agree with this as well. For now, age and gender are still allowed to be considered in the North Star State. They are not the only things under consideration, though. Some of those direct measures that Daniel Schwarcz discussed are factors as well.

Read More: How to Find a Safe, Budget-Friendly Car for Your Teen

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Car Insurance Rates by ZIP Code in Minnesota

Most people don’t realize that their car insurance rates can be impacted just by the neighborhood that they call home. Sometimes, just crossing the street into a new ZIP code can make a world of difference. Please take a look at the tables below to find out what we mean.

As the largest city in Minnesota, Minneapolis boasts no less than 68 ZIP codes. Not everyone in these ZIP codes pays the same for car insurance, though. The data reveals that Minneapolis residents who live near the U.S.

Minnesota 25 Most Expensive Car Insurance Full Coverage by ZIP Codes

| ZIP | City | Monthly Rate | Most Expensive Company | Most Expensive Rate | 2nd Expensive Company | 2nd Expensive Rate |

|---|---|---|---|---|---|---|

| 55411 | Minneapolis | $552 | Liberty Mutual | $1,745 | Allstate | $534 |

| 55106 | Saint Paul | $547 | Liberty Mutual | $1,748 | Allstate | $547 |

| 55101 | Saint Paul | $546 | Liberty Mutual | $1,748 | Allstate | $544 |

| 55103 | Saint Paul | $543 | Liberty Mutual | $1,748 | Allstate | $544 |

| 55404 | Minneapolis | $541 | Liberty Mutual | $1,745 | Allstate | $549 |

| 55412 | Minneapolis | $536 | Liberty Mutual | $1,745 | Allstate | $539 |

| 55107 | Saint Paul | $534 | Liberty Mutual | $1,748 | Allstate | $511 |

| 55454 | Minneapolis | $533 | Liberty Mutual | $1,745 | Allstate | $547 |

| 55415 | Minneapolis | $532 | Liberty Mutual | $1,745 | Allstate | $547 |

| 55407 | Minneapolis | $532 | Liberty Mutual | $1,696 | Allstate | $550 |

| 55408 | Minneapolis | $531 | Liberty Mutual | $1,745 | Allstate | $549 |

| 55402 | Minneapolis | $529 | Liberty Mutual | $1,745 | Allstate | $547 |

| 55455 | Minneapolis | $529 | Liberty Mutual | $1,745 | Allstate | $544 |

| 55104 | Saint Paul | $528 | Liberty Mutual | $1,696 | Allstate | $544 |

| 55405 | Minneapolis | $527 | Liberty Mutual | $1,745 | Allstate | $550 |

| 55406 | Minneapolis | $521 | Liberty Mutual | $1,696 | Allstate | $547 |

| 55414 | Minneapolis | $521 | Liberty Mutual | $1,696 | Allstate | $544 |

| 55403 | Minneapolis | $521 | Liberty Mutual | $1,745 | Allstate | $547 |

| 55413 | Minneapolis | $521 | Liberty Mutual | $1,745 | Allstate | $531 |

| 55401 | Minneapolis | $518 | Liberty Mutual | $1,745 | Allstate | $531 |

| 55114 | Saint Paul | $517 | Liberty Mutual | $1,696 | Allstate | $544 |

| 55102 | Saint Paul | $516 | Liberty Mutual | $1,696 | Allstate | $494 |

| 55409 | Minneapolis | $509 | Liberty Mutual | $1,696 | Allstate | $542 |

| 55130 | Saint Paul | $483 | Liberty Mutual | $1,193 | Allstate | $539 |

| 55450 | Minneapolis | $480 | Liberty Mutual | $1,745 | Allstate | $422 |

Bank Stadium pays an average of $6,385, while those who reside near North Commons Park pay almost $300 more. If you move into the Minneapolis neighborhood near Lyndale Farmstead Park, though, you will be paying about $200 less than those near U.S. Bank Stadium.

Minnesota 25 Cheapest Car Insurance Full Coverage Rates by ZIP Codes

| ZIP | City | Monthly Rates | Cheapest Company | Cheapest Monthly Rate | 2nd Cheapest Company | 2nd Cheapest Monthly Rate |

|---|---|---|---|---|---|---|

| 56007 | Albert Lea | $331 | State Farm | $152 | Nationwide | $199 |

| 56088 | Truman | $332 | State Farm | $139 | Farmers | $204 |

| 56120 | Butterfield | $334 | State Farm | $141 | USAA | $203 |

| 55912 | Austin | $334 | State Farm | $155 | USAA | $209 |

| 56159 | Mountain Lake | $335 | State Farm | $145 | USAA | $203 |

| 55987 | Winona | $335 | State Farm | $159 | Nationwide | $207 |

| 56039 | Granada | $335 | State Farm | $137 | Nationwide | $211 |

| 56027 | Elmore | $335 | State Farm | $136 | Farmers | $199 |

| 56073 | New Ulm | $336 | State Farm | $139 | USAA | $203 |

| 56181 | Welcome | $336 | State Farm | $140 | Nationwide | $211 |

| 56062 | Madelia | $336 | State Farm | $142 | USAA | $203 |

| 56031 | Fairmont | $336 | State Farm | $137 | Nationwide | $211 |

| 56127 | Dunnell | $336 | State Farm | $147 | Farmers | $204 |

| 56087 | Springfield | $336 | State Farm | $142 | USAA | $203 |

| 56054 | Lafayette | $336 | State Farm | $148 | Farmers | $215 |

| 56081 | Saint James | $336 | State Farm | $142 | USAA | $203 |

| 56075 | Northrop | $336 | State Farm | $157 | Nationwide | $211 |

| 56098 | Winnebago | $336 | State Farm | $143 | Farmers | $203 |

| 56019 | Comfrey | $337 | State Farm | $139 | USAA | $203 |

| 56041 | Hanska | $337 | State Farm | $140 | USAA | $203 |

| 56001 | Mankato | $337 | State Farm | $168 | Nationwide | $218 |

| 56085 | Sleepy Eye | $337 | State Farm | $136 | USAA | $203 |

| 56036 | Glenville | $337 | State Farm | $153 | Farmers | $201 |

| 56171 | Sherburn | $337 | State Farm | $143 | Nationwide | $211 |

| 56162 | Ormsby | $337 | State Farm | $157 | Nationwide | $211 |

Your neighborhood is not the only geographic factor that car insurance companies consider when determining how much you will pay for your policy. Sometimes, the city that you love can cost you big bucks as well.

Read More: Most Expensive Tolls in America

Cheapest Car Insurance Rates by City in Minnesota

From sights along the Mighty Mississippi as it meanders through Minneapolis-St. Paul Paul, to the tiny town of Funkley, where Funkley Bar becomes City Hall when the City Council meets, the North Star State has some of the most beautiful and interesting cities in the nation. Learn more about 15 startling facts about America’s infrastructure.

This is why having the correct information in your hands as you determine which car insurance provider is right for you could help you avoid a costly mistake when investing in your policy. We’ve put together research that can help you invest wisely. Please take a look at the tables below to see what residents of your hometown are paying for their car insurance policies.

Minnesota 25 Cheapest Auto Insurance Full Coverage by City

| City | Monthly Rate | Cheapest Company | Cheapest Monthly Rate | 2nd Cheapest Company | 2nd Cheapest Monthly Rate |

|---|---|---|---|---|---|

| Albert Lea | $331 | State Farm | $152 | Nationwide | $199 |

| Truman | $332 | State Farm | $139 | Farmers | $204 |

| Butterfield | $334 | State Farm | $141 | USAA | $203 |

| Austin | $334 | State Farm | $155 | USAA | $209 |

| Mountain Lake | $335 | State Farm | $145 | USAA | $203 |

| Goodview | $335 | State Farm | $159 | Nationwide | $207 |

| Granada | $335 | State Farm | $137 | Nationwide | $211 |

| Elmore | $335 | State Farm | $136 | Farmers | $199 |

| New Ulm | $336 | State Farm | $139 | USAA | $203 |

| Welcome | $336 | State Farm | $140 | Nationwide | $211 |

| Madelia | $336 | State Farm | $142 | USAA | $203 |

| Fairmont | $336 | State Farm | $137 | Nationwide | $211 |

| Dunnell | $336 | State Farm | $147 | Farmers | $204 |

| Springfield | $336 | State Farm | $142 | USAA | $203 |

| Lafayette | $336 | State Farm | $148 | Farmers | $215 |

| St. James | $336 | State Farm | $142 | USAA | $203 |

| Northrop | $336 | State Farm | $157 | Nationwide | $211 |

| Winnebago | $336 | State Farm | $143 | Farmers | $203 |

| Comfrey | $337 | State Farm | $139 | USAA | $203 |

| Hanska | $337 | State Farm | $140 | USAA | $203 |

| Sleepy Eye | $337 | State Farm | $136 | USAA | $203 |

| Glenville | $337 | State Farm | $153 | Farmers | $201 |

| Sherburn | $337 | State Farm | $143 | Nationwide | $211 |

| Ormsby | $337 | State Farm | $157 | Nationwide | $211 |

| Lewisville | $338 | State Farm | $143 | USAA | $203 |

With a population of around 18,000, it’s no wonder that car insurance rates in Albert Lea are lower compared to the sprawling city of Minneapolis, where Minnesotans pay an average of over $2,000 more.

Minnesota 25 Most Expensive Auto Insurance Full Coverage by City

| City | Monthly Rate | Most Expensive Company | Most Expensive Monthly Rate | 2nd Expensive Company | 2nd Expensive Monthly Rate |

|---|---|---|---|---|---|

| Minneapolis | $509 | Liberty Mutual | $1,647 | Allstate | $523 |

| St. Paul | $498 | Liberty Mutual | $1,543 | Allstate | $512 |

| Little Canada | $450 | Liberty Mutual | $1,193 | Allstate | $495 |

| Brooklyn Center | $438 | Liberty Mutual | $1,144 | Allstate | $460 |

| Falcon Heights | $426 | Liberty Mutual | $1,199 | Allstate | $467 |

| Columbia Heights | $425 | Liberty Mutual | $1,144 | Allstate | $454 |

| Maplewood | $422 | Liberty Mutual | $1,193 | Allstate | $449 |

| Waskish | $419 | Liberty Mutual | $1,269 | Farmers | $380 |

| St. Francis | $417 | Liberty Mutual | $1,258 | Allstate | $393 |

| Martin Lake | $417 | Liberty Mutual | $1,258 | Allstate | $393 |

| Richfield | $417 | Liberty Mutual | $1,195 | Allstate | $442 |

| Lake George | $417 | Liberty Mutual | $1,269 | Farmers | $374 |

| South St. Paul | $416 | Liberty Mutual | $1,193 | Allstate | $444 |

| Columbus | $416 | Liberty Mutual | $1,258 | Allstate | $397 |

| Bethel | $415 | Liberty Mutual | $1,258 | Allstate | $393 |

| East Bethel | $415 | Liberty Mutual | $1,258 | Allstate | $393 |

| Fridley | $414 | Liberty Mutual | $1,144 | Allstate | $458 |

| Almelund | $414 | Liberty Mutual | $1,258 | Allstate | $419 |

| Isanti | $413 | Liberty Mutual | $1,258 | Allstate | $399 |

| Garrison | $412 | Liberty Mutual | $1,269 | Allstate | $378 |

| Andover | $412 | Liberty Mutual | $1,258 | Allstate | $423 |

| Grandy | $412 | Liberty Mutual | $1,258 | Allstate | $398 |

| Swatara | $412 | Liberty Mutual | $1,269 | Allstate | $374 |

| Taylors Falls | $412 | Liberty Mutual | $1,258 | Allstate | $419 |

| Centerville | $412 | Liberty Mutual | $1,258 | Allstate | $411 |

More people mean more cars on the road, which explains the drastic difference in premium prices between Albert Lea and Minneapolis, since more cars usually translate into more accidents.

With more accidents come more claims filed against car insurance companies, leading to higher rates for everyone. Should you ever find yourself in the unfortunate position of needing to file a claim, you will want a great car insurance provider on your side.

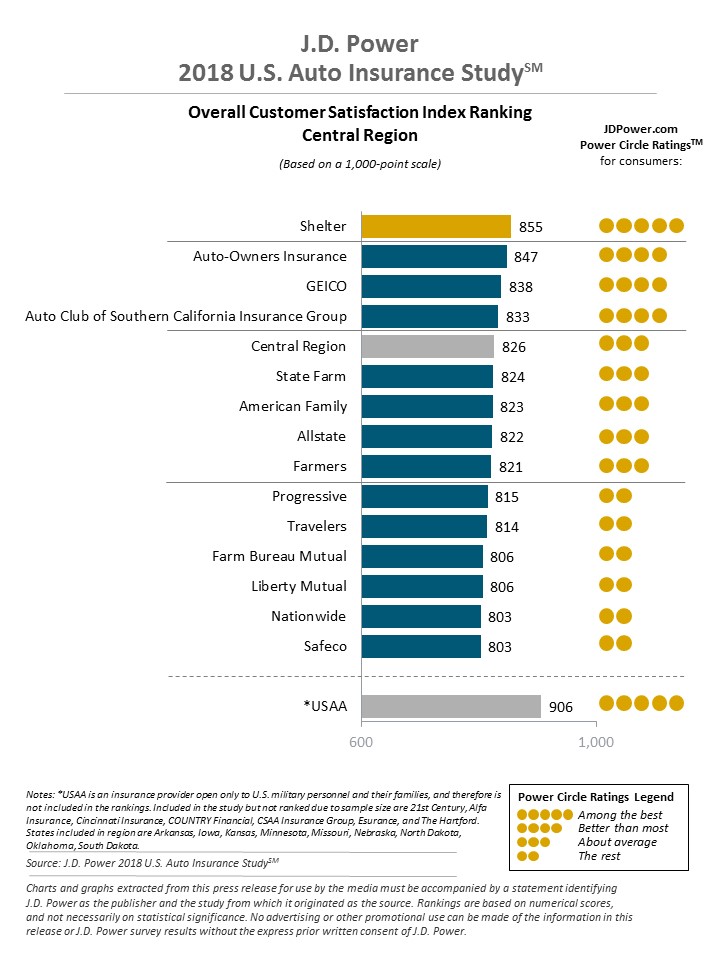

Minnesota’s Best Car Insurance Companies

With so many auto insurance companies in Minnesota, it can be difficult to determine which provider is right for you. Having trusted agencies like A.M. Best and JD Power look out for you makes it easier, though. Take a look at what they have to say about the best car insurance companies in the North Star State.

As the only worldwide company with a singular focus on the insurance market, A.M. Best has become one of the most trusted agencies in the global insurance industry, used by organizations such as the National Association of Insurance Commissioners (NAIC). The table below shows you how they have rated the biggest insurance providers in the North Star State.

Car Insurance Companies by A.M. Best and Outlook

| Best Rated Companies | A.M. Best | Outlook |

|---|---|---|

|

| A+ | Stable |

| A | Stable | |

| A | Stable | |

| A++ | Stable | |

| A | Stable | |

| A+ | Stable | |

| A+ | Stable | |

| A++ | Stable | |

| A++ | Stable | |

| A++ | Stable |

When you choose a company that has been given an A++ rating and/or a stable outlook by A.M. Best, you are choosing a company that has a good loss ratio and a great outlook for future growth and prosperity. Understanding a company’s financial stability and loss ratio can help you choose a car insurance provider that will be more likely to pay out your claim should you ever need to file one.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Companies With the Best Car Insurance Ratings

Just like A.M. Best has your back when it comes to understanding the car insurance market and its overall viability, so too does JD Power.

What they have found is that customer satisfaction ratings with car insurance providers are at a record high.  Buying car insurance in Minnesota isn’t always as great as the perfect pan of Hot Dish. Making sure you have all the information you need to make an informed decision before purchasing your car insurance policy can make the experience more pleasant.

Buying car insurance in Minnesota isn’t always as great as the perfect pan of Hot Dish. Making sure you have all the information you need to make an informed decision before purchasing your car insurance policy can make the experience more pleasant.

Companies With the Most Complaints

Before choosing a car insurance provider to help protect you and your family, it’s a good idea to find out their complaint ratio. This complaint ratio can help you determine where each car insurance provider in your area stands in relation to its competitors. This can save you money by giving you insight into who is competing for your business.

The complaint ratio’s baseline is 1.0. This means that the higher the complaint ratio is above the baseline of 1.0, the more complaints there are against a car insurance company. Below is a list of the top ten car insurance companies in the North Star State, along with their complaint ratios, so you can see how each one performs.

Minnesota Largest Companies Complaint Ratios

| Insurance Company | Direct Premiums Written | Complaint Ratio | Loss Ratio | Market Share |

|---|---|---|---|---|

|

| $200,235 | 0.5 | 60.51% | 5.56% |

| $418,487 | 0.79 | 62.97% | 11.62% | |

| $212,804 | 0 | 56.43% | 5.91% | |

| $129,987 | 0.68 | 74.00% | 3.61% | |

| $110,671 | 5.95 | 60.04% | 3.07% | |

| $5,413,758 | 0.74 | 73.57% | 1.70% | |

| $586,357 | 0.75 | 62.53% | 16.27% | |

| $891,085 | 0.44 | 65.52% | 24.73% | |

| $106,222 | 0.09 | 65.96% | 2.95% | |

| $110,895 | 0.74 | 73.57% | 3.08% |

Don’t let the raw numbers fool you. Just because a company has a high complaint ratio doesn’t mean it’s a bad company to do business with. To get a fuller picture of the complaint ratio, you have to consider the company’s market share.

Looking at the table in this light reveals that although American Family Insurance Group has a complaint ratio that is a bit on the high side also has a higher portion of the market share.

More market share means more customers, which means a higher possibility for complaints overall. We truly hope that you never need to file a complaint against your car insurance provider, but if it should come to that, the state of Minnesota has a few ways for you to do so. Some of these ways include:

- Online at https://mn.gov/commerce/consumers/file-a-complaint/

- Email your questions to [email protected]

- By Mail at 85 7th Place East, Suite 500, St. Paul, MN 55101

Now that you are gaining a better grasp of how to use the loss ratio and complaint ratio to negotiate a better price on your car insurance policy, it is time to start looking at what those companies are charging for coverage.

The Cheapest Car Insurance Companies in Minnesota

Every good shopper knows that you never take the first price given to you if you can help it. Being able to haggle means knowing what competitors charge for the same goods or services on the market. We are here to help you with that. The table below gives you a glimpse into what the biggest competitors in your area are charging on average.

This information can help you gain the upper hand in lowering your car insurance cost.

Car Insurance Rates in Minnesota

| Company | Monthly Premium | +/- Compared to State Average (Rate) | +/- Compared to State Average (%) |

|---|---|---|---|

|

| $378 | +$19 | 0% |

| $293 | -$992 | 0% | |

| $261 | -$1,376 | 0% | |

| $292 | -$1,015 | 0% | |

| $1,130 | +$9,050 | +1% | |

| $114 | -$2,169 | -1% | |

| $244 | -$1,587 | -1% | |

| $172 | -$2,447 | -1% | |

| $118 | -$2,089 | -1% | |

| $239 | -$1,652 | -1% |

Knowing how far your dollar will stretch with each competitor on the market can help you save money. Before you become a customer, though, you will want to know how each of these companies determines your rates. We have talked a little about your age and gender, as well as how where you live can impact your rates.

Did you know that how much you drive can also play a role in how companies decide how much they should charge you? Keep reading to find out more.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Commute Rates by Company in Minnesota

Driving is mostly a game of chance. One thing that you can pretty much count on, though, is the fact that the more you drive, the higher your insurance premiums will most likely be. This is why it pays big dividends sometimes to shop before you buy.

Across the country, car insurance providers charge customers based on the number of miles they travel annually, and looking at the numbers reveals that residents of the North Star State really are on the go.

Read More: How to Drive Safely, No Matter the Time of Day

More people on the roads means a greater chance of traffic incidents, which can lead to higher rates. This is why car insurance providers consider how much you drive when determining your premiums.

Car Insurance Monthly Rates in Minnesota by Annual Mileage

| Company | 6,000 Miles | 12,000 Miles |

|---|---|---|

|

| $378 | $378 |

| $290 | $297 | |

| $261 | $261 | |

| $288 | $296 | |

| $1,097 | $1,163 | |

| $244 | $244 | |

| $244 | $254 | |

| $168 | $177 | |

| $175 | $184 | |

| $235 | $242 |

The table reveals that car insurance companies in Minnesota are pretty fair when it comes to charging you for every mile you drive. This is where a fine eye for detail comes in, though. Choosing a company like State Farm or USAA could save you money no matter how long your commute is because they are both the lowest-priced carriers in this category, and their rates do not fluctuate much with every mile you put behind you.

Keep in mind, though, that these companies might also have a complaint or loss ratio that might cause you to reconsider, so getting all of your ducks in a row before targeting an insurance provider is always the best decision.

The Coverage Level Rates by Company in Minnesota

Understanding where you live, who you are, and how healthy a particular car insurance company might be is only part of the process of purchasing your car insurance policy. You will also need to consider how much coverage you need and find out what that coverage will cost you. The table below can help you get started.

Car Insurance Monthly Rate in Minnesota by Coverage Level for Top Providers

| Company | Low Coverage | Medium Coverage | High Coverage |

|---|---|---|---|

|

| $372 | $377 | $383 |

| $293 | $302 | $286 | |

| $252 | $263 | $270 | |

| $283 | $291 | $300 | |

| $1,103 | $1,131 | $1,156 | |

| $231 | $246 | $256 | |

| $244 | $258 | $272 | |

| $165 | $173 | $179 | |

| $171 | $180 | $187 | |

| $232 | $238 | $246 |

It goes without saying that the higher your coverage level, the more money you will pay for car insurance premiums. That is not all there is to it, though. For instance, a new car may require more coverage, while an older car with high mileage might require less.

The price for this coverage may also be influenced by other factors, such as where you live or the length of your commute. Another factor is your driving record, of course. But did you know that things like your education level and credit score can also impact how much you pay? Keep reading to find out how to get affordable car insurance in Minnesota.

Credit-Based Insurance Rates in Minnesota

Your actions on the road are some of the things you do that can raise your premiums. However, your financial habits can also play a significant role. According to a 2015 article published by Consumer Reports, car dealerships and credit card companies use your credit score to determine your risk level:

Car insurers are also rifling through your credit files to…predict the odds that you’ll file a claim.

This means that too many unpaid or delinquent bills on your credit report could cost you big time when it comes time to purchase your car insurance policy.

Car Insurance Monthly Rates in Minnesota by Provider & Credit Score

| Company | Good Credit | Fair Credit | Poor Credit |

|---|---|---|---|

|

| $279 | $300 | $554 |

| $214 | $266 | $401 | |

| $221 | $237 | $326 | |

| $239 | $286 | $350 | |

| $796 | $1,019 | $1,576 | |

| $208 | $234 | $290 | |

| $210 | $256 | $408 | |

| $112 | $154 | $251 | |

| $198 | $235 | $359 | |

| $159 | $183 | $374 |

People with better credit scores get better rates on car insurance because the insurance provider assumes that if a person with good credit has an accident, they will most likely pay out of pocket rather than file a claim. This doesn’t mean that maintaining a clean driving record doesn’t have its advantages, though.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Driving Record Rates by Company in Minnesota

Safe driving means checking your bad attitude at the car door. Your behavior behind the wheel can also cost you more money when it comes time to invest in car insurance. Take a look at the table below to see how.

Car Insurance Monthly Rates in Minnesota by Provider & Driving Record

| Company | Clean Record | One Ticket | One Accident | One DUI |

|---|---|---|---|---|

|

| $274 | $360 | $398 | $478 |

| $197 | $224 | $355 | $398 | |

| $224 | $254 | $282 | $286 | |

| $193 | $207 | $308 | $458 | |

| $830 | $895 | $1,137 | $1,659 | |

| $194 | $229 | $257 | $296 | |

| $202 | $238 | $312 | $380 | |

| $158 | $172 | $186 | $172 | |

| $189 | $217 | $284 | $342 | |

| $177 | $211 | $226 | $340 |

The drastic difference in rates between a driver with a clean record and one who has had one speeding ticket or accident illustrates the importance of exercising good driving habits on Minnesota roadways. If you think your driving skills need work, the North Star State also has a list of approved accident prevention courses.

You can also request a certified copy of your Minnesota driving record by printing out the request form and mailing it to the Driver and Vehicle Services Unit at 445 Minnesota Street, Suite 161, St. Paul, MN, 55101-5161. You can also request one online for your convenience.

Largest Car Insurance Providers in Minnesota

We have talked a little bit about market share, which is the percentage of the overall market that a particular car insurance company controls.

Market share is much more than that, though. It is the key to understanding how loss ratios and complaint ratios work to save you money on car insurance by examining how market share relates to direct premiums written.

Car Insurance Companies in Minnesota by Market Share

| Insurance Company | Direct Premiums Written | Market Share |

|---|---|---|

| $891,085 | 24.73% | |

| $586,357 | 16.27% | |

| $418,487 | 11.62% | |

| $212,804 | 5.91% | |

|

| $200,235 | 5.56% |

| $129,987 | 3.61% | |

| $125,000 | 3.47% | |

| $110,895 | 3.08% | |

| $110,671 | 3.07% | |

| $106,222 | 2.95% |

As the table shows, State Farm has the largest share of the Minnesota car insurance market, with almost $900,000 in Direct Premiums Written. This indicates that the car insurance market as a whole is pretty healthy in the North Star State, which translates into safety for you as a consumer once you purchase your car insurance policy.

These companies write new policies as a means of growth rather than raising their rates to increase their bottom line.

Number of Insurers in Minnesota

Minnesota has 39 domestic insurers and 816 foreign insurers, all operating in the State. That is 855 options for car insurance companies in the Land of 10,000 Lakes. So, what is the difference between the two? Simply states:

- A domestic insurer is one that has been formed under the laws of a state, such as Minnesota.

- A foreign insurer is one formed under the laws of any state, district, territory, or commonwealth of the United States other than the state of Minnesota.

Both types of insurers must adhere to the laws governing car insurance providers in the North Star State, regardless of their location. The choice between one or the other is a personal one. Dealing with either type of insurer is easier, though, when you understand the laws under which they are formed and the ones that they must comply with.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Minnesota State Laws on Car Insurance

Trying to navigate your way through all of the laws that govern car insurance in the North Star State can be a confusing and frustrating task. Attempting to understand just which laws apply to whom after an accident can complicate things even more. Gaining a good grasp of these laws before you are ever involved in an accident can help. This is where we come in.

Ensuring drivers in Minnesota are licensed and carry insurance makes the roads safer for everyone.

As a longtime supporter of Driver’s Licenses for All, I’m proud to sign it into law as we move toward making Minnesota a safe state for all.

— Governor Tim Walz (@GovTimWalz) March 7, 2023

We are here to guide you through the ins and outs of Minnesota laws concerning car insurance so that you’ll know your rights and what to do when you get pulled over.

Did you know that there are insurance requirements for registering a vehicle and age-related factors for getting your driver’s license in Minnesota, too? Almost every aspect of vehicle ownership and operation in the North Star State is regulated to protect drivers, passengers, and the general public from injury, loss, or damage.

Determining State Laws

You may be wondering just who is responsible for writing the laws that govern car ownership, vehicle registration, and driver’s licenses in the Land of 10,000 Lakes. Like all other laws in Minnesota, laws and regulations for these things begin in the various chambers and subcommittees that make up the Minnesota State Legislature.

The State Legislature, in conjunction with the Minnesota Department of Commerce and the Minnesota Department of Transportation, has determined the various safety, vehicle registration, driver’s license, and insurance laws in the North Star State. Chief among these is that Minnesota has been designated a “No-Fault” state. What this means is that:

Certain expenses resulting from the personal injuries of a car owner, the owner’s family, and the driver and occupants of the owner’s car are paid by the car owner’s insurance company regardless of who is at fault in causing an auto accident.

This system is designed to minimize the delay in paying for medical or rehabilitation services after an accident. After the passage of laws that designated Minnesota as a “No-Fault” state, companies operating in the North Star State were required to sign the No-Fault Certificate Form. This form stated that:

These companies formally agreed to provide Minnesota no-fault benefits to their non-Minnesota insureds if those insureds are involved in an accident while driving their vehicle in Minnesota.

This means that all drivers and passengers involved in a car accident with a driver from Minnesota will be covered.

Getting Windshield Coverage

Should I use insurance to replace my windshield? Damage to your windshield is also covered under certain provisions within your standard car insurance policy. This is important to know, considering that in Minnesota:

It is illegal to drive a vehicle if the windshield is discolored or cracked in a way that limits the driver’s clear view.

If you are found to be in violation, you may be subject to citations and fees. When it’s time to repair your windshield, you have the right to choose who provides the service. Keep in mind, though, that if you choose a vendor who is not preferred by your car insurance provider, you might be stuck paying the difference in cost.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Getting High-Risk Auto Insurance

The more tickets, accidents, and claims you have, the higher your rates will be. That is just an unavoidable fact of driving, no matter which state you live in. If you live in the North Star State, though, you could be required to obtain an SR-22 form if you are determined to be a high-risk driver.

While Minnesota does not require the SR-22 form, you may be required to obtain a certificate of insurance to reinstate your license if it has been revoked. The North Star State also has the Minnesota Automobile Insurance Plan, which is meant to provide insurance for drivers who cannot obtain car insurance on the open market due to the risk that they pose to car insurance providers.

Read More: How much is a ticket for driving without a license?

Getting Low-Cost Insurance

Drivers who pose a greater risk to insurance companies’ bottom lines are not the only ones who have specific protections under Minnesota state laws and provisions.

In the Land of 10,000 Lakes, the Minnesota Automobile Insurance Plan also helps drivers find a fair price on low-income car insurance in Minnesota.

Automobile Insurance Fraud

Because Minnesota is a no-fault state, the chances of insurance fraud being committed in the North Star State are increased. In fact, according to Consumer Watchdog:

No-fault’s mandatory payments create incentives to increase medical treatment and encourage fraud for those people without other forms of health coverage.

This increase in fraudulent claims is one reason why car insurance rates in no-fault states like Minnesota are generally higher. Some opponents of the no-fault system also believe that limiting a person’s responsibility for their poor driving habits encourages them to behave recklessly behind the wheel, since the financial responsibility for causing an accident will not fall on them as the at-fault driver.

Reckless drivers or people without health insurance are not the only ones who may be responsible for committing fraud. According to III, fraud may also be committed by:

- Applicants for insurance

- Policy-holders

- Third-party claimants

- Doctors or other healthcare professionals who might inflate the billing costs

- Repair shops and mechanics who claim damage in excess of what is actually present, or who claim previous damages on a new claim

These are just some of the people or vendors who might be liable for committing insurance fraud. To be safe, you should always keep track of all transactions and billing invoices after a car accident. Penalties for committing insurance fraud could include:

- 90 days in jail and a fine of up to $1,000 for a charge of fraud where the value is up to $500

- Up to 5 years in jail and a fine of no more than $10,000 for a charge of fraud where the value is between $1,000 and $5,000

- Up to 10 years imprisonment and a fine of up to $20,000 for a charge of fraud where the value is between $5,000 and $35,000

- 20 years in prison and a fine of up to $100,000 for a charge of fraud where the value is more than $35,000

If you think that you have been the victim of fraud, you can visit the Minnesota Attorney General’s website and report it to the authorities.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Statute of Limitations

The statute of limitations on claims of car insurance fraud begins the moment a loss occurs and lasts 7 years. Fraud cases are not the only things that have a statute of limitations, though. There is also a statute of limitations on how long you have to report a claim after a traffic accident or incident.

NOLO states that if you are injured in a car accident, you have a two-year statute of limitations to file a claim, which begins to run from the date of the accident. Wrongful death claims have a three-year statute of limitations that also starts to run from the date of the accident.

Specific Minnesota Driving Laws

Minnesotans aren’t serious all of the time, as the law that states that you can not cross state lines with a duck on your head proves. The North Star state also has a strange law that says that all bathtubs must have feet. You are also not allowed to park your elephant on Main Street. Okay, so the last one was just an old Minnesota urban legend. See more in this guide for traffic citations.

Standing on the sidelines ❌

Saving with Progressive ✅ pic.twitter.com/7tbCtdJsmf— Progressive (@progressive) February 15, 2025

A law that is not an urban legend states that it is perfectly legal to drive in reverse without wearing a seatbelt. It is illegal, though, to drive down Lake Street in Minneapolis in a red car. Zipper-merging is not the law, though, but it is strongly recommended by MnDOT. There are many other general traffic regulations in Minnesota, which can be found in more detail on the Minnesota Legislature website.

Vehicle Licensing Laws in Minnesota

Minnesota does not just have general traffic regulations or car insurance laws on the books. The North Star State also has laws that determine the vehicle registration requirements in the Land of 10,000 Lakes. Some of these requirements may include the following:

- Presenting the foreign state title of a vehicle previously registered or purchased out-of-state

- Providing an odometer reading

- Presenting your driver’s license or state-issued ID

- And presenting proof of insurance

The North Star State also participates in the REAL ID program, which requires that you bring specific forms of identification when seeking your Minnesota driver’s license or state ID with the REAL ID endorsement attached to it.

The Minnesota DVS website has a printable version of the REAL ID identification and accepted documents list (Read More: Can I get car insurance with no license?).

Penalties for Driving Without Insurance

Just like there are penalties for driving with an expired tag in Minnesota, there are also penalties for driving without car insurance. For your first offense, you could be fined between $200 and $ 1,000 or be required to perform community service. You could also face up to 90 days in prison.

Why risk it, though, when you have all of the information you need right here to make an educated decision that could save you money when purchasing your car insurance policy? Should you get pulled over or need to prove that you have car insurance to register a vehicle, the North Star State allows you to use the following ways to prove your financial responsibility:

- A printed car insurance ID card

- An e-insurance card that can be presented on your cell phone or other handheld devices

In addition to laws governing vehicle registration requirements in Minnesota, the North Star State also regulates who can become a licensed driver.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Teen Driver Laws

Most teenagers can’t wait to experience the freedom that the open road provides. In Minnesota, though, that freedom has limits. Some of these limits dictate the hours that teenagers can be on the road. For instance, for the first 6 months of licensure, a teenager can not drive between the hours of 12 a.m. and 5 a.m.

Read More: Learner’s Permit Insurance Coverage

There are also passenger limits for the first 6 months, which limit the number of passengers in a teenage driver’s car to one person under the age of 20. For the second 6 months, that limit increases to 3. Cell phone use and texting are also completely illegal for drivers under 18, except when making a 911 call.

Teen drivers are at a higher risk for accidents due to less driving experience. If you have a first-time driver at home, reduce your stress by understanding their #autoinsurance policy and reinforcing safe driving behaviors: https://t.co/fLyKCNIbIe#TeenDriverSafetyWeek pic.twitter.com/CdWzscKrh0

— Insurance Information Institute (@iiiorg) October 23, 2024

Any underage driver who is caught drinking and driving is also subject to the regular DWI laws and sanctions mandated by the state of Minnesota. Teenagers in Minnesota can obtain their Instructional Permit at age 15 with parental consent. This type of license requires that a licensed adult over 21 be present in the vehicle when it is in operation.

At 16 years of age, a Minnesota teen can apply for a Provisional License. They must have 40 hours of logged supervised driving time prior to applying. The person who signed the driving log must also have completed a 90-minute supplemental parent-child curriculum, unless the teenager has logged 50 hours of practice driving.

A full, unrestricted driver’s license becomes an option upon the teenager’s 18th birthday. This is, of course, if the teenager does not have any legal restrictions on their driving record, such as suspensions or revocations.

Driver’s License Renewal Procedures

Teen drivers are not the only ones with restrictions on obtaining and maintaining their driver’s licenses in the North Star State. Failing to renew a driver’s license may lead to traffic citations. The general population is required to renew their Minnesota driver’s license every four years. It must do so in person each time, as they must prove they have adequate vision to operate a motor vehicle.

Older drivers are also subject to the same renewal regulations. The Minnesota Office of Traffic Safety offers a four-hour Defensive Driving Training Course for people over age 55 at various locations.

The Minnesota Department of Public Safety offers tips and considerations for older drivers and their family members who may be concerned about driving safety in Minnesota.

The Hartford also offers tips for talking to aging family members about the possibility that they might not be the safest when they are behind the wheel. Getting older doesn’t mean that you become a bad driver. It just means that, as the Minnesota Office of Traffic Safety points out:

Older drivers are more likely to get killed or injured because they are more likely to become physically fragile and less able to recover from injuries.

The Minnesota Office of Traffic Safety also notes that one out of every four traffic fatalities in Minnesota is a person over the age of 65, so be careful out there.

MN New Residents Procedure for Car Insurance

Teenage drivers and older Minnesotans are not the only ones subject to specific license renewal procedures for driving laws. New residents of the North Star State must also meet their requirements to become legally sanctioned drivers in Minnesota. According to the Minnesota Department of Human Services, you are considered a resident of Minnesota based on the following criteria:

- If you are physically present in the state

- If you reside in Minnesota voluntarily and do not maintain a home elsewhere, and have done so for 30 days

The Minnesota Department of Public Safety then requires that you obtain insurance before registering your vehicle in the North Star State and that you pass a knowledge test regarding Minnesota’s driving laws if you have a valid license from another state. As a new resident, you will need to:

- Complete the Minnesota Driver’s License Application

- Present one primary and one secondary form of identification

- Present your license from your previous state of residence

- Pass the vision test

If you would like to study the Minnesota driving laws before attempting to obtain your driver’s license in the North Star State, the Minnesota DVS has an online driver’s handbook to help you.

Now that you know how to get your driver’s license and register your vehicle, it is time for us to help you understand how to keep them in good standing. Learn if you can insure a car that is not in your name.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Negligent Operator Treatment System

Unlike most states, Minnesota does not operate under a point system. Instead, the North Star State depends on the Minnesota Safe and Sober Campaign, just because the North Star State does not mean that you can drive like a maniac.

The Minnesota Department of Driver and Vehicle Services will still suspend your driver’s license if you get too many moving violations in a specified amount of time. The Minnesota DVS considers the following as major violations:

- Reckless Driving

- Not carrying enough insurance

- Driving under the Influence (DUI)

Minnesota DVS also considers the following as non-moving violations but still ticket-worthy offenses:

- Inattentive driving

- Driving while talking on your cell phone

- Driving without a seatbelt

If your driver’s license is suspended or revoked, you can visit the Minnesota DVS online portal to pay the reinstatement fees.

The Rules of the Road

Don’t let Minnesota’s lack of a point system fool you. If you get too many tickets or have too many accidents, your car insurance rates will go up. This is an inevitable rule of the road. There are also plenty of other rules for driving on Minnesota’s roadways.

Read More: Citation vs. Ticket: Are they the same thing?

Knowing what these rules are and following them can help you significantly when it’s time to purchase your car insurance policy. Keep scrolling to find out all the information you need to be a well-informed and safe driver when out on the Minnesota highway.

Minnesota: A No-Fault or At-Fault State

You already know that Minnesota is a no-fault state. What does this mean to you, though, if you are ever involved in an accident? What this means to you as a driver in the North State is that if you are ever in an accident, your car insurance coverage will be responsible for paying your medical bills, regardless of who caused the crash.

These bills will be paid out of your Personal Injury Protection (PIP) coverage benefits. Under PIP, you can not get paid for pain and suffering or any other non-monetary damages. According to NOLO:

No-Fault/PIP also does not appply to a motorcyclist’s injuries after and accident in Minnesota.

These rules are vastly different from those in an at-fault state, where all medical and damage payments are initially made by the insurance company of the driver deemed at fault in a car accident.

Whether you live in a no-fault state like Minnesota or an at-fault state like Texas, there are certain rules of the road that cross state lines. Seatbelt laws are among these. The requirements and penalties vary by state, though.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Seatbelt and Car Seat Laws in Minnesota

According to the Insurance Institute for Highway Safety (IIHS), driving without a seatbelt is a primary offense as of June 6, 2009. This means that you can be pulled over and ticketed for no other reason than other than not having yourself or your passengers properly secured by a seatbelt or child safety restraint device.

Minnesota law requires that children 7 years or younger who are more than 57 inches tall wear a seatbelt at all times. The fine for failing to comply is $25. If the child is less than 8 years old and less than 57 inches tall, they must be in a child safety seat. If you break this law, you will be fined $50.

Should wearing your seatbelt be required?

byu/WyoGuy2 inAskConservatives

The Minnesota Office of Traffic Safety also states that there is no law against children being in the front seat, although the rear seat is generally considered the safest place for them to sit. The Minnesota Office of Traffic Safety also warns that all passengers, regardless of age, must be legally restrained while in a motor vehicle. Any passenger over 15 who is unbelted will be ticketed directly.

Riding in the cargo area of a pickup truck is legal in the Land of 10,000 Lakes, according to AAA.

The Keep Right and Move Over Laws in Minnesota

While almost everyone knows that they are supposed to buckle up when riding in a moving vehicle, many people don’t realize that it is illegal to camp out in the left lane in Minnesota if you are traveling slower than the rest of the traffic.

This law is designed to reduce the number of accidents by limiting the number of lane changes made by faster-moving drivers. Browse our guide to learn the specific laws and rules by state.

The North Star State also has a “Move Over” Law aimed at keeping law enforcement and emergency service personnel safe when they are operating on the side of the road.

Specifically, the law states that if the road has more than two lanes, you must keep at least one full lane clear from stopped emergency vehicles with their lights engaged. If you can’t move over, you must reduce your speed. You can be fined more than $100 if you fail to do so.

Speed Limit in Minnesota

The North Star State recognizes speed as one of its major issues when it comes to highway safety. See more in our guide to learn the specific laws and rules by state.

The Minnesota Department of Public Safety even released a fact sheet on the topic, which states that between 2013 and 2017:

Fatalities resultung from speed-related crashes costs Minnesota over $639 million.

Speed increases the chances that you will lose control of your vehicle or fail to stop in time if the driver in front of you suddenly brakes. Because Minnesota recognizes the dangers of excess speed, the Minnesota Department of Transportation has set out some of the following speed limits:

- 10 MPH in alleys

- 30 MPH on urban streets

- 55 MPH on most other roadways

- 65 MPH on expressways and urban interstates

- 70 MPH on rural interstates

School zones in Minnesota have a speed limit of no less than 15 MPH but no more than 30.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Ridesharing Overview

One of the most popular ways to get around these days is through Ridesharing. Companies such as Uber and Lyft just pick you up and handle all of the traffic headaches for you.

Ridesharing does not come without insurance and other regulations, though. Investopedia points out that drivers of Rideshare vehicles used to be forced to get commercial insurance.

Lyft and Uber pulling out of the Twin Cities could be a good thing… Hear me out.

byu/TheGreatMars inTwinCities

That is now a thing of the past. Many major car insurance companies are now offering Rideshare policies or allowing policyholders to add them to their traditional ones.

Be aware, though, that if you get caught driving for a rideshare company and you haven’t notified your car insurance carrier of your intentions to use your private passenger vehicle for that purpose, your coverage could be dropped.

Road Automation

Like ridesharing, Automated Vehicles are all the rage these days. The idea that the future is now is fascinating, but self-driving cars come with risks. These risks have caused the Governor of Minnesota to issue an Executive Order on the matter.

In this executive order, the governor established an advisory board to develop recommendations for changes to the state’s laws, rules, and policies related to autonomous technology. It seems there’s still more to come in this area, so stay tuned.

Safety Laws