Best Car Insurance in Missouri for 2026 [MO’s Top 10 Companies]

Finding the best car insurance in Missouri is easy with Liberty Mutual, Farmers, and Travelers. For as low as $18 a month, these MO insurers offer top claims assistance, up to 30% UBI discounts, and strong financial stability, making them a reliable choice for meeting Missouri car insurance requirements.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Insurance Feature Writer

Rachel Bodine graduated from college with a BA in English. She has since worked as a Feature Writer in the insurance industry and gained a deep knowledge of state and countrywide insurance laws and rates. Her research and writing focus on helping readers understand their insurance coverage and how to find savings. Her expert advice on insurance has been featured on sites like PhotoEnforced, All...

Rachel Bodine

Licensed Insurance Agent

Eric Stauffer is an insurance agent and banker-turned-consumer advocate. His priority is educating individuals and families about the different types of insurance coverage. He is passionate about helping consumers find the best coverage for their budgets and personal needs. Eric is the CEO of C Street Media, a full-service marketing firm and the co-founder of ProperCents.com, a financial educat...

Eric Stauffer

Updated May 2025

3,072 reviews

3,072 reviewsCompany Facts

Full Coverage in Missouri

A.M. Best Rating

Complaint Level

Pros & Cons

3,072 reviews 1,734 reviews

1,734 reviewsCompany Facts

Full Coverage in Missouri

A.M. Best Rating

Complaint Level

Pros & Cons

1,734 reviewsLiberty Mutual, Farmers, and Travelers offer the best car insurance in Missouri. These MO insurers provide accident forgiveness, safe-driver rewards, and rates as low as $18 per month.

Missouri drivers face risks like distraction and bad weather, so having the right protection is essential. Below, we break down average car insurance rates by city, highlight key discounts, and show how age and location affect your cost.

Our Top 10 Company Picks: Best Car Insurance in Missouri

| Company | Rank | Monthly Rates | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | $197 | A | Comprehensive Coverage | Liberty Mutual | |

| #2 | $207 | A | Personalized Service | Farmers | |

| #3 | $173 | A++ | Specialized Coverage | Travelers | |

| #4 | $226 | A+ | Strong Network | Allstate |

| #5 | $150 | A+ | Innovative Technology | Progressive |

| #6 | $162 | A | Customer Focus | American Family | |

| #7 | $137 | A++ | Affordable Rates | Geico | |

| #8 | $130 | A++ | National Presence | State Farm | |

| #9 | $101 | A+ | Flexible Policies | Nationwide | |

| #10 | $76 | A++ | Military Focus | USAA |

It also examines minimum legal coverage and optional add-ons and provides tips for selecting a policy that best suits your needs.

- USAA offers the cheapest coverage in Missouri for $18 a month

- Liberty Mutual provides Missouri citizens with dedicated support

- Missouri drivers face risks like distracted driving and weather hazards

Comparing Missouri car insurance quotes is the easiest way to find affordable coverage. Simply enter your ZIP code into our free comparison tool to find rates in your area.

#1 – Liberty Mutual: Top Overall Pick

Pros

- Extensive Protection: Liberty Mutual offers Missouri drivers comprehensive coverage options at $129 for full protection against various road hazards.

- Substantial Discounts: Missouri residents can enjoy up to 35% anti-theft and 25% bundling discounts, according to Liberty Mutual car insurance reviews.

- Claims Assistance: Policyholders throughout Missouri receive dedicated support from Liberty Mutual’s extensive claims network during stressful post-accident situations.

Cons

- Premium Pricing: At $46 for minimum coverage, Liberty Mutual costs more than several competitors for basic protection in Missouri markets.

- Credit Sensitivity: Missouri drivers with poor credit face significantly higher rates at $541 monthly with Liberty Mutual’s credit-based pricing model.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#2 – Farmers: Best for Personalized Service

Pros

- Agent Network: Farmers has a big network of local agents all over Missouri who can help you out with tricky insurance choices and offer personalized advice.

- Customized Packages: Missouri customers can tailor policies with Farmers’ flexible coverage options starting at $48 for minimum legal requirements.

- Claims Satisfaction: The Farmers car insurance review highlights their strong claims handling satisfaction among Missouri policyholders after weather-related incidents.

Cons

- Young Driver Costs: Missouri teens face steep premiums with Farmers, averaging $814 monthly for 17-year-old female drivers seeking full coverage.

- Rate Increases: Missouri policyholders often experience significant premium jumps with Farmers after filing even minor claims or receiving tickets.

#3 – Travelers: Best for Specialized Coverage

Pros

- Unique Protections: Travelers car insurance review shows Missouri drivers benefit from specialized coverage options like premier new car replacement and gap insurance.

- Strong Financial Stability: With an A++ A.M. Best rating, Travelers provides Missouri policyholders exceptional financial security for claim payments.

- Accident Forgiveness: First-time accidents for qualified Missouri drivers won’t raise premiums under Travelers’ forgiveness program at $114 for full coverage.

Cons

- Limited Locations: Missouri rural drivers may struggle to find Travelers agents in smaller communities throughout the state for in-person assistance.

- Technology Limitations: Missouri customers’ digital experience lags behind that of their competitors despite Travelers’ strong traditional insurance offerings.

#4 – Allstate: Best for Strong Network

Pros

- Local Presence: Allstate’s extensive agent network throughout Missouri’s urban and rural areas ensures personalized service regardless of location.

- Claims Guarantee: The Allstate car insurance review confirms Missouri customers receive guaranteed claim service satisfaction or money back.

- Education Resources: Missouri drivers use Allstate’s tools. They learn to drive better and pay less for insurance.

Cons

- Premium Rates: Missouri drivers pay higher premiums with Allstate at $52 for minimum coverage compared to most competing insurance providers.

- Loyalty Pricing: Long-term Missouri customers sometimes face higher rate increases than new policyholders despite maintaining clean driving records.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#5 – Progressive: Best for Innovative Technology

Pros

- Rate Comparison Tool: Missouri shoppers can compare multiple companies’ rates directly through Progressive’s transparent pricing tool before purchasing coverage.

- Snapshot Program: The Progressive car insurance review highlights how Missouri drivers saved an average of $231 annually through their usage-based insurance program.

- Mobile Technology: Progressive offers Missouri customers superior digital tools for policy management and claims reporting regardless of their location.

Cons

- Coverage Gaps: Some specialized protection options wanted by Missouri drivers aren’t available through Progressive’s standard policy offerings.

- Customer Service Inconsistency: Missouri policyholders report varying experiences with Progressive’s customer support depending on their specific claim situation.

#6 – American Family: Best for Customer Focus

Pros

- Family-Oriented Policies: American Family car insurance review shows Missouri households receive special multi-vehicle and young driver discounts unavailable elsewhere.

- Claims Satisfaction: Missouri customers consistently rate American Family highly for their smooth claims process following accidents and weather damage.

- Teen Driver Support: Parents across Missouri appreciate American Family’s Teen Safe Driver program while paying moderate rates of $106 for full coverage.

Cons

- Digital Limitations: Missouri customers seeking fully digital insurance experiences find American Family’s technology offerings somewhat limited compared to competitors.

- Coverage Restrictions: Some specialty vehicles common in rural Missouri areas have limited coverage options under American Family’s standard policies.

#7 – Geico: Best for Affordable Rates

Pros

- Competitive Pricing: Missouri drivers enjoy some of the most affordable rates with Geico at just $32 for minimum and $90 for full coverage policies.

- Military Discounts: The Geico car insurance review notes that active military personnel throughout Missouri receive special rate reductions not widely available elsewhere.

- Online Efficiency: Geico provides Missouri customers with superior digital tools for quick quotes, policy changes, and claims without agent intervention.

Cons

- Limited Personalization: Missouri drivers seeking highly customized coverage options may find Geico’s standardized policies somewhat restrictive for unique situations.

- Agent Availability: Residents in rural Missouri areas have limited access to in-person Geico agents when complex insurance questions arise.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#8 – State Farm: Best for National Presence

Pros

- Local Agents: State Farm car insurance review confirms Missouri customers benefit from the largest network of local agents providing personalized service throughout the state.

- Banking Integration: Missouri policyholders can combine insurance and banking services with State Farm for simplified financial management and potential discounts.

- Accident Forgiveness: Qualified Missouri drivers keep rates after their first accident with State Farm’s accident forgiveness.

Cons

- Technology Gaps: Missouri customers seeking cutting-edge digital insurance tools may find State Farm’s technology offerings somewhat traditional compared to competitors.

- Rate Transparency: Missouri shoppers sometimes struggle to understand State Farm’s complex pricing structure despite competitive $85 full coverage rates.

#9 – Nationwide: Best for Flexible Policies

Pros

- Affordability Leader: Missouri drivers have access to the second-lowest rates nationwide, at just $23 for minimum coverage and $66 for full coverage options.

- Vanishing Deductible: The Nationwide car insurance review highlights how Missouri policyholders can reduce deductibles by $100 annually for safe driving.

- On Your Side Review: Missouri customers receive free annual policy reviews, which ensure optimal coverage and available discounts as their situations change.

Cons

- Higher Complaint Ratio: Missouri policyholders file more complaints about Nationwide, with a 0.78 ratio compared to other major insurers in the state.

- Coverage Limitations: Some specialty vehicles common in rural Missouri areas have restricted coverage options under standard Nationwide policies.

#10 – USAA: Best for Military Focus

Pros

- Unmatched Rates: Eligible Missouri military families can access the lowest premiums, at just $18 for minimum coverage and $50 for full coverage protection.

- Superior Service: USAA car insurance review confirms Missouri members consistently report the highest satisfaction ratings among all insurance providers.

- Military Understanding: In Missouri, service members find help in USAA’s coverage, which is built for their needs when they go to war or move.

Cons

- Eligibility Restrictions: Most Missouri residents cannot access USAA’s exceptional rates without military service connections or family member eligibility.

- Limited Locations: Missouri USAA members have no physical branch locations for in-person assistance when complex insurance questions arise.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Missouri Car Insurance Rates From Top Insurers

Buying car insurance means understanding Missouri’s auto insurance requirements and knowing which car insurance companies offer the best value. Below are the items included in the car insurance minimum coverage:

- Bodily Injury Liability: $25,000 per person, $50,000 per accident

- Property Damage Liability: $10,000 per accident

- Uninsured Motorist: $25,000 per person, $50,000 per accident

The table below outlines cheap car insurance in Missouri, showing monthly rates by provider and coverage level so you can easily compare your options.

Missouri Car Insurance Monthly Rates by Provider & Coverage Level

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

|

| $80 | $226 |

| $57 | $162 | |

| $73 | $207 | |

| $48 | $137 | |

| $70 | $197 | |

| $36 | $101 | |

| $53 | $150 | |

| $46 | $130 | |

| $61 | $173 | |

| $27 | $76 |

Selecting the right insurer protects both your family and your finances after an accident. It also ensures help with claims processing and legal guidance in the Show-Me State.

We’re here to guide you through buying car insurance in Missouri, from legal requirements to choosing a provider that fits your needs.

Use the data above to set your budget and identify cheap car insurance in Missouri, especially if you’re aiming for cheap full coverage car insurance in Missouri. Liberty Mutual, for example, stands out in terms of competitive rates and broad coverage options.

Reliable Missouri car insurance companies offer financial strength, responsive claims support, and affordability.Brad Larson LICENSED INSURANCE AGENT

A.M. Best rates Liberty Mutual highly for its financial stability. Missouri drivers on Reddit also recommend it as a trusted insurer.

Missouri Auto Insurance Cost Factors

If you’re wondering, “How much is car insurance in Missouri?” Your car, age, gender, and location all impact your auto insurance premiums. To find the best coverage in Missouri, compare providers and plans.

A Consumer Federation of America study found that in 10 cities, 40- and 60-year-old women with perfect driving records often paid more than men for basic coverage. Gender and age can affect your premiums. Check the table below to see how these factors influence rates in Missouri.

Full Coverage Auto Insurance Monthly Rates in Missouri by Provider, Age, & Gender

| Company | Age: 17 Female | Age: 17 Male | Age: 25 Female | Age: 25 Male | Age: 35 Female | Age: 35 Male | Age: 60 Female | Age: 60 Male |

|---|---|---|---|---|---|---|---|---|

|

| $430 | $460 | $240 | $252 | $231 | $228 | $226 | $223 |

| $659 | $714 | $226 | $234 | $237 | $229 | $213 | $220 | |

| $814 | $842 | $225 | $236 | $198 | $197 | $176 | $187 | |

| $493 | $522 | $145 | $146 | $158 | $177 | $123 | $157 | |

| $1,031 | $1,121 | $267 | $306 | $244 | $248 | $211 | $227 | |

| $586 | $679 | $177 | $194 | $161 | $164 | $141 | $149 | |

| $572 | $643 | $214 | $219 | $176 | $163 | $144 | $148 | |

| $407 | $513 | $159 | $181 | $141 | $141 | $126 | $126 | |

| $454 | $525 | $150 | $160 | $140 | $145 | $130 | $135 | |

| $383 | $468 | $161 | $179 | $129 | $128 | $116 | $118 |

Location also plays a role—your neighborhood or city may affect your insurance costs. Keep reading to learn more. Living on the best street in the city has its advantages. Your neighbors are friendly, and nearby amenities are conveniently located.

Convenience comes at a cost. Check the tables below to see how much your neighbors pay for car insurance. Use this data to find the cheapest ZIP codes and identify where the most affordable coverage options are available in Missouri.

Missouri Cheapest Monthly Rates by Zip Codes

| ZIP Code | City | Monthly Rate | Most Expensive Company | Most Expensive Monthly Rate | 2nd Most Expensive Company | 2nd Most Expensive Monthly Rate | Cheapest Company | Cheapest Monthly Rate | 2nd Cheapest Company | 2nd Cheapest Monthly Rate |

|---|---|---|---|---|---|---|---|---|---|---|

| 65301 | Sedalia | $245 | $345 |

| $322 | $166 | $198 | |||

| 65536 | Lebanon | $245 | $347 |

| $319 | $165 | $187 | |||

| 65340 | Marshall | $247 | $342 | $330 | $168 | $176 | ||||

| 65347 | Nelson | $251 | $340 | $330 | $168 | $175 | ||||

| 65023 | Centertown | $251 | $348 | $323 | $173 | $190 | ||||

| 65473 | Fort Leonard Wood | $251 | $357 |

| $351 | $165 | $195 | |||

| 65109 | Jefferson City | $252 | $350 |

| $308 | $173 | $194 | |||

| 65339 | Malta Bend | $252 | $348 |

| $339 | $168 | $176 | |||

| 63461 | Palmyra | $252 | $341 | $330 | $163 | $206 | ||||

| 65344 | Miami | $252 | $354 | $330 | $168 | $175 | ||||

| 65337 | La Monte | $253 | $346 | $330 | $166 | $192 | ||||

| 65101 | Jefferson City | $253 | $353 | $323 | $173 | $195 | ||||

| 64735 | Clinton | $253 | $343 | $333 | $170 | $190 | ||||

| 65350 | Smithton | $253 | $345 | $330 | $166 | $198 | ||||

| 65053 | Lohman | $253 | $348 |

| $325 | $173 | $191 | |||

| 64658 | Marceline | $254 | $360 | $330 | $165 | $194 | ||||

| 63352 | Laddonia | $254 | $358 | $330 | $174 | $185 | ||||

| 63501 | Kirksville | $254 | $362 | $330 | $166 | $206 | ||||

| 64001 | Alma | $254 | $349 |

| $341 | $173 | $191 | |||

| 65330 | Gilliam | $255 | $351 | $330 | $168 | $176 | ||||

| 65321 | Blackburn | $255 |

| $360 | $349 | $168 | $176 | |||

| 65349 | Slater | $255 | $351 | $330 | $168 | $176 | ||||

| 65323 | Calhoun | $255 | $343 |

| $331 | $170 | $176 | |||

| 65320 | Arrow Rock | $255 | $353 | $330 | $168 | $175 | ||||

| 65401 | Rolla | $255 | $363 |

| $341 | $174 | $185 |

The data shows that residents near Russell Park pay almost $300 less than those near Tandy Recreation Center. Rates can vary widely depending on ZIP code due to factors like local traffic conditions, accident frequency, and theft rates.

Missouri Most Expensive Monthly Rates by ZIP Codes

| ZIP Code | City | Monthly Rate | Most Expensive Company | Most Expensive Monthly Rate | 2nd Most Expensive Company | 2nd Most Expensive Monthly Rate | Cheapest Company | Cheapest Monthly Rate | 2nd Cheapest Company | 2nd Cheapest Monthly Rate |

|---|---|---|---|---|---|---|---|---|---|---|

| 63120 | SAINT LOUIS | 435 |

| 646 | 546 | 227 | 303 | |||

| 63113 | SAINT LOUIS | 435 |

| 689 |

| 543 | 227 | 303 | ||

| 63115 | SAINT LOUIS | 431 |

| 656 |

| 547 | 227 | 303 | ||

| 63107 | SAINT LOUIS | 430 |

| 669 | 543 | 227 | 303 | |||

| 63147 | SAINT LOUIS | 428 |

| 632 |

| 560 | 227 | 303 | ||

| 63106 | SAINT LOUIS | 423 |

| 589 |

| 581 | 227 | 303 | ||

| 63118 | SAINT LOUIS | 412 | 543 |

| 540 | 227 | 279 | |||

| 63137 | SAINT LOUIS | 411 |

| 627 |

| 494 | 227 | 279 | ||

| 63136 | SAINT LOUIS | 409 |

| 561 |

| 532 | 227 | 276 | ||

| 63112 | SAINT LOUIS | 405 | 543 |

| 524 | 227 | 303 | |||

| 63111 | SAINT LOUIS | 400 | 543 |

| 538 | 227 | 287 | |||

| 63116 | SAINT LOUIS | 398 | 543 |

| 516 | 227 | 283 | |||

| 63101 | SAINT LOUIS | 397 | 543 |

| 507 | 227 | 279 | |||

| 63102 | SAINT LOUIS | 396 | 543 |

| 500 | 227 | 279 | |||

| 63138 | SAINT LOUIS | 395 |

| 573 |

| 494 | 227 | 274 | ||

| 63103 | SAINT LOUIS | 393 | 543 |

| 508 | 227 | 279 | |||

| 63108 | SAINT LOUIS | 391 | 543 |

| 518 | 227 | 276 | |||

| 63155 | SAINT LOUIS | 390 | 543 |

| 465 | 227 | 279 | |||

| 63104 | SAINT LOUIS | 383 | 543 |

| 478 | 227 | 279 | |||

| 63110 | SAINT LOUIS | 381 | 543 |

| 492 | 227 | 271 | |||

| 64124 | KANSAS CITY | 377 | 554 |

| 459 | 211 | 293 | |||

| 64127 | KANSAS CITY | 376 | 554 |

| 450 | 211 | 293 | |||

| 64123 | KANSAS CITY | 375 |

| 510 | 497 | 211 | 293 | |||

| 64128 | KANSAS CITY | 375 | 554 |

| 465 | 211 | 293 | |||

| 63121 | SAINT LOUIS | 375 | 490 |

| 482 | 227 | 267 |

When searching for the best car insurance in St. Louis, these local details can have a significant impact on your monthly premium. The Show-Me State has some of the most beautiful historic neighborhoods in the U.S., but that charm may come at a cost when finding the best car insurance in Missouri.

Larger cities like St. Louis often pay higher premiums due to more cars and accidents. See the tables below to compare car insurance rates in your city.

Missouri Cheapest Monthly Rates by Cities

| Cheapest Cities in Missouri | Monthly Rate | Most Expensive Company | Most Expensive Monthly Rate | 2nd Most Expensive Company | 2nd Most Expensive Monthly Rate | Cheapest Company | Cheapest Monthly Rate | 2nd Cheapest Company | 2nd Cheapest Monthly Rate |

|---|---|---|---|---|---|---|---|---|---|

| Sedalia | $245 | $345 |

| $322 | $166 | $198 | |||

| Lebanon | $245 | $346 |

| $319 | $165 | $187 | |||

| Marshall | $247 | $342 | $330 | $168 | $176 | ||||

| Nelson | $251 | $340 | $330 | $168 | $175 | ||||

| Centertown | $251 | $348 | $323 | $173 | $190 | ||||

| Fort Leonard Wood | $251 | $357 |

| $351 | $165 | $195 | |||

| Malta Bend | $252 | $348 |

| $339 | $168 | $176 | |||

| Palmyra | $252 | $341 | $330 | $163 | $206 | ||||

| Jefferson City | $252 | $352 | $308 | $173 | $194 | ||||

| Miami | $252 | $354 | $330 | $168 | $175 | ||||

| La Monte | $253 | $345 | $330 | $166 | $191 | ||||

| Clinton | $253 | $343 | $333 | $170 | $189 | ||||

| Smithton | $253 | $345 | $330 | $166 | $198 | ||||

| Lohman | $253 | $348 |

| $325 | $173 | $191 | |||

| Marceline | $254 | $360 | $330 | $165 | $194 | ||||

| Laddonia | $254 | $358 | $330 | $174 | $185 | ||||

| Kirksville | $254 | $362 | $330 | $166 | $205 | ||||

| Alma | $254 | $349 |

| $342 | $173 | $191 | |||

| Gilliam | $254 | $351 | $330 | $168 | $176 | ||||

| Blackburn | $254 |

| $360 | $349 | $168 | $176 | |||

| Slater | $255 | $351 | $330 | $168 | $176 | ||||

| Calhoun | $255 | $343 |

| $331 | $170 | $176 | |||

| Arrow Rock | $255 | $353 | $330 | $168 | $175 | ||||

| Rolla | $255 | $363 |

| $341 | $175 | $185 | |||

| Vandalia | $255 | $362 |

| $334 | $174 | $184 |

Sedalia offers the most affordable rates, allowing residents to save on car insurance. St. Louis residents pay an average of $4,361, nearly $1,300 more than Sedalia residents, who pay $2,938 for the same coverage. With St. Louis’s population of nearly 320,000 and Sedalia’s 22,000, the increased population means more cars and a higher accident risk.

Missouri Most Expensive Monthly Rates by Cities

| Most Expensive Cities in Missouri | Monthly Rate | Most Expensive Company | Most Expensive Monthly Rate | 2nd Most Expensive Company | 2nd Most Expensive Monthly Rate | Cheapest Company | Cheapest Monthly Rate | 2nd Cheapest Company | 2nd Cheapest Monthly Rate |

|---|---|---|---|---|---|---|---|---|---|

| Pine Lawn | 435 |

| 646 | 546 | 227 | 303 | |||

| Bellefontaine Neighbors | 411 |

| 627 |

| 494 | 227 | 280 | ||

| Castle Point | 409 |

| 561 |

| 532 | 227 | 276 | ||

| St. Louis | 399 | 539 |

| 512 | 227 | 282 | |||

| Spanish Lake | 395 |

| 573 |

| 494 | 227 | 274 | ||

| Bel-Nor | 374 | 490 |

| 482 | 227 | 267 | |||

| Hanley Hills | 365 | 514 |

| 487 | 227 | 267 | |||

| Calverton Park | 360 |

| 469 | 463 | 227 | 248 | |||

| Black Jack | 360 |

| 470 | 465 | 205 | 257 | |||

| Old Jamestown | 356 |

| 478 | 463 | 205 | 261 | |||

| Berkeley | 351 | 470 | 462 | 227 | 251 | ||||

| Clayton | 350 | 543 | 463 | 227 | 240 | ||||

| Florissant | 346 |

| 463 | 463 | 205 | 241 | |||

| Hazelwood | 342 | 462 |

| 459 | 205 | 225 | |||

| University City | 331 | 476 |

| 410 | 227 | 239 | |||

| Bella Villa | 326 |

| 434 | 431 | 227 | 237 | |||

| Richmond Heights | 325 | 452 | 439 | 227 | 234 | ||||

| Breckenridge Hills | 324 | 483 |

| 420 | 205 | 238 | |||

| Maplewood | 323 | 469 |

| 414 | 227 | 234 | |||

| Mehlville | 323 |

| 445 | 436 | 221 | 227 | |||

| Olivette | 322 | 441 |

| 414 | 227 | 237 | |||

| Bel-Ridge | 319 | 446 |

| 409 | 227 | 238 | |||

| Cedar Hill | 319 | 438 |

| 414 | 227 | 232 | |||

| Kansas City | 317 | 444 |

| 401 | 210 | 226 | |||

| Luebbering | 316 | 420 |

| 404 | 205 | 220 |

Accidents lead to claims, which in turn raise rates for everyone. This makes selecting the best car insurance in Missouri even more important. We can help you make the right choice. Adjusting your driving habits can lower your car insurance rates, but that’s not always possible. Therefore, shopping around is essential.

The table below shows the cost of each mile, helping you make informed decisions and potentially save money by choosing the best car insurance in Missouri.

Missouri Commute Monthly Rates by Provider

| Company | 10 Miles Commute | 25 Miles Commute |

|---|---|---|

|

| $341 | $341 |

| $271 | $277 | |

| $359 | $359 | |

| $236 | $245 | |

| $377 | $377 | |

| $189 | $189 | |

| $285 | $285 | |

| $219 | $230 | |

| $251 | $261 | |

| $203 | $218 |

USAA offers the lowest rate regardless of mileage, but other factors also matter. If you have a long commute, consider reviewing the complaint and loss ratios of different companies, as increased time on the road increases the risk of accidents. Paying a bit more for a company with fewer claim rejections might be worth it. Additionally, consider the amount of coverage you require.

Read More: Different Types of Car Insurance Coverage

The age of your car and the distance you travel aren’t the only factors affecting your rates. Consumer Reports revealed that car insurance companies in some states may charge more based on your credit score.

Missouri Auto Insurance Monthly Rates by Credit Score

| Company | Good Credit | Fair Credit | Poor Credit |

|---|---|---|---|

|

| $250 | $303 | $471 |

| $212 | $252 | $358 | |

| $325 | $342 | $411 | |

| $173 | $216 | $332 | |

| $260 | $329 | $541 | |

| $160 | $184 | $223 | |

|

| $251 | $273 | $330 |

| $165 | $201 | $307 | |

| $117 | $163 | $351 |

A higher credit score can save you money on car insurance because insurers assume you’re less likely to file a claim after an accident.

Improving your credit score can help you save money on car insurance, but maintaining a clean driving record is the most effective way to do so. Note that different providers handle claims differently, which can impact your experience and the resolution.

Missouri uses a points system to track driving records. A speeding ticket can add points to your license for 18 months, potentially leading to suspension. Other violations may stay on your record for up to 3 years and can significantly raise your car insurance rates. See the table below for details.

Missouri Auto Insurance Monthly Rates by Driving Record

| Company | Clean Record | One Ticket | One Accident | One DUI |

|---|---|---|---|---|

|

| $293 | 331 | $330 | $411 |

| $205 | 234 | $296 | $360 | |

| $311 | 362 | $387 | $378 | |

| $188 | 204 | $243 | $328 | |

| $273 | 435 | $393 | $405 | |

| $149 | 162 | $190 | $254 | |

|

| $247 | 289 | $330 | $274 |

| $206 | 224 | $242 | $224 | |

| $169 | 185 | $205 | $283 |

Driving defensively in the Show-Me State can save you money. So, we can designate a driver and lighten up that lead foot.

High-Risk Insurance

High-risk drivers in Missouri may face higher car insurance rates or struggle to find coverage.

If this happens, the Missouri Automobile Insurance Plan can help. To qualify, you must prove you’ve been denied coverage within the last 60 days and have a valid driver’s license. For more information, contact the Missouri Department of Insurance:

- Call 800-726-7390

- Email [email protected]

Sometimes, financial struggles can also make finding car insurance challenging.

Read More: Things You Do That Can Raise Your Premiums

Car Insurance Coverage Options in Missouri

To get the most value from your car insurance in Missouri, it’s essential to understand how your coverage is priced. Knowing how car insurance works helps ensure you’re not overpaying while staying properly protected.

Missouri Car Insurance Monthly Rates by Coverage Type

| Type | Cost |

|---|---|

| Collision | $23 |

| Combined Total | $73 |

| Comprehensive | $15 |

| Liability | $35 |

Saving on essential coverage may also allow you to add extra coverage to your policy without stretching your budget. Missouri requires minimum coverage for bodily injury, property damage, and uninsured drivers. Additional options can offer better protection:

- Personal Injury Protection (PIP): Covers medical costs, regardless of fault.

- Medical Payments (MedPay): This covers medical bills for all passengers, including ambulance and treatment expenses.

- Uninsured/Underinsured Motorist: Included in Missouri’s minimums—covers costs if the other driver lacks sufficient insurance.

Consider a provider’s loss ratio to assess financial health and reliability. A high loss ratio (75 %+) may signal rising rates; a low ratio (below 35%) may indicate overpriced policies.

Missouri Car Insurance Loss Ratios for MedPay and UM/UIM Coverage

| Coverage Type | 2022 | 2023 | 2024 |

|---|---|---|---|

| Medical Payments (MedPay) | 76% | 78.6% | 79% |

| Uninsured/Underinsured Motorist | 82% | 84.6% | 85% |

Missouri’s current loss ratios suggest a stable market. With 14% of drivers uninsured, adding extra coverage can provide better protection for you and your family.

Add-Ons and Endorsements

Owning a car offers freedom and independence, but it also reflects your personality. Some express this by choosing a specific make, modifying their car, or restoring a classic.

To protect your investment, it’s essential to ensure your car has the right coverage, regardless of the make and model you drive. Add-ons and endorsements from the best car insurance in Missouri can help.

Popular add-ons include:

- Rental Reimbursement: Pays for a rental car while your vehicle is being repaired after a covered claim.

- Emergency Roadside Assistance: Helps cover towing, flat tires, lockouts, and other roadside issues.

- Gap Insurance: Pays the difference between your car’s value and what you owe if it’s totaled or stolen.

- Non-Owner Car Insurance: Offers liability coverage for drivers without a personal vehicle.

- Mechanical Breakdown Insurance: This covers major car repairs that are not related to accidents.

Before modifying your vehicle, check Missouri state laws on lift kits and window tinting.

Missouri restricts the height to which a car can be lowered and the type of window tinting permitted.

Windshield Coverage

Even safe drivers can encounter unexpected issues, such as windshield damage. The right insurance helps with claims, but Missouri requires windshields to be clear and free of cracks over 3 inches. Deviating from insurer-recommended repair shops could cost you extra. Violations may lead to fines or failure to pass the State Safety Inspection.

Read More: Should I use insurance to replace my windshield?

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Missouri Auto Insurance Discounts

Missouri policyholders seeking low-income car insurance in Missouri often ask insurers about available discounts to reduce their premiums. These companies below offer savings for bundling, safe driving, and more, helping drivers lower their car insurance costs easily.

Missouri Car Insurance Discounts From the Top Providers

| Company | Anti-Theft | Bundling | New Car | Safe Driver | UBI |

|---|---|---|---|---|---|

|

| 10% | 25% | 10% | 18% | 30% |

| 25% | 25% | 15% | 18% | 30% | |

| 10% | 20% | 12% | 20% | 30% | |

| 25% | 25% | 10% | 15% | 25% | |

| 35% | 25% | 8% | 20% | 30% | |

| 5% | 20% | 15% | 12% | 40% | |

| 25% | 10% | 10% | 10% | $231/yr | |

| 15% | 17% | 15% | 20% | 30% | |

| 15% | 13% | 8% | 17% | 30% | |

| 15% | 10% | 10% | 10% | 30% |

Explore your options with confidence; only car insurance companies in Missouri can offer the right mix of coverage and discounts tailored to your needs.

Largest Companies’ Financial Ratings

A.M. Best is the only credit agency in the world with a singular focus on the insurance industry. For this reason, it has become a trusted agency that other agencies, such as the National Association of Insurance Commissioners (NAIC), rely on.

This means that you can rely on them to help you determine which providers offer the best car insurance in Missouri and which is the most trusted car insurance company in your area.

By looking at how they’ve scored the companies you’re considering, you can gain insight into the overall health of the car insurance market in Missouri.

Insurance Companies by A.M. Best Rating and Outlook

| Best Rated Companies | A.M. Best Rating | Outlook |

|---|---|---|

|

| A+ | Stable |

| A | Stable | |

| A | Stable | |

| A++ | Stable | |

| A | Stable | |

| A+ | Stable | |

| A+ | Stable | |

| A++ | Stable | |

| A++ | Stable | |

| A++ | Stable |

When you choose a company with a high rating from A.M. Best, you are choosing one that has a good loss ratio and whose financial outlook is stable. Lowering auto insurance premium costs is possible by taking advantage of available discounts, keeping a spotless driving record, and choosing coverage that aligns with your individual needs.

Companies With Best Ratings

A.M. Best is not the only company that is looking out for you. J.D. Power has also been monitoring the car insurance market, and what it has discovered is that consumer satisfaction with car insurance providers is at an all-time high.

J.D. Power Car Insurance Study

| Insurance Company | J.D. Power Score | Power Circle Rating |

|---|---|---|

| 855 | 🟡🟡🟡🟡🟡 | |

| 847 | 🟡🟡🟡🟡 |

| 838 | 🟡🟡🟡🟡 | |

| 833 | 🟡🟡🟡🟡 | |

| Central Region | 826 | 🟡🟡🟡 |

| 824 | 🟡🟡🟡 | |

| 823 | 🟡🟡🟡 | |

|

| 822 | 🟡🟡🟡 |

| 821 | 🟡🟡🟡 | |

| 815 | 🟡🟡 | |

| 814 | 🟡🟡 | |

| 806 | 🟡🟡 | |

| 806 | 🟡🟡 | |

| 803 | 🟡🟡 | |

| 803 | 🟡🟡 | |

| 906 | 🟡🟡🟡🟡🟡 |

As satisfied as car insurance consumers seem to be, everyone knows that filing a car insurance claim after an accident isn’t always as delightful as a warm roll from Bread Co. To make sure you’re ready and protected in the event of an emergency, we are here to assist you in locating the best auto insurance in Missouri.

Companies With the Most Complaints

Knowing which insurers receive the most complaints can help you make an informed choice. The complaint ratio compares a company’s complaint volume to its size, with 1.0 being the average.

Car Insurance Market Performance by Company

| Company | Direct Premiums Written | Complaint Ratio | Loss Ratio | Market Share |

|---|---|---|---|---|

|

| $163,137 | 0.03 | 60.06% | 4.19% |

| $506,153 | 0.01 | 66.85% | 12.99% | |

| $219,419 | 0.01 | 66.63% | 5.63% | |

| $253,457 | 0.01 | 75.07% | 6.5% | |

| $256,156 | 0.02 | 64.67% | 6.57% | |

| $170,000 | 0.78 | 65% | 4.5% | |

| $370,336 | 0.09 | 58.99% | 9.5% | |

| $937,742 | 0.09 | 65.35% | 24.06% | |

| $150,000 | 0.41 | 93.20% | 3.8% | |

| $154,615 | 0 | 87.73% | 3.97% |

Higher ratios mean more complaints, but context matters. Larger companies often receive more simply due to more customers.

Read More: Best Car Insurance Companies

Missouri Car Insurance Insights

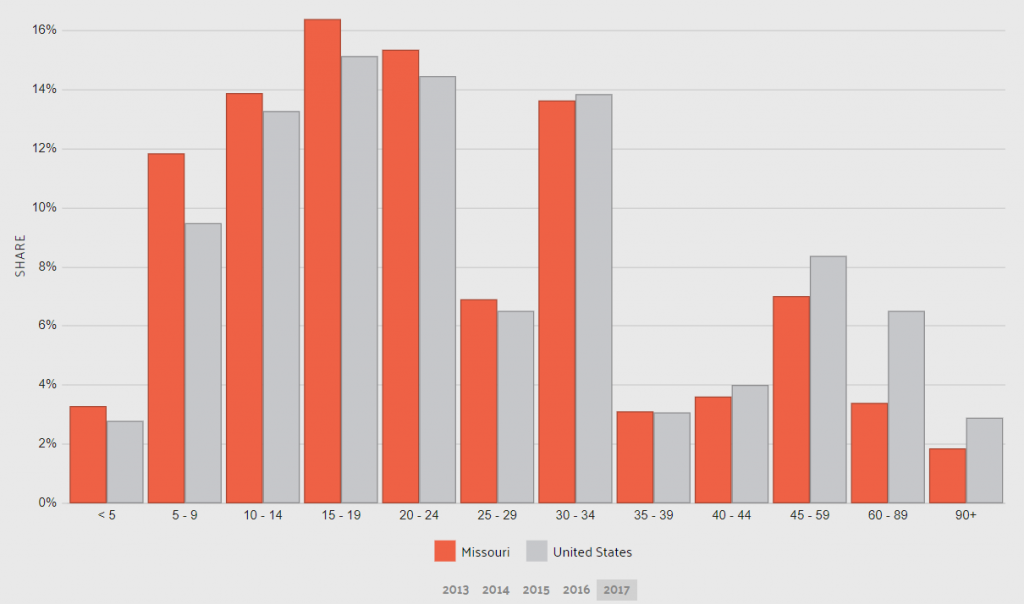

Missouri’s auto insurance landscape shows distinct patterns compared to national trends. Young drivers, those between 15 and 24, make up almost 40% of the claims. The 15 to 19-year-old age group has the most claims, at 15%. It shows that teen drivers in Missouri are taking bigger risks.

So, in Missouri, about 40% of households have two cars, and roughly 22% have three. Overall, around 62% own two or more vehicles, which probably affects how they shop for insurance.

Missouri’s auto insurance report card presents a mixed picture. While the state earns favorable B+ grades for traffic density, it faces challenges with weather-related risks (B) and vehicle theft (C+).

Missouri Report Card: Auto Insurance Premiums

| Category | Grade | Explanation |

|---|---|---|

| Traffic Density | B+ | Urban areas like St. Louis and Kansas City experience heavier traffic. |

| Average Claim Size | B | Claims are moderately priced, often reflecting lower repair/labor costs. |

| Weather-Related Risk | B | Moderate risk due to occasional hail, ice storms, and flooding. |

| Uninsured Drivers Rate | B- | Missouri has a slightly higher than average rate of uninsured drivers. |

| Vehicle Theft Rate | C+ | Some urban centers have higher than average vehicle theft incidents. |

For Missouri residents seeking optimal protection, these combined statistics emphasize the importance of comparing policies that offer strong coverage for young drivers, multi-vehicle discounts, and adequate protection against the state’s specific risk factors.

Read More: 7 Benefits of Teaching Your Teen to Drive

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Missouri State Laws

You need car insurance to drive legally in Missouri, where laws govern coverage requirements, driver licensing, and vehicle registration. With 943 licensed insurers—43 domestic and 900 foreign—you have plenty of options, all required to follow state laws. Understanding these rules helps you choose the best policy and avoid legal issues.

Read More: Does your car insurance and registration need to be under the same name?

MO Car Insurance Costs & Proof of Financial Responsibility

In Missouri, drivers must show proof of financial responsibility when registering a vehicle or if requested by law enforcement.

Acceptable forms include a liability insurance policy meeting the state minimums, a surety or real estate bond, a cash or securities deposit with the Department of Revenue, or a certificate of self-insurance for businesses. Nonresidents must meet the insurance requirements of their home state.

On average, Missouri drivers spend about 2.3% of their disposable income—around $872 annually—on car insurance. This is slightly lower than the national average of $935.80 and less than neighboring Kentucky. To save money, it’s smart to compare rates. You may also be able to deduct car insurance from your taxes if you use your vehicle for business purposes.

Penalties for Driving Without Insurance

In Missouri, you are required to have car insurance to register a vehicle or obtain a driver’s license, and coverage must be continuous.

Driving without insurance can result in:

- 4 license points

- Up to a $300 fine

- Up to 15 days in jail

- Possible license suspension

Points stay on your license indefinitely. Insurance follows the vehicle, so if you drive an uninsured car—even if you’re insured—you’ll still get penalized. Stay protected and choose the right provider to avoid any issues.

Read More: Do you need insurance to buy a car?

Teen, Senior, & New Resident Driving Regulations

Missouri follows a graduated licensing system to help teen drivers gain experience safely. Teens can get an instructional permit at 15, which requires 12 months of incident-free driving, 40 daytime hours, and 10 nighttime hours with a licensed adult. At 16, they can apply for an intermediate license with limited night driving.

Graduated licensing in Missouri ensures teen drivers gain experience safely, building skills step-by-step before earning full driving privileges.Michelle Robbins Licensed Insurance Agent

These restrictions are lifted after six months of safe driving. How your children will impact your car insurance policy often depends on their driving record and experience, so these early steps matter.

Older drivers in Missouri must renew their licenses every three years after age 70 and pass a vision test each time. As aging can affect driving ability, it’s important to monitor changes in vision and response time. If safety becomes a concern, having an open conversation with aging loved ones about their driving habits can help prevent accidents and ensure everyone’s safety on the road.

If you’re new to Missouri, getting set up is simple. To title and tag an out-of-state vehicle, bring all your previous state’s paperwork, including the title. To exchange your driver’s license, just bring your out-of-state license and surrender it when applying for your Missouri license.

Driver’s License Renewal Procedures

Once you obtain your Missouri license, you will need to keep it current. Ages 18–20 renew every 3 years, 21–69 renew every 6 years, and 70+ return to a 3-year cycle.

Renewal can be done in the office or by mail. Military members and their dependents can retain their out-of-state licenses if they claim residency elsewhere. Non-U.S. citizens may have different renewal cycles depending on their immigration status and the documents they hold.

Read More: Can I get car insurance without a license?

Negligent Operator Treatment Systems

To keep your insurance rates low in Missouri, it’s important to maintain a clean driving record by understanding the state’s point system for traffic citations. Points are assigned for offenses like 2 points for DUI, 3 points for speeding, 4 points for reckless driving, and more serious violations, such as driving with a suspended license or felony vehicle crimes, which is 12 points.

If you ask us, there’s no such thing as too many Dougs. pic.twitter.com/s5o0940Bwz

— Liberty Mutual (@LibertyMutual) November 6, 2023

Accumulating 4 to 12 points within 12 months triggers a warning, while additional points can lead to license suspensions ranging from 30 to 90 days. License revocation occurs if you reach 12 or more points in 12 months, 18 or more in 24 months, or 24 or more in 36 months. After reinstatement, 4 points are removed from your record.

Rules of the Road

Now that you are aware of the penalties, it is wise to familiarize yourself with the road rules. Knowing them helps you avoid trouble and keep insurance costs down. Keep scrolling—we’ve got you covered.

Missouri follows a fault-based insurance system, meaning the driver who is found legally responsible for causing an accident is also financially liable for resulting medical expenses and property damage.

This system places greater importance on determining fault after a collision and can lead to legal or financial consequences for the at-fault driver. As a result, having adequate liability coverage is essential to protect yourself from out-of-pocket costs or potential lawsuits.

Read More: No-Fault vs. Tort Car Insurance

Seatbelt and Car Seat Laws

In Missouri, seatbelt use is mandatory for all front-seat passengers aged 16 and older. For younger passengers, child safety laws require that children under age 3 and weighing 40 pounds or less be secured in a proper child restraint.

Children ages 4 to 7 who weigh more than 40 pounds but less than 80 pounds must use a booster seat or approved child restraint system.

Violating these child passenger safety laws can result in a $50 fine. How have cars gotten safer in the past 40 years? Advances in seatbelt design, airbag systems, and child restraint technology have significantly improved passenger safety, especially for children, who remain safest when riding in the back seat.

Keep Right and Move Over Laws

In Missouri, it’s illegal to linger in the left lane on multi-lane roads. Violators face fines. The “Move Over” law requires drivers to switch lanes for emergency vehicles, law enforcement, or workers displaying red, blue, or amber lights. If moving over isn’t possible, reduce speed. Violating this law can lead to fines or imprisonment.

Read More: How to Get a Car Out of Impound

Speed Limits

Missouri speed limits include 65 MPH on rural expressways, 55 MPH on state-lettered highways, 25 MPH in cities and towns where posted, and 20 MPH in most school zones.

Vehicles must maintain at least 40 MPH on interstate highways unless slowed by weather or operating as agricultural equipment. Following posted limits is one of the most important safe driving tips to avoid accidents and penalties.

Ridesharing

Missouri passed HB130 in 2017, allowing rideshare companies like Uber and Lyft to expand. This shift led to changes in insurance coverage for rideshare drivers. Initially, drivers used traditional policies, but now State Farm, USAA, and American Family offer specific rideshare endorsements.

You don’t have to choose these carriers, but they stay current with Missouri’s rideshare laws. Check State Farm’s site to learn more about their rideshare coverage options.

Read More: Cheap Rideshare Auto Insurance

When considering a car insurance provider, inquire about rideshare coverage and associated costs. Missouri also now mandates background checks for rideshare drivers and requires insurance coverage for vehicles in rideshare service. The state is working to protect all drivers on its roads.

Automation on the Road

When shopping for car insurance, ask your agent about rideshare coverage and costs. Missouri now requires background checks and insurance for rideshare drivers, ensuring the safety of all road users.

Proposals for self-driving cars in Missouri failed in 2019, but lawmakers may revisit the issue with new proposals soon.

Safety Laws in Missouri

Missouri enforces a range of safety laws addressing DUI, marijuana-impaired driving, distracted driving, ridesharing, and autonomous vehicles. Understanding and following these laws helps promote road safety and can contribute to lower car insurance rates.

A blood alcohol concentration (BAC) over 0.08 results in DUI charges, with enhanced penalties for BAC levels of 0.15 or higher. Missouri uses a 5-year Look-Back Period, meaning DUI offenses stay on your record for five years.

Penalties include:

- First Offense: Up to 6 months in jail, up to $1,000 fine, 30-day license suspension, 60-day restricted license, possible Ignition Interlock Device (IID).

- Second Offense: Up to 1 year in jail, up to $2,000 fine, 5-year license revocation, 6 months IID.

- Third Offense: Up to 4 years in jail, up to $10,000 fine, 10-year license revocation, 6 months IID.

Missouri has a 5-year Look-Back Period, meaning DUI offenses stay on your record for five years. Driving under the influence of marijuana also carries strict penalties:

- First Offense: Up to 6 months in jail, mandatory substance abuse program, 30-day license suspension.

- Second Offense: Up to 1 year in jail, 30 days of community service, up to $1,000 fine, 2-year license suspension.

- Third Offense: Class D felony, up to 4 years in jail, 60 days community service, up to $5,000 fine, 3-year license revocation.

- Fourth Offense: Class C felony, up to 7 years in jail, up to $5,000 fine, minimum 3-year license revocation.

- Fifth Offense: Class B felony, up to 15 years in jail, 3+ years license revocation.

Aside from DUI, texting while driving is a primary offense for drivers under age 21, and law enforcement can pull them over solely for using a phone. In cities like Chesterfield, Ellisville, and Florissant, bans apply to drivers of all ages. Staying alert behind the wheel is essential for avoiding fines and staying safe.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Driving in Missouri

Driving comes with risks, including weather and theft. Understanding Missouri-specific risks can help lower your car insurance rates. The number one car stolen in the Show-Me State is the 2004 Ford pickup.

Most Stolen Vehicles in Missouri

| Rank | Make/Model | Model Year | Thefts |

|---|---|---|---|

| #1 | Hyundai Elantra | 2017 | 1,200 |

| #2 | Hyundai Sonata | 2015 | 1,150 |

| 3# | Kia Optima | 2016 | 1,100 |

| #4 | Chevrolet Silverado 1500 | 2004 | 950 |

| #5 | Kia Soul | 2015 | 900 |

| #6 | Honda Accord | 1997 | 850 |

| #7 | Honda Civic | 1998 | 800 |

| #8 | Kia Forte | 2017 | 750 |

| #9 | Ford F-150 | $2,006 | 700 |

| #10 | Kia Sportage | 2016 | 650 |

Just because you may not own any of the vehicles on this list doesn’t mean that extra coverage, such as comprehensive, isn’t a good idea. Comprehensive coverage can protect you from vandals, natural disasters, and animal strikes as well.

Read More: Best Car Insurance by Vehicle

Vehicle Thefts by City

Missouri drivers face risks both on the road and from vehicle theft. The data below was gathered from the FBI website and shows the top 10 cities in Missouri in terms of vehicle theft.

Missouri Motor Vehicle Thefts by City

| City | Motor Vehicle Thefts |

|---|---|

| Blue Springs | 128 |

| Columbia | 447 |

| Independence | 1,426 |

| Joplin | 253 |

| Kansas City | 9,053 |

| Lee's Summit | 109 |

| Raytown | 119 |

| Springfield | 977 |

| St. Joseph | 427 |

| St. Louis | 6,203 |

High theft rates in cities like Kansas City and St. Louis drive up insurance costs, but smaller cities aren’t immune. While rear-end collisions and fender benders are the most common claims, costlier incidents like side-impact and single-vehicle accidents still pose a financial burden.

5 Most Common Auto Insurance Claims in Missouri

| Claim Type | Portion of Claims | Cost per Claim |

|---|---|---|

| Rear-End Collision | 28% | $4,500 |

| Fender Bender | 22% | $2,200 |

| Single Vehicle Accident | 18% | $5,800 |

| Side-Impact Collision | 16% | $6,100 |

| Theft Claim | 8% | $9,000 |

Car thefts are rare but costly. Missouri drivers can reduce risks and boost accident preparedness by staying alert, using theft prevention, and carrying the right coverage.

Road Fatalities in Missouri

Missouri’s crash statistics reveal just how significantly weather and visibility impact road safety. With thousands of accidents occurring during normal conditions, the added risk from rain, snow, and poor lighting underscores the importance of driving safely to avoid costly claims and potential fatalities.

Missouri Traffic Crashes by Weather and Light Conditions

| Weather Condition | Daylight | Dark, Lighted | Dark | Dawn/Dusk | Other/Unknown | Total |

|---|---|---|---|---|---|---|

| Normal | 14,701 | 5,590 | 8,294 | 1,249 | 88 | 29,922 |

| Rain | 878 | 515 | 699 | 54 | 8 | 2,154 |

| Snow/Sleet | 241 | 63 | 168 | 13 | 7 | 492 |

| Other | 115 | 52 | 232 | 30 | 11 | 440 |

| Unknown | 833 | 248 | 544 | 57 | 127 | 1,809 |

| TOTAL | 16,768 | 6,468 | 10,937 | 1,403 | 241 | 35,817 |

Rural and urban counties both experience traffic fatalities, but higher-population areas like Jackson and St. Louis consistently show elevated numbers. This reinforces the link between dense traffic, risk exposure, and the need for caution during high-risk conditions such as wet weather.

Missouri County Traffic Fatalities

| County | 2020 Fatalities | 2021 Fatalities | 2022 Fatalities | 2023 Fatalities | 2024 Fatalities |

|---|---|---|---|---|---|

| Adair | 6 | 14 | 18 | 11 | 11 |

| Andrew | 19 | 14 | 15 | 4 | 16 |

| Atchison | 14 | 9 | 15 | 6 | 12 |

| Audrain | 10 | 12 | 2 | 3 | 2 |

| Barry | 7 | 18 | 19 | 5 | 8 |

| Barton | 11 | 14 | 0 | 5 | 13 |

| Bates | 13 | 13 | 18 | 2 | 1 |

| Benton | 18 | 10 | 9 | 6 | 11 |

| Bollinger | 0 | 7 | 8 | 17 | 4 |

| Boone | 17 | 14 | 3 | 11 | 3 |

| Buchanan | 10 | 13 | 3 | 7 | 13 |

| Butler | 0 | 2 | 3 | 18 | 9 |

| Caldwell | 13 | 11 | 10 | 11 | 18 |

| Callaway | 4 | 8 | 6 | 6 | 13 |

| Camden | 3 | 17 | 11 | 13 | 11 |

| Cape Girardeau | 1 | 12 | 15 | 18 | 18 |

| Carroll | 0 | 6 | 2 | 16 | 11 |

| Carter | 11 | 18 | 17 | 18 | 8 |

| Cass | 11 | 1 | 13 | 4 | 6 |

| Cedar | 16 | 9 | 17 | 8 | 13 |

| Chariton | 9 | 12 | 1 | 11 | 19 |

| Christian | 15 | 5 | 2 | 0 | 18 |

| Clark | 14 | 11 | 15 | 0 | 14 |

| Clay | 14 | 11 | 8 | 14 | 15 |

| Clinton | 18 | 19 | 3 | 1 | 4 |

| Cole | 11 | 10 | 0 | 15 | 2 |

| Cooper | 19 | 6 | 3 | 7 | 11 |

| Crawford | 2 | 0 | 0 | 12 | 19 |

| Dade | 4 | 5 | 9 | 4 | 11 |

| Dallas | 9 | 4 | 3 | 0 | 10 |

| Daviess | 17 | 17 | 2 | 5 | 6 |

| Dekalb | 2 | 3 | 7 | 1 | 15 |

| Dent | 18 | 6 | 17 | 18 | 13 |

| Douglas | 13 | 8 | 13 | 4 | 17 |

| Dunklin | 8 | 11 | 13 | 1 | 4 |

| Franklin | 18 | 18 | 12 | 1 | 2 |

| Gasconade | 13 | 3 | 6 | 17 | 5 |

| Gentry | 16 | 10 | 12 | 6 | 11 |

| Greene | 12 | 14 | 5 | 18 | 4 |

| Grundy | 4 | 0 | 1 | 3 | 0 |

| Harrison | 2 | 0 | 14 | 14 | 17 |

| Henry | 5 | 10 | 9 | 7 | 5 |

| Hickory | 7 | 1 | 0 | 5 | 3 |

| Holt | 15 | 1 | 18 | 3 | 9 |

| Howard | 8 | 6 | 8 | 8 | 7 |

| Howell | 4 | 7 | 7 | 1 | 4 |

| Iron | 16 | 8 | 13 | 8 | 9 |

| Jackson | 6 | 15 | 16 | 17 | 14 |

| Jasper | 11 | 19 | 4 | 11 | 10 |

| Jefferson | 18 | 3 | 2 | 14 | 17 |

| Johnson | 0 | 6 | 18 | 6 | 3 |

| Knox | 15 | 1 | 7 | 1 | 5 |

| Laclede | 3 | 13 | 9 | 2 | 10 |

| Lafayette | 5 | 9 | 12 | 14 | 3 |

| Lawrence | 1 | 11 | 2 | 6 | 16 |

| Lewis | 0 | 0 | 2 | 6 | 14 |

| Lincoln | 18 | 13 | 11 | 3 | 8 |

| Linn | 11 | 18 | 14 | 14 | 2 |

| Livingston | 12 | 7 | 0 | 2 | 18 |

| Macon | 17 | 9 | 14 | 8 | 6 |

| Madison | 7 | 10 | 2 | 0 | 1 |

| Maries | 5 | 12 | 13 | 7 | 2 |

| Marion | 3 | 14 | 10 | 6 | 15 |

| Mcdonald | 1 | 5 | 8 | 13 | 5 |

| Mercer | 0 | 17 | 16 | 17 | 10 |

| Miller | 2 | 8 | 5 | 7 | 7 |

| Mississippi | 8 | 4 | 4 | 1 | 3 |

| Moniteau | 1 | 3 | 6 | 9 | 13 |

| Monroe | 11 | 0 | 1 | 8 | 0 |

| Montgomery | 14 | 2 | 17 | 17 | 13 |

| Morgan | 16 | 15 | 3 | 11 | 5 |

| New Madrid | 13 | 14 | 17 | 12 | 10 |

| Newton | 14 | 8 | 10 | 10 | 4 |

| Nodaway | 6 | 7 | 0 | 2 | 6 |

| Oregon | 0 | 1 | 3 | 1 | 11 |

| Osage | 14 | 14 | 10 | 18 | 0 |

| Ozark | 1 | 10 | 12 | 10 | 17 |

| Pemiscot | 5 | 6 | 12 | 13 | 14 |

| Perry | 16 | 1 | 3 | 4 | 10 |

| Pettis | 12 | 3 | 6 | 6 | 1 |

| Phelps | 6 | 5 | 8 | 2 | 6 |

| Pike | 10 | 14 | 15 | 4 | 6 |

| Platte | 17 | 14 | 18 | 6 | 15 |

| Polk | 5 | 17 | 2 | 6 | 6 |

| Pulaski | 2 | 5 | 7 | 1 | 0 |

| Putnam | 1 | 4 | 9 | 11 | 15 |

| Ralls | 8 | 0 | 4 | 14 | 2 |

| Randolph | 6 | 0 | 11 | 10 | 0 |

| Ray | 2 | 1 | 3 | 3 | 15 |

| Reynolds | 15 | 15 | 6 | 17 | 12 |

| Ripley | 0 | 6 | 14 | 17 | 15 |

| Saline | 1 | 14 | 17 | 4 | 14 |

| Schuyler | 15 | 4 | 8 | 8 | 17 |

| Scotland | 7 | 8 | 11 | 6 | 12 |

| Scott | 3 | 4 | 13 | 14 | 18 |

| Shannon | 13 | 4 | 5 | 12 | 6 |

| Shelby | 5 | 4 | 17 | 2 | 13 |

| St. Charles | 8 | 6 | 10 | 9 | 3 |

| St. Clair | 1 | 2 | 5 | 0 | 7 |

| Francois | 3 | 8 | 10 | 17 | 17 |

| St. Louis City | 17 | 3 | 14 | 15 | 6 |

| St. Louis Co. | 18 | 0 | 7 | 8 | 12 |

| Ste. Genevieve | 12 | 16 | 7 | 18 | 2 |

| Stoddard | 0 | 7 | 9 | 5 | 17 |

| Stone | 4 | 6 | 6 | 0 | 2 |

| Sullivan | 8 | 18 | 17 | 8 | 15 |

| Taney | 4 | 7 | 17 | 7 | 6 |

| Texas | 6 | 4 | 12 | 11 | 6 |

| Vernon | 9 | 12 | 0 | 4 | 4 |

| Warren | 11 | 5 | 2 | 3 | 6 |

| Washington | 14 | 11 | 2 | 5 | 15 |

| Wayne | 18 | 17 | 13 | 18 | 0 |

| Webster | 9 | 13 | 3 | 1 | 0 |

| Worth | 0 | 15 | 7 | 3 | 3 |

| Wright | 7 | 14 | 15 | 6 | 14 |

Despite some counties maintaining stable or lower overall fatality numbers, crash deaths remain consistently high in metropolitan areas. These patterns align with areas that also report heavy crash volumes and insurance claims.

Missouri Traffic Fatalities by County

| County | 2019 | 2020 | 2021 | 2022 | 2023 |

|---|---|---|---|---|---|

| Jackson | 114 | 133 | 114 | 111 | 133 |

| St. Louis | 110 | 99 | 110 | 99 | 99 |

| St. Louis City | 71 | 71 | 71 | 71 | 71 |

| St. Charles | 37 | 37 | 37 | 37 | 37 |

| Jefferson | 35 | 35 | 35 | 35 | 35 |

| Greene | 49 | 53 | 49 | 53 | 53 |

| Newton | 21 | 21 | 21 | 21 | 21 |

| Phelps | 21 | 21 | 21 | 21 | 21 |

| Platte | 21 | 21 | 21 | 21 | 21 |

| Clay | 19 | 19 | 19 | 19 | 19 |

Speeding plays a major role in fatal crashes, especially in populous counties like Jackson and St. Louis. The trend emphasizes how excessive speed combined with weather-related hazards can have deadly consequences.

Missouri Speeding-Related Fatalities by County

| County | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Adair | 1 | 0 | 1 | 0 | 1 |

| Andrew | 2 | 1 | 2 | 1 | 2 |

| Atchison | 0 | 1 | 0 | 1 | 0 |

| Audrain | 1 | 2 | 1 | 2 | 1 |

| Barry | 4 | 3 | 5 | 2 | 3 |

| Boone | 5 | 4 | 6 | 5 | 6 |

| Jackson | 52 | 54 | 58 | 61 | 63 |

| St. Charles | 14 | 13 | 12 | 13 | 14 |

| St. Louis City | 29 | 31 | 28 | 30 | 30 |

| St. Louis Co. | 32 | 33 | 34 | 35 | 37 |

Drunk driving also remains a persistent issue, with several counties reporting alcohol-related deaths year after year. It reinforces the importance of proactive safety behavior and responsible choices.

| County | 2013 Alcohol Fatalities | 2014 Alcohol Fatalities | 2015 Alcohol Fatalities | 2016 Alcohol Fatalities | 2017 Alcohol Fatalities |

|---|---|---|---|---|---|

| Adair | 0 | 0 | 0 | 0 | 1 |

| Andrew | 1 | 1 | 0 | 1 | 0 |

| Atchison | 0 | 0 | 0 | 1 | 0 |

| Audrain | 0 | 2 | 0 | 0 | 2 |

| Barry | 5 | 4 | 2 | 4 | 1 |

| Barton | 0 | 1 | 0 | 0 | 0 |

| Bates | 0 | 1 | 0 | 0 | 0 |

| Benton | 1 | 2 | 1 | 0 | 0 |

| Bollinger | 0 | 1 | 1 | 2 | 1 |

| Boone | 3 | 5 | 7 | 8 | 2 |

| Buchanan | 3 | 2 | 3 | 2 | 1 |

| Butler | 2 | 1 | 1 | 2 | 2 |

| Caldwell | 0 | 0 | 1 | 0 | 0 |

| Callaway | 2 | 1 | 7 | 1 | 2 |

| Camden | 4 | 1 | 3 | 3 | 5 |

| Cape Giradeau | 1 | 1 | 3 | 3 | 5 |

| Carroll | 0 | 0 | 0 | 0 | 0 |

| Carter | 2 | 0 | 1 | 0 | 0 |

| Cass | 7 | 1 | 0 | 6 | 1 |

| Cedar | 0 | 1 | 0 | 0 | 1 |

| Chariton | 2 | 1 | 0 | 0 | 0 |

| Christian | 1 | 3 | 1 | 1 | 5 |

| Clark | 1 | 0 | 0 | 1 | 2 |

| Clay | 5 | 3 | 5 | 5 | 6 |

| Clinton | 0 | 2 | 0 | 1 | 0 |

| Cole | 2 | 3 | 2 | 2 | 1 |

| Cooper | 2 | 2 | 0 | 0 | 0 |

| Crawford | 1 | 1 | 0 | 2 | 0 |

| Dade | 0 | 0 | 0 | 0 | 1 |

| Dallas | 0 | 2 | 0 | 2 | 2 |

| Daviess | 1 | 0 | 0 | 1 | 1 |

| Dekalb | 2 | 0 | 0 | 0 | 0 |

| Dent | 1 | 1 | 0 | 0 | 0 |

| Douglas | 1 | 1 | 0 | 0 | 1 |

| Dunklin | 2 | 4 | 4 | 3 | 4 |

| Franklin | 8 | 6 | 5 | 6 | 2 |

| Gasconade | 0 | 1 | 2 | 2 | 2 |

| Gentry | 0 | 0 | 0 | 0 | 0 |

| Greene | 6 | 1 | 8 | 7 | 8 |

| Grundy | 0 | 0 | 1 | 0 | 0 |

| Harrison | 1 | 0 | 0 | 0 | 2 |

| Henry | 0 | 1 | 0 | 1 | 2 |

| Hickory | 0 | 0 | 0 | 1 | 2 |

| Holt | 0 | 0 | 1 | 1 | 0 |

| Howard | 1 | 0 | 0 | 1 | 0 |

| Howell | 3 | 0 | 1 | 2 | 2 |

| Iron | 1 | 0 | 0 | 1 | 0 |

| Jackson | 27 | 19 | 21 | 33 | 39 |

| Jasper | 5 | 1 | 4 | 2 | 4 |

| Jefferson | 8 | 9 | 8 | 9 | 5 |

| Johnson | 9 | 2 | 0 | 3 | 1 |

| Knox | 0 | 0 | 0 | 0 | 0 |

| Laclede | 1 | 2 | 1 | 2 | 1 |

| Lafayette | 1 | 0 | 2 | 1 | 3 |

| Lawrence | 2 | 1 | 3 | 2 | 3 |

| Lewis | 0 | 0 | 0 | 1 | 0 |

| Lincoln | 2 | 6 | 1 | 2 | 2 |

| Linn | 0 | 0 | 0 | 0 | 2 |

| Livingston | 2 | 0 | 0 | 0 | 1 |

| Macon | 0 | 0 | 1 | 0 | 1 |

| Madison | 0 | 1 | 1 | 0 | 0 |

| Maries | 1 | 2 | 0 | 0 | 2 |

| Marion | 1 | 0 | 1 | 1 | 0 |

| Mcdonald | 3 | 3 | 3 | 2 | 3 |

| Mercer | 0 | 0 | 1 | 1 | 1 |

| Miller | 8 | 4 | 3 | 3 | 1 |

| Mississippi | 1 | 0 | 0 | 2 | 1 |

| Moniteau | 1 | 2 | 1 | 1 | 0 |

| Monroe | 0 | 1 | 0 | 0 | 0 |

| Montgomery | 2 | 0 | 1 | 1 | 0 |

| Morgan | 0 | 0 | 2 | 1 | 1 |

| New Madrid | 1 | 3 | 2 | 0 | 1 |

| Newton | 2 | 6 | 1 | 4 | 8 |

| Nodaway | 1 | 2 | 0 | 2 | 1 |

| Oregon | 0 | 0 | 1 | 1 | 1 |

| Osage | 0 | 1 | 0 | 0 | 0 |

| Ozark | 1 | 1 | 0 | 1 | 0 |

| Pemiscot | 1 | 4 | 1 | 0 | 2 |

| Perry | 1 | 2 | 1 | 0 | 1 |

| Pettis | 2 | 4 | 2 | 1 | 2 |

| Phelps | 2 | 1 | 4 | 1 | 4 |

| Pike | 0 | 0 | 2 | 1 | 0 |

| Platte | 3 | 2 | 3 | 5 | 7 |

| Polk | 3 | 0 | 0 | 1 | 1 |

| Pulaski | 5 | 1 | 1 | 2 | 1 |

| Putnam | 0 | 0 | 0 | 0 | 0 |

| Ralls | 1 | 0 | 0 | 3 | 0 |

| Randolph | 1 | 0 | 0 | 0 | 2 |

| Ray | 0 | 2 | 2 | 2 | 1 |

| Reynolds | 0 | 2 | 1 | 1 | 0 |

| Ripley | 2 | 2 | 0 | 2 | 2 |

| Saline | 2 | 1 | 1 | 0 | 0 |

| Schuyler | 0 | 0 | 0 | 3 | 0 |

| Scotland | 0 | 0 | 1 | 0 | 1 |

| Scott | 3 | 2 | 1 | 1 | 0 |

| Shannon | 3 | 0 | 1 | 1 | 1 |

| Shelby | 0 | 0 | 0 | 0 | 0 |

| St. Charles | 6 | 11 | 7 | 7 | 11 |

| St. Clair | 3 | 0 | 2 | 0 | 0 |

| St. Francois | 4 | 3 | 2 | 3 | 2 |

| St. Louis City | 18 | 14 | 16 | 23 | 15 |

| St. Louis County | 15 | 14 | 18 | 21 | 26 |

| Ste. Genevive | 1 | 0 | 1 | 1 | 5 |

| Stoddard | 2 | 0 | 3 | 1 | 3 |

| Stone | 0 | 1 | 2 | 3 | 2 |

| Sullivan | 0 | 2 | 0 | 0 | 0 |

| Taney | 2 | 3 | 5 | 2 | 3 |

| Texas | 0 | 3 | 5 | 3 | 1 |

| Vernon | 1 | 0 | 3 | 1 | 1 |

| Warren | 1 | 1 | 5 | 3 | 1 |

| Washington | 8 | 1 | 2 | 1 | 3 |

| Wayne | 0 | 0 | 0 | 0 | 2 |

| Webster | 2 | 0 | 4 | 2 | 3 |

| Worth | 0 | 0 | 1 | 0 | 0 |

| Wright | 1 | 1 | 1 | 1 | 1 |

Insurance claims data show that cities with more frequent crashes also file more claims, with Kansas City and St. Louis leading the state.

Missouri Accidents & Claims per Year by City

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Blue Springs | 1,300 | 1,500 |

| Columbia | 2,700 | 3,100 |

| Florissant | 1,200 | 1,400 |

| Independence | 2,400 | 2,900 |

| Kansas City | 12,500 | 14,300 |

| Lee's Summit | 1,900 | 2,200 |

| O'Fallon | 1,800 | 2,000 |

| Springfield | 4,500 | 5,200 |

| St. Joseph | 1,600 | 1,900 |

| St. Louis | 11,200 | 13,000 |

These trends point to urban congestion, speeding, and weather as primary contributors to accident volume, making driving safely in rain and wet weather even more important in high-traffic areas.

Fatalities by Crash Type & EMS Response Time

Fatal crashes in Missouri are often caused by specific behaviors, not specific individuals, with single-vehicle incidents and road departures being the most common. Distractions like reaching for a fallen item can be deadly, so staying focused is critical.

Emergency medical services typically arrive in about 21 minutes in rural areas and 12 minutes in urban areas, responding to hundreds of fatal crashes each year. Drive safely, no matter the time of day—your choices behind the wheel can make all the difference.

Missouri Specific Driving Laws

In Missouri, it’s illegal to honk someone else’s horn—or leave your car running unattended.

These quirky laws may seem outdated, but they’re still on the books. Missouri also has plenty of practical driving laws—keep scrolling to learn more.

Statute of Limitations

Missouri residents must meet several legal and documentation requirements to drive legally. The state enforces a five-year statute of limitations for personal injury claims and has unique laws regarding fraud and licensing.

While bicycles and mopeds don’t require registration, operators must have a valid license. To register a vehicle, drivers must provide proof of ownership, insurance, a safety inspection, VIN, and payment, along with a completed title and license application.

Getting a driver’s license requires proof of identity, social security number, and residency, along with passing necessary tests if you're a new driver.Eric Stauffer LICENSED INSURANCE AGENT

Missouri is REAL ID compliant, meaning residents will need a REAL ID to board domestic flights or access federal buildings. To obtain one, you must present identity documents like a U.S. passport, certified birth certificate, or permanent resident card, and proof of lawful U.S. status.

Read More: Do you need a driver’s license to buy a car?

You must also prove you belong here—show your Social Security card, tax form, or pay stub. Missouri has a website to help you gather the papers you need.

Automobile Insurance Fraud in Missouri

Missouri has laws in place to protect drivers from car insurance fraud, with serious penalties such as jail time, fines, and restitution. The Missouri Department of Insurance even offers an online quiz to help residents identify and avoid fraudulent activity.

Types of car insurance fraud include:

- Unbundling: Combining smaller procedures into one to charge more.

- Upcoding: Claiming more serious procedures than actually performed.

- Duplicating: Submitting the same claim to multiple agencies.

Repair shops and insurance providers can also commit fraud, such as overstating damage or failing to deposit premiums.

Consumers can be guilty of fraud for claiming previous injuries or property damage in a car accident or failing to report changes in status.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Transportation in Missouri

Missouri drivers share the road with more than just cars. In rural areas, you might encounter agricultural equipment, while city streets are filled with cars, bikes, and pedestrians. With more people on the road, the risk of incidents increases, making it essential to make an informed decision when purchasing car insurance. Rural areas have less traffic but more fatalities, as fewer people often lead to careless driving.

| Traffic Fatalities | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|

| Total | 757 | 766 | 870 | 947 | 930 |

| Rural | 459 | 471 | 497 | 553 | 465 |

| Urban | 298 | 295 | 372 | 394 | 465 |

Missouri Commute Times

With the average family owning two cars each in the Show-Me State, it is no wonder that commute time in Missouri is around 23 minutes, according to Data USA.

Although your commute may seem like it’s in the Show-Me State, it is actually below the national average, which stands at around 26 minutes.

Read More: Buying a Car

Spending any time in traffic increases your chances of an accident, though, so it is a brilliant idea to consider how far your commute will be and what that will cost you on average before choosing a provider, just like we talked about in the previous sections.

Missouri Commuter Transportation

Given the independence of residents of the Show-Me State, it is no surprise that most choose to travel alone by car to work.

![]()

If you choose to drive alone instead of in a carpool, you are taking on the risk of an accident on your own insurance. To make sure you are adequately covered, you should select the best auto insurance in Missouri.

Read More: Carpooling

Traveling alone by car also means that you are contributing to Missouri’s congestion issues, which is why selecting from the best car insurance companies can help you ensure that you’re covered no matter the driving conditions.

Traffic Congestion in Missouri

Missouri isn’t as congested as cities like Boston or Washington, D.C., but St. Louis and Kansas City still face traffic delays, with residents losing 46-47 hours annually. While congestion is less costly in Missouri, it’s still smart to consider how much insurance you need for your car to balance protection and savings.

Finding Your Perfect Protection in Missouri

Liberty Mutual, Farmers, and Travelers have the best car insurance in Missouri, with unique strengths. Liberty Mutual offers extensive protection and substantial discounts, while Farmers provides exceptional personalized service through its local agent network. Travelers stand out with specialized coverage options like premier new car replacement, which is not available elsewhere.

The average car insurance cost in Missouri ranges from $50-$148 monthly, varying significantly by location. Understanding common risks faced by teen drivers is crucial, as teens account for nearly 40% of state auto claims.

Remember, the ideal policy balances coverage, service, and reliability for your specific needs. Take the first step toward cheaper car insurance rates. Enter your ZIP code to see how much you could save.

Frequently Asked Questions

What is the cheapest car insurance in Missouri?

USAA offers the cheapest car insurance in Missouri, with an average rate of $50 per month. However, it is only available to military members and their families. Nationwide follows with an average rate of $66 per month for broader availability.

What penalties could I face for driving without insurance in Missouri?

Penalties include up to a $300 fine, 15 days in jail, 4 license points, and possible license suspension. You may also receive a ticket for driving without a license if your license is suspended due to insurance violations.

Which insurance company offers the best customer service in Missouri?

State Farm is highly regarded for its customer service, offering reliable coverage and quick claim resolution. With an average rate of $85 per month, it provides both affordability and strong customer service.

What should I do after a car accident in Missouri?

Document the scene, exchange information with other parties, report to police for accidents over $500, send photos of car accidents to your insurance company, and file a claim promptly.

What is the best car insurance for military personnel in Missouri?

USAA is the top choice for military personnel and their families in Missouri, offering cheap auto insurance in Missouri starting at $18 per month and excellent customer service. Explore your car insurance options by entering your ZIP code and finding which companies have the lowest rates.

How much does car insurance cost in Missouri?

The average cost of car insurance in Missouri varies, but on this ranking list, rates range from $50 to $148 per month, depending on the company and coverage level.

What factors affect car insurance premiums in Missouri?

Age, driving record, credit score, vehicle type, and location all impact rates. Car maintenance expenses are not covered by standard insurance, but may affect premiums if poor maintenance leads to accidents.

What are the minimum car insurance requirements in Missouri?

Missouri requires $25,000/$50,000 for bodily injury liability, $10,000 for property damage liability, and $25,000/$50,000 for uninsured motorist coverage to legally drive in the state.

What are the common risks faced by Missouri drivers?

Common risks faced by drivers include distracted driving and inexperience, while all Missouri drivers contend with weather hazards, vehicle theft (particularly Ford pickups), and an uninsured driver rate of 14%. Ready to find cheaper car insurance coverage? Enter your ZIP code to begin.

Related Articles

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.