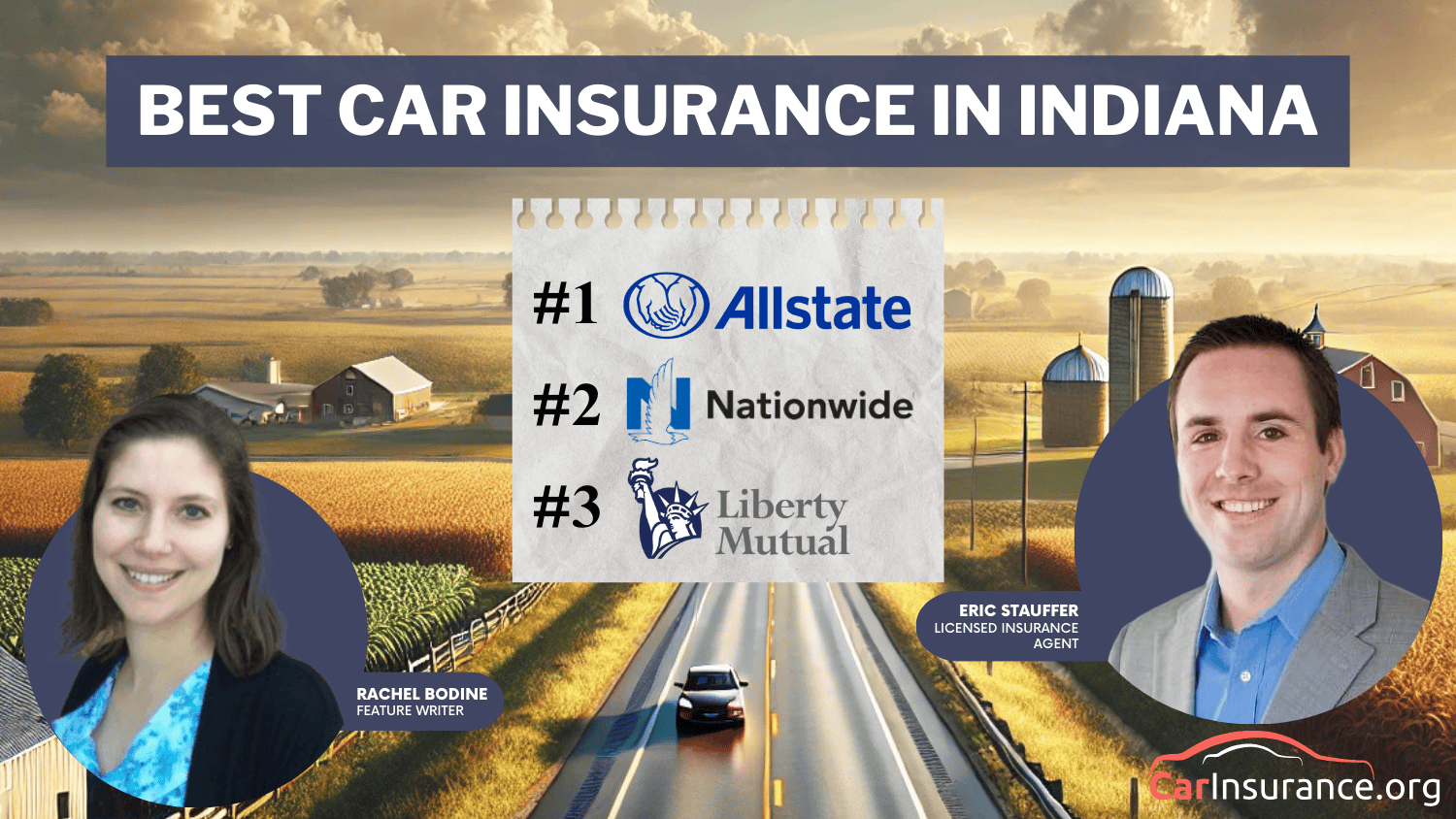

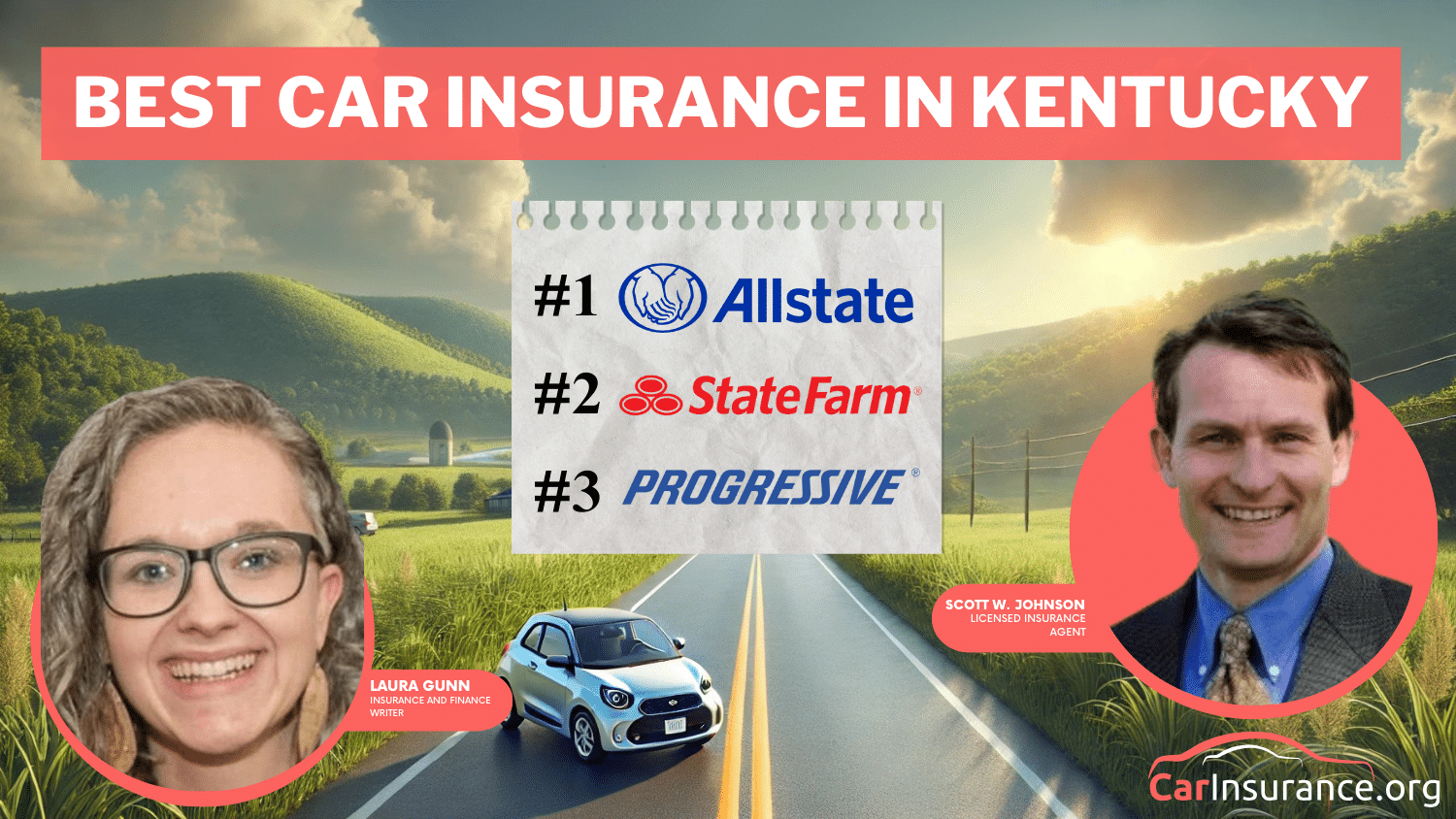

Progressive offers top coverage, Geico leads in Oregon with a great app, and Farmers rewards safe drivers.

Read More: Car Insurance Rates by State

Explore your car insurance options by entering your ZIP code and finding which companies have the lowest rates.