Best Car Insurance in Georgia for 2026 [Review the Top 10 Companies Here]

Travelers, Geico, and State Farm offer the best car insurance in Georgia, with Travelers starting at just $24 per month. These top car insurance companies in GA are known for affordable rates, great discounts, and reliable coverage, making them ideal choices for Georgia drivers seeking quality protection.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Insurance Feature Writer

Rachel Bodine graduated from college with a BA in English. She has since worked as a Feature Writer in the insurance industry and gained a deep knowledge of state and countrywide insurance laws and rates. Her research and writing focus on helping readers understand their insurance coverage and how to find savings. Her expert advice on insurance has been featured on sites like PhotoEnforced, All...

Rachel Bodine

Licensed Insurance Agent

Eric Stauffer is an insurance agent and banker-turned-consumer advocate. His priority is educating individuals and families about the different types of insurance coverage. He is passionate about helping consumers find the best coverage for their budgets and personal needs. Eric is the CEO of C Street Media, a full-service marketing firm and the co-founder of ProperCents.com, a financial educat...

Eric Stauffer

Updated April 2025

19,116 reviews

19,116 reviewsCompany Facts

Full Coverage in Georgia

A.M. Best Rating

Complaint Level

Pros & Cons

19,116 reviews18,157 reviewsCompany Facts

Full Coverage in Georgia

A.M. Best Rating

Complaint Level

Pros & Cons

18,157 reviewsWhen searching for the best car insurance in Georgia, Travelers, Geico, and State Farm are particularly noteworthy due to their distinctive features. Travelers has the cheapest coverage at just $24 a month, which makes it the perfect choice for budget-friendly drivers.

Geico has the best discounts, with savings for safe drivers and military members, making it the perfect option for people wanting to save even more.

Our Top 10 Company Picks: Best Car Insurance in Georgia

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 13% | A++ | Broad Coverage | Travelers | |

| #2 | 25% | A++ | Extensive Discounts | Geico | |

| #3 | 17% | B | Cheap Rates | State Farm | |

| #4 | 20% | A+ | Financial Strength | Nationwide | |

| #5 | 25% | A+ | Comprehensive Options | Allstate | |

| #6 | 25% | A | Personalized Service | American Family | |

| #7 | 20% | A | Flexible Policies | Farmers |

| #8 | 25% | A | Innovative Discounts | Liberty Mutual | |

| #9 | 10% | A+ | Technology Integration | Progressive |

| #10 | 10% | A++ | Military Focus | USAA |

State Farm, with its strong customer service and affordable rates, is ideal for drivers who need affordability and assurance.

- Travelers has the cheapest car insurance rates in Georgia

- Geico offers great discounts for safe drivers

- State Farm is known for its great claim satisfaction

Utilize this car insurance guide to compare the benefits of these leading automobile insurance providers in Georgia and select the best solution for your needs.

Ready to find affordable car insurance? Get started today by entering your ZIP code into our free comparison tool.

#1 – Travelers: Top Overall Pick

Pros

- Full Protection Options: It provides liability, collision, and comprehensive coverage for full protection against all types of risks.

- Cheap Full Coverage Prices: The cheapest plan starts at $24 a month, making it one of the cheapest options for car insurance in Georgia.

- Discounts For Bundling: Policyholders receive discounts of up to 13% by bundling home and automobile insurance for lower premiums overall.

Cons

- Fewer Discount Opportunities: Fewer savings opportunities compared to competitors like Geico and Liberty Mutual.

- Higher Rates for Risky Drivers: Rates can rise significantly for those with past accidents or traffic violations, as noted in this Travelers car insurance review.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#2 – Geico: Best for Extensive Discounts

Pros

- Big Savings Opportunities: Drivers can score up to 25% off through bundling, military perks, and safe driving discounts, making coverage more affordable.

- Low-Cost Minimum Coverage: With rates as low as $24 per month, it’s one of the most budget-friendly choices for Georgia drivers needing basic protection.

- Strong Financial Standing: Holding an A++ rating from A.M. Best, this insurer ensures financial security and smooth claims, as noted in many Geico car insurance reviews.

Cons

- Higher Full Coverage Costs: Compared to options like State Farm and Travelers, full coverage plans tend to be more expensive.

- Limited Local Agent Access: Since this provider mainly operates online, it may not be ideal for drivers who prefer in-person help when shopping for car insurance quotes in GA.

#3 – State Farm: Best for Cheap Rates

Pros

- Great for Young Drivers in Georgia: Offers student discounts and training programs. State Farm car insurance review highlights these perks for teens and students.

- Personalized Support from Local Agents: Numerous agents statewide offer in-person help, making it easier for Georgia drivers to manage policies and claims efficiently.

- Bundling Perks for Bigger Savings: Georgia drivers can save up to 17% by combining home and auto insurance, reducing overall costs under a single provider.

Cons

- Fewer Discount Opportunities Available: It offers less variety in savings programs than competitors like Geico and Liberty Mutual, limiting options for Georgia drivers to cut costs.

- Claims Processing: Some policyholders complain of delays in handling claims, which can be irritating when handling auto insurance quotes in Georgia following an accident.

#4 – Nationwide: Best for Financial Strength

Pros

- Reliable Financial Strength in Georgia: With an A+ rating, Nationwide car insurance reviews reveal its smooth claims processing and long-term security for policyholders.

- Budget-Friendly Full Coverage Options: Monthly premiums start at $61, making it affordable for drivers needing more coverage than the state’s minimum.

- SmartRide Rewards Safe Driving Habits: The app allows safe drivers to save up to 40%, helping them secure the best Georgia GA car insurance quotes for lower rates.

Cons

- Fewer Local Agents for In-Person Help: Nationwide has fewer in-person service locations in Georgia than major competitors like State Farm and Allstate.

- Higher Costs for Basic Coverage: Minimum coverage rates are higher than those of budget-friendly insurers like Geico, making it less appealing for cost-conscious drivers.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#5 – Allstate: Best for Comprehensive Option

Pros

- Wide Coverage Options: Includes accident forgiveness, new car replacement, and rideshare coverage, ensuring drivers have full protection.

- Big Bundling Savings: Home and auto policyholders can combine coverage and save up to 25% on their premiums, making it a cost-effective option.

- Drivewise Discount Perks: Safe driving habits can help lower premiums through real-time tracking, offering personalized savings opportunities.

Cons

- Higher Risk Rates: Rates for those with past accidents or violations may rise significantly compared to the average car insurance in Georgia.

- Claims Process Concerns: As noted in the Allstate car insurance review, some policyholders report slow processing times and delays, which impact reliability.

#6 – American Family: Best for Personalized Service

Pros

- Dedicated Local Agents: American Family car insurance reviews highlight its strong focus on customer support since local agents provide tailored plans.

- Big Bundling Discounts: Georgia drivers can save up to 25% by combining auto and home insurance with one provider, making coverage more affordable.

- Extra Coverage Options: Includes add-ons like roadside assistance and rental car reimbursement, offering extra security for Georgia drivers.

Cons

- Fewer Service Locations: This insurer has fewer in-person service locations than larger providers, which may affect convenience for some.

- Higher Coverage Costs: Coverage in Georgia is pricier than budget-friendly auto insurers in Georgia like Geico and Travelers, making it less cost-effective.

#7 – Farmers: Best for Flexible Policies

Pros

- Customizable Coverage Options: Our Farmers car insurance review discusses add-ons like OEM parts and full windshield coverage for better protection.

- Bundling Discounts Available: Save up to 20% when combining home and auto insurance, making it easier to lower costs in Georgia.

- Roadside Assistance 24/7: Get affordable emergency services as an add-on, ensuring help is available whenever you need it.

Cons

- Higher Rates for Risks: Those with accidents or DUIs can expect higher premiums, which increases the cost of coverage in Georgia.

- Claims Processing Concerns: A few customers complain about slower claims processing, which impacts the average Georgia car insurance experience.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#8 – Liberty Mutual: Best for Innovative Discounts

Pros

- Exclusive Georgia Discounts: Discounts offer savings with paperless billing and RightTrack telematics, rewarding safe driving habits and helping reduce costs.

- Affordable for High-Risk Drivers: This Liberty Mutual car insurance review reveals lower rates for drivers with past accidents or traffic violations.

- Financial Strength: Receives an A rating by A.M. Best, making Georgia motorists able to count on its financial stability and policyholder protection.

Cons

- Higher Minimum Coverage Prices: It is pricier than Geico, increasing the cost of auto insurance rates Georgia motorists pay for minimum coverage.

- Limited Local Agents: It has fewer in-person service locations than Allstate and State Farm, reducing accessibility for Georgia policyholders.

#9 – Progressive: Best for Technology Integration

Pros

- Customizable Pricing Tool: The Progressive car insurance review highlights the Name Your Price tool, which helps Georgia drivers personalize policies to fit their budgets.

- Safe Driving Discounts: The Snapshot telematics program rewards good driving with up to 30% savings, making it easier for responsible drivers to lower their premiums.

- Competitive Rates Offered: This company offers reasonably priced plans, particularly for drivers with good records, making insurance more affordable in Georgia.

Cons

- Increased Charges for Risk Drivers: Car insurance costs in Georgia tend to be higher for accident-prone drivers or those convicted of DUIs, resulting in increased monthly fees.

- Inconsistent Customer Support: Certain policyholders report mixed experiences when making claims or requesting assistance with their insurance policies.

#10 – USAA: Best for Military Focus

Pros

- Military-Focused Coverage: Designed for service members, offering unique benefits and discounts to those who qualify.

- Affordable Veteran Rates: Provides some of the most budget-friendly options for active and retired military personnel seeking coverage.

- Highly Rated Service: Consistently earns high marks for claims handling and service, as seen in many USAA car insurance reviews.

Cons

- Limited Membership: Only military members, veterans, and their families can qualify for coverage, limiting availability.

- Few GA Locations: Unlike some auto insurance companies in Georgia, residents know USAA mainly operates online, reducing in-person service.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Understanding Georgia Car Insurance Coverage and Rates

Finding the best car insurance in Georgia means comparing rates. Geico offers the lowest, with a minimum coverage of $24 per month and a full coverage of $61 per month, while Liberty Mutual offers the highest. Shopping around helps drivers save.

Georgia Car Insurance Monthly Rates by Provider & Coverage

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $66 | $165 | |

| $50 | $124 | |

|

| $60 | $149 |

| $24 | $61 | |

| $106 | $263 | |

| $61 | $152 | |

|

| $46 | $115 |

| $43 | $107 | |

| $44 | $110 | |

| $29 | $71 |

The average car insurance rates in Georgia vary by coverage level. Liberty Mutual has the highest, from $803 to $877 per month, while Geico and USAA are cheaper. Higher coverage costs more, but it offers better financial protection.

Choosing car insurance for Georgia depends on factors like driving history and location. Geico and USAA have lower rates, while Liberty Mutual and Nationwide charge more but may offer added benefits.

Georgia Auto Insurance Monthly Rates by Coverage Level for Top Providers

| Insurance Company | Low | Medium | High |

|---|---|---|---|

| $323 | $355 | $375 | |

| $267 | $292 | $333 | |

|

| $308 | $342 | $375 |

| $230 | $249 | $265 | |

| $803 | $833 | $877 | |

| $528 | $550 | $543 | |

|

| $343 | $369 | $412 |

| $264 | $282 | $300 | |

| $292 | $317 | $350 | |

| $251 | $262 | $276 |

The 10 cheapest car insurance companies provide affordable rates with good coverage. Minimum coverage is the cheapest, but full coverage gives more security. Comparing insurers and discounts helps drivers save.

Georgia Car Insurance Accident and Claims

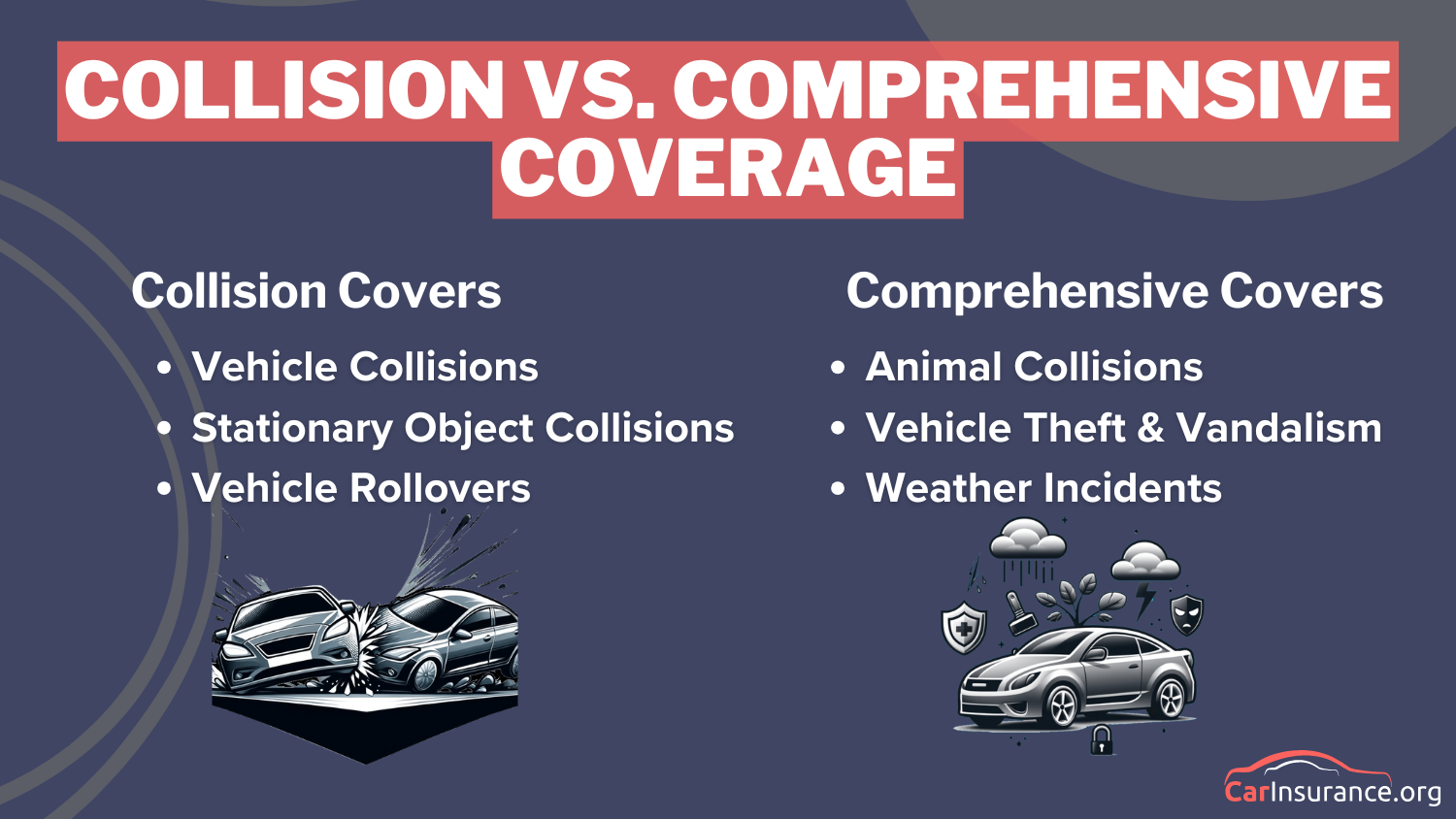

Collision insurance covers crash-related damages, including rollovers and hitting objects. With frequent Car Accidents & Claims, this coverage helps drivers avoid costly repairs in high-traffic areas.

Comprehensive insurance covers theft, vandalism, and weather-related damage. Many looking for the best car insurance in Georgia choose both coverages to ensure protection against unexpected incidents.

Accidents vary across cities. Atlanta reports 20,000 crashes yearly, leading to 15,000 claims, while Macon has fewer. Comparing car insurance quotes, Georgia helps drivers find suitable coverage.

Georgia Accidents & Claims per Year by City

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Atlanta | $20,000 | $15,000 |

| Augusta | $4,500 | $3,800 |

| Columbus | $4,000 | $3,500 |

| Macon | $3,000 | $2,700 |

| Savannah | $5,000 | $4,000 |

Savannah and Augusta report thousands of yearly crashes, emphasizing the need for the best car insurance in Georgia. Traffic, road conditions, and driver habits influence the number of car accidents & claims.

Collision claims account for 30% of all claims, costing an average of $3,500, while comprehensive claims cover 25%. Drivers compare car insurance quotes in Georgia to find policies that fit their needs.

5 Most Common Auto Insurance Claims in Georgia

| Claim Type | Portion of Claims | Cost per Claim |

|---|---|---|

| Collision | 30% | $3,500 |

| Comprehensive | 25% | $2,800 |

| Uninsured Motorist | 20% | $4,200 |

| Bodily Injury | 15% | $15,000 |

| Property Damage | 10% | $5,000 |

Bodily injury claims are costly at $15,000 per claim, while property damage averages $5,000. Many drivers check the average car insurance cost in Georgia to ensure they have sufficient coverage.

Georgia Car Insurance Minimum Coverage

Understanding Georgia’s car insurance requirements is essential. Liability insurance is required and pays for damages you inflict on others. While minimum coverage lowers costs, Georgia’s average car insurance cost could be higher if an accident exceeds your limits.

Drivers must be insured against both property damage and physical harm. Bodily injury liability coverage pays for medical costs if you injure someone, while property damage liability covers vehicle or property repairs. Georgia requires at least $25,000 per person, $50,000 per accident, and $25,000 for property damage.

Travelers offers reliable coverage with flexible options, making it a top choice for Georgia drivers seeking both affordability and protection.Eric Stauffer Licensed Insurance Agent

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Car Insurance Rates by Provider, Age, Gender, and Driving Record in GA

In Georgia, age, gender, and driving history affect rates. Teen drivers pay the most, with male teens slightly higher. Finding affordable car insurance in GA means comparing rates.

Georgia Auto Insurance Monthly Rates by Provider, Age, & Gender

| Insurance Company | Age: 17 Female | Age: 17 Male | Age: 25 Female | Age: 25 Male | Age: 35 Female | Age: 35 Male | Age: 60 Female | Age: 60 Male |

|---|---|---|---|---|---|---|---|---|

| $410 | $435 | $185 | $205 | $150 | $165 | $140 | $155 | |

| $390 | $420 | $180 | $200 | $145 | $160 | $135 | $150 | |

|

| $405 | $440 | $190 | $210 | $155 | $170 | $145 | $160 |

| $375 | $400 | $170 | $190 | $135 | $150 | $125 | $140 | |

| $420 | $450 | $195 | $215 | $160 | $175 | $150 | $165 | |

| $395 | $425 | $185 | $205 | $150 | $165 | $140 | $155 | |

|

| $400 | $430 | $180 | $200 | $140 | $155 | $130 | $145 |

| $370 | $390 | $165 | $185 | $130 | $145 | $120 | $135 | |

| $385 | $415 | $175 | $195 | $140 | $155 | $130 | $145 | |

| $350 | $375 | $160 | $180 | $125 | $140 | $115 | $130 |

Rates vary by age and gender. A 17-year-old male with Allstate pays $435, while a female pays $410. Average Georgia car insurance rates drop with age. USAA and State Farm have lower premiums.

Driving history impacts rates. A clean record with Geico costs $120, but a DUI raises it to $220. Tickets and accidents increase costs. Comparing insurers helps find affordable car insurance in GA.

Georgia Auto Insurance Monthly Rates by Provider & Driving Record

| Insurance Company | Clean Record | One Ticket | One Accident | One DUI |

|---|---|---|---|---|

| $150 | $180 | $210 | $250 | |

| $140 | $170 | $200 | $240 | |

|

| $145 | $175 | $205 | $245 |

| $120 | $150 | $180 | $220 | |

| $160 | $190 | $220 | $270 | |

| $130 | $160 | $190 | $230 | |

|

| $135 | $165 | $195 | $235 |

| $125 | $155 | $185 | $225 | |

| $140 | $170 | $200 | $240 | |

| $110 | $140 | $170 | $210 |

Finding the Best Car Insurance in Georgia

Discovering the appropriate car insurance in Georgia is a process of comparing prices, coverage, and discounts. From affordable auto insurance, GA, or one that recognizes good driving behavior, by way of these five steps, you can obtain the best value for money.

Here are five key steps to help you navigate the process and secure the best deal for your needs.

- Compare the Best Providers: To get affordable car insurance in GA, compare car insurance companies like Travelers, Geico, and State Farm based on coverage, rates, and discounts.

- Know Georgia’s Minimum Coverage Requirements: Georgia requires liability coverage, but upgrading to full coverage or car insurance with telematics can improve financial protection and savings.

- Compare Rates to Find the Best Deal: The cost of auto insurance in Georgia varies depending on the driver’s profile, so using tools to gather auto insurance quotes, GA helps find the lowest rates.

- Maximize Discounts to Save on Premiums: Many insurers provide discounts for combining insurance and safe driving, as well as car insurance with telematics, which rewards responsible drivers.

- Choose the Right Policy for Your Needs: Reviewing auto insurance quotes GA from multiple providers ensures the best balance of cost, coverage, and service.

By following these steps, you get cheap car insurance GA while getting the right coverage. Quote comparison, discounting, and car insurance with telematics can reduce expenses without sacrificing protection.

Ready to find cheaper car insurance coverage? Enter your ZIP code to begin.

Frequently Asked Questions

What factors influence car insurance rates in Georgia?

Car insurance rates in Georgia depend on your driving history, age, location, and the coverage level you select. Urban areas with higher traffic tend to have higher rates. Look at the factors that affect the price of car insurance for expanded insights.

What is the difference between minimum and full coverage in Georgia?

Minimum coverage meets Georgia’s state requirements and covers liability for accidents you cause, while full coverage includes additional protections like collision and comprehensive insurance.

How do I qualify for discounts with car insurance companies in Georgia?

Numerous insurers provide discounts for policy bundling, safe driving, or certain safety features on your car. Check with providers for specific offers. Ready to find cheaper car insurance coverage? Enter your ZIP code to begin.

Can my car insurance rate change after an accident in Georgia?

Yes, your premium may increase after an accident, especially if you’re found at fault. The increase depends on your insurer’s policies and your driving history. Find out what things you do that can raise your premiums.

What are the benefits of bundling home and car insurance in Georgia?

Bundling home and car insurance often leads to significant discounts, streamlining your policies under one provider for added convenience and cost savings.

How can I get personalized car insurance quotes in Georgia?

You can request quotes directly from insurance providers or use online comparison tools to view multiple options tailored to your needs, driving history, and location.

Is it worth adding comprehensive coverage in Georgia?

If you want protection against incidents like theft, vandalism, or natural disasters, comprehensive coverage is a smart choice, especially in areas prone to such risks. Learn how to drive safely, no matter the time of day.

What are the most common types of claims in Georgia?

The most common car insurance claims in Georgia include collision, uninsured motorist, bodily injury, and property damage. Collision and comprehensive claims are the most frequent.

Are there any car insurance options specifically for military families in Georgia?

Yes, USAA offers exclusive discounts and coverage tailored for military members and their families, providing competitive rates and high customer service ratings. Find cheap car insurance quotes by entering your ZIP code here.

How does my driving history affect my insurance rates in Georgia?

A clean driving record may lead to cheaper insurance, while accidents, speeding tickets, or DUIs can raise rates. Insurers assess risk based on past behavior. Read how to file a car insurance claim after an accident.

Related Articles

-

Mar 2025

Best Car Insurance in Kentucky for 2026 [Find the Top 10 Companies Here]

-

Feb 2025

Best Car Insurance in Vermont for 2026 [Your Guide to the Top 10 Companies]

-

Apr 2025

Best Car Insurance in Wisconsin for 2026 [Check Out the Top 10 Companies]

-

Mar 2025

Best Car Insurance in California for 2026 [Check Out These 10 Companies]

-

May 2025

Best Car Insurance in Minnesota for 2026 [MN’s Top 10 Companies]

-

Mar 2025

Best Car Insurance in New Jersey for 2026 [Compare the Top 10 Companies]

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.