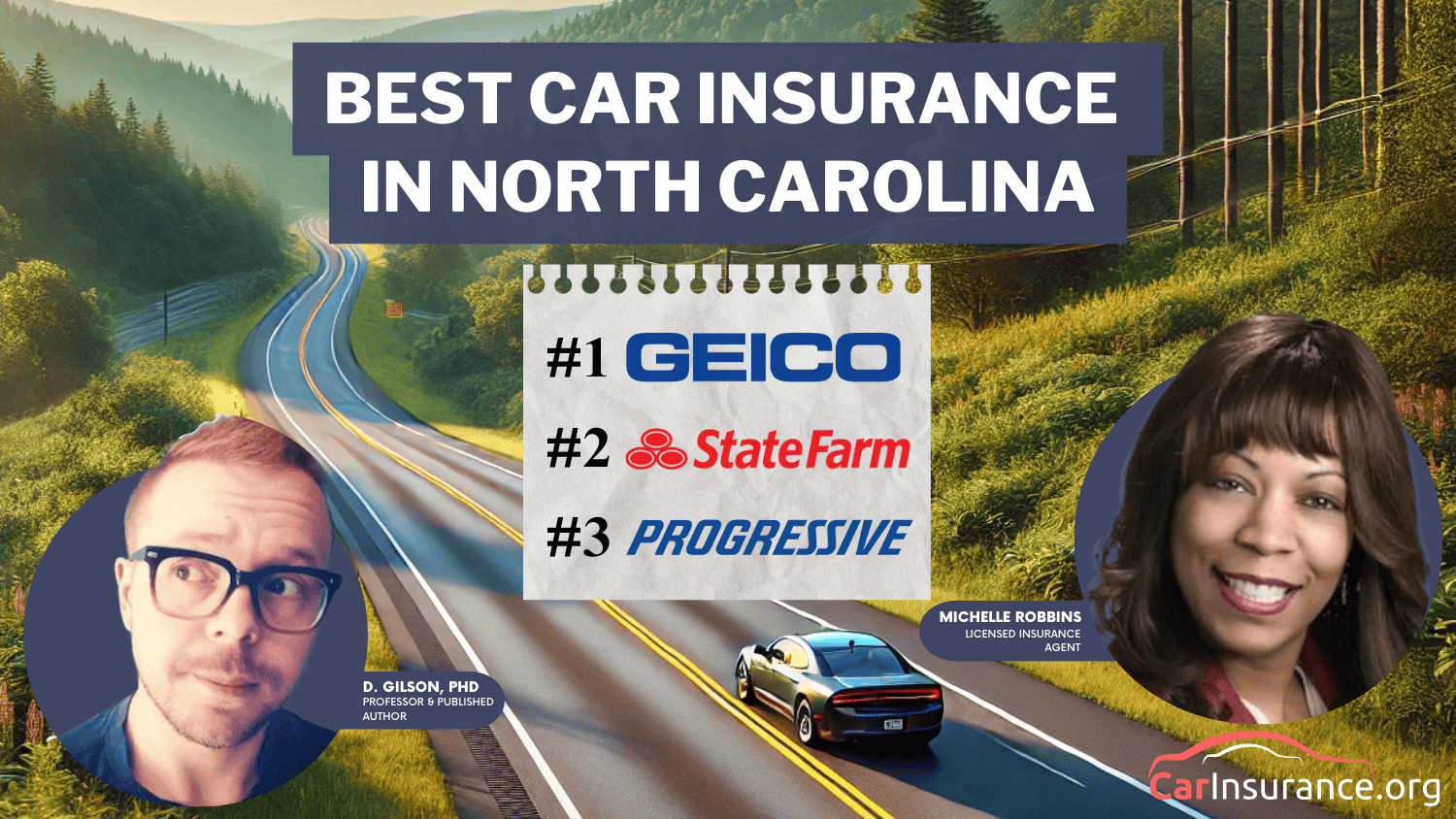

Best Car Insurance in North Carolina for 2026 [10 Standout Companies]

Geico, State Farm, and Progressive offer the best car insurance in North Carolina, with rates as low as $13/month. Geico stands out for its accident forgiveness program. State Farm has a vast network of expert local agents while Progressive is a great option for high-risk drivers.

Quote’s drivers have found rates as low as $42/month in the last few days!

Updated Jul 2025

Is State Farm Insurance good? As one of the most popular providers in the country, State Farm boasts strong fi... more

Is State Farm Insurance good? As one of the most popular providers in the country, State Farm boasts strong financial ratings and positive customer reviews. State Farm homeowners insurance reviews rank it in the top ten for claims satisfaction. Coverage is also available in all 50 states, which is important to Florida less

Learn more about Liberty Mutual Insurance, what products they offer, what their consumers think about them and... more

Learn more about Liberty Mutual Insurance, what products they offer, what their consumers think about them and how they compare against other carriers. less

For more than 90 years, American Family has been protecting and supporting its customers with strong customer ... more

For more than 90 years, American Family has been protecting and supporting its customers with strong customer service. They claim to be more than just an insurance company. They want to transform the way you think about insurance. At AmFam, they believe your dreams are important and that is why they work hard to protec less

Learn more about Progressive Insurance, what products they offer, what their consumers think about them and ho... more

Learn more about Progressive Insurance, what products they offer, what their consumers think about them and how they compare against other carriers. less

D. Gilson is a writer and author of essays, poetry, and scholarship that explore the relationship between popular culture, literature, sexuality, and memoir. His latest book is Jesus Freak, with Will Stockton, part of Bloomsbury’s 33 1/3 Series. His other books include I Will Say This Exactly One Time and Crush. His first chapbook, Catch & Release, won the 2012 Robin Becker Prize from Seve...

Michelle Robbins has been a licensed insurance agent for over 13 years. Her career began in the real estate industry, supporting local realtors with Title Insurance. After several years, Michelle shifted to real estate home warranty insurance, where she managed a territory of over 100 miles of real estate professionals. Later, Agent Robbins obtained more licensing and experience serving families a...

When looking for the best car insurance in North Carolina, drivers should take advantage of affordable rates and comprehensive discounts. Geico, State Farm, and Progressive offer great NC auto insurance.

Geico offers 25% bundling discounts and cheap full coverage. State Farm stands out with its broad network of local agents, while Progressive has flexible options that allow you to find the best policy when buying car insurance.

Our Top 10 Company Picks: Best Car Insurance in North Carolina

Protect your vehicle from whatever the road throws at it by entering your ZIP code into our free comparison tool to find affordable car insurance quotes in NC.

JUST THE BASICS

North Carolina requires minimum liability coverage of 30/60/25

State Farm excels with its extensive local agent network in NC

Geico has affordable car insurance rates at $13 monthly

Low-Cost Coverage: Continuously provides some of the lowest rates for NC residents, making them a top choice for policyholders searching for cheap car insurance.

Strong National Coverage: Geico’s extensive network covers all 50 states, so NC drivers who frequently travel or relocate can rely on it.

Significant Bundling Discount: Motorists in NC can save up to 25% by bundling multiple policies. To gather additional information, read our Geico car insurance review.

Cons

Limited Local Agents: Unlike other NC car insurance companies, Geico relies heavily on online and phone-based service, which may not appeal to drivers who prefer in-person support.

Potentially Higher Rates for High-Risk Drivers: NC drivers with tickets or accidents might experience expensive rates from companies specializing in high-risk policies.

Best for Agent Personal Service: State Farm offers an enormous local network of agents for North Carolina drivers who prefer personalized face-to-face service.

Solid Customer Satisfaction Ratings: Consistently ranks high for claims handling and policyholder support, making it one of NC’s best car insurance choices.

Decent Discounts for Bundling: NC residents who bundle home and auto policies can save up to 17%. Check out our State Farm car insurance review for additional information.

Cons

Slightly Higher Premiums: State Farm’s rates can be higher than Geico or Progressive, especially for young drivers in North Carolina.

Low Ratings in Financial Stability: With a B rating from A.M. Best, its financial stability isn’t as strong as some competitors offering the best car insurance in NC.

#3 – Progressive: Best for Competitive Rates

Pros

Competitive Premiums: Progressive offers some of the most affordable rates, particularly for high-risk drivers in North Carolina.

Strong Digital Tools: The Name Your Price® tool and Snapshot® program help NC motorists find customized pricing based on their driving habits.

Wide Range of Discounts: NC residents can save through bundling, safe driving, and homeowners discounts. Read our Progressive car insurance review for further insights.

Cons

Lower Customer Satisfaction Ratings: Some North Carolina policyholders report issues with claims handling and unexpected rate increases.

Smaller Bundling Discount: At only 10%, its bundling discount is lower than other companies offering the best car insurance in North Carolina.

#4 – Allstate: Best for Drivewise Program

Pros

Drivewise Program Rewards Safe Driving: North Carolina drivers can save by enrolling in Allstate’s telematics program, which rewards good driving habits.

Strong Bundling Discounts: NC drivers can bundle automobile and home insurance and save up to 25% discount.

Various Policy Options: This policy provides accident forgiveness and deductible rewards and is a strong option for NC motorists looking for extra protection.

Cons

Higher Premiums: North Carolina drivers may find Allstate’s rates higher than those of Geico and Progressive.

Not-so-Reliable Claims Process: Some NC policyholders report inconsistent claims handling. Learn more in our Allstate car insurance review.

#5 – Liberty Mutual: Best for Accident Forgiveness

Pros

Accident Forgiveness: Helps North Carolina motorists avoid premium increases after their first accident.

Customizable Policies: NC drivers can tailor policies to their specific coverage needs. For additional information, read our Liberty Mutual car insurance review.

Substantial Bundling Discounts: Offers up to 25% off when North Carolina residents bundle multiple policies.

Cons

Rates Can Be High Without Discounts: NC drivers who do not qualify for discounts are often subjected to higher premium coverage rates.

Significant Claims Process Complaints: Some North Carolina resident drivers report slow-paced claims handling.

#6 – USAA: Best for Military Benefits

Pros

Special Benefits for Military: USAA offers some of the best car insurance in North Carolina for active-duty military veterans and their families.

Highly Rated Customer Service: Consistently receives top marks for claims satisfaction among military families in NC.

Discounts for Military Members: This includes savings for garaging vehicles on military bases and low-mileage driving, which is beneficial for NC service members.

Cons

Limited Eligibility for Non-Military Affiliates: Only available to military personnel, veterans, and their families. Look into our USAA car insurance review for more details.

No Physical Branches for Assistance: North Carolina military families may rely on online or phone-based service.

#7 – Farmers: Best for Personalized Service

Pros

Excellent Local Agent Network: Provides highly personalized service, ideal for NC drivers who prefer one-on-one support.

Customizable Coverage Options: North Carolina residents can tailor policies to meet their needs. For further details, take a closer look at our Farmers car insurance review.

Generous Bundling Discount: Up to 20% off for North Carolina policyholders bundling home and auto insurance.

Cons

Higher Premiums: Farmers’ premiums can be more expensive than other car insurance options in North Carolina.

Limited Online Tools: NC drivers may find Farmers’ digital experience less advanced than that of competitors.

Substantial Bundling Discounts: Up to 20% off for North Carolina drivers bundling auto and home insurance.

Vanishing Deductible Feature: Rewards safe drivers in North Carolina by reducing deductibles over time.

Wide Range of Policy Options: Includes roadside assistance, rental car reimbursement, and accident forgiveness for NC motorists.

Cons

Limited Availability in Some States: North Carolina residents should confirm coverage options before signing up.

Higher Premiums for Some Drivers: Young drivers in NC may find better rates with Geico or Progressive. Get more information by reading our Nationwide car insurance review.

#9 – Travelers: Best for Green Coverage

Pros

Eco-Friendly Insurance Options: Provides discounts for North Carolina motorists with hybrid or electric vehicles.

Good Coverage Options: Includes accident forgiveness and new car replacement for North Carolina drivers.

Competitive Rates for Safe Drivers: Rewards NC policyholders with clean driving records.

Cons

Fewer Local Agents: North Carolina drivers may rely on online or phone support.

Discounts Aren’t as high as Competitors: Bundling discount is only 13%. For extra details, check our Travelers car insurance review.

#10 – American Family: Best for Customizable Policies

Pros

Customizable Policies: North Carolina motorists can choose from add-ons, including gap insurance and accident forgiveness.

Substantial Bundling Discount: Provides up to 25% savings when NC residents bundle policies.

Local Agent Support: Offers in-person assistance for North Carolina policyholders. To learn more, read our American Family car insurance review.

Cons

Limited Availability in Few Cities: Not available in all states, including some parts of NC.

Higher Rates for Some Drivers: Young drivers in NC may find cheaper options elsewhere.

Car Insurance Monthly Rates in NC by Provider & Coverage Level

Evaluating what you need to know when buying a car includes finding a policy that balances affordability with quality protection. Choosing the right car insurance in North Carolina is essential for securing the best coverage and savings.

North Carolina Car Insurance Monthly Rates by Provider & Coverage Level

Whether you’re looking for car insurance companies in NC with a strong national reputation, local agent support, or competitive pricing, comparing options can help you secure the best car insurance in North Carolina for your budget and driving habits

Lower Your Rates With Car Insurance Discounts in North Carolina

Finding the best car insurance in North Carolina isn’t just about the cheapest policy—it’s about the best coverage for your needs. Compare car insurance quotes in North Carolina by shopping around, asking questions, and checking for discounts like bundling, safe driving programs, and anti-theft savings.

Car Insurance Discounts From the Top Providers in North Carolina

Insurance Company

Available Discounts

Drivewise, Multi-Policy (Bundling), Early Signing, Good Student, Safe Driving Club, Anti-Theft, FullPay, Responsible Payer

KnowYourDrive, Multi-Policy (Bundling), Loyalty, Low Mileage, Good Student, Early Bird, Generational, Defensive Driving

Signal, Good Student, Multi-Policy (Bundling), Homeowner, Alternative Fuel, Anti-Theft, Affinity, Responsible Driver

Good Driver, Military, Multi-Vehicle, Bundling, Anti-Theft, Good Student, Defensive Driving, Emergency Deployment

Multi-Policy (Bundling), New Vehicle, Good Student, Safe Driver, Multi-Car, Vehicle Safety, Paperless, Early Shopper

Top insurers offer discounts for safe drivers, students, and multi-policy holders. Use the Department of Insurance’s tools to verify licensed providers and avoid scams. Also, follow safe driving tips to stay accident-free and qualify for even lower rates.

Minimum Coverage Requirements in North Carolina

To legally drive, North Carolina requires minimum liability coverage of 30/60/25 and matching uninsured/underinsured motorist coverage. These cover damages to others if you’re at fault, but they don’t cover your own vehicle.

Minimum Coverage Insurance Requirements in North Carolina

While North Carolina car insurance companies offer extra protection like collision and comprehensive, they aren’t required. The state follows an at-fault system, not no-fault, so choosing the best car insurance in North Carolina ensures better financial protection.

Additional North Carolina Automobile Insurance Coverage Requirements

In North Carolina, you can prove financial responsibility with a Certificate of Self-Insurance if you meet specific criteria, like having at least 26 vehicles. Alternatively, you can use a surety bond or security deposit, but these options are generally more expensive than traditional policies.

Additional Coverage Requirements in North Carolina

While the state requires minimum liability coverage, additional protections like collision and comprehensive are optional. If you choose these, keep in mind that you can’t pay your deductible if the coverage doesn’t apply in certain situations, and these options help protect you in more cases.

Proof of Auto Insurance in North Carolina

In North Carolina, you must carry proof of coverage like SR-22 Insurance, whether it’s through North Carolina auto insurance companies or an approved alternative. This proof can be an insurance card, self-insurance certificate, certificate of deposit, or surety bond, each containing specific details.

Choosing the right NC car insurance is about finding a provider that meets your state legal requirements.

Daniel Walker

Licensed Insurance Agent

Filing a car insurance claim after a road accident can be a headeache, that’s why reading this article can help clarify what to do next for drivers involved in an accident. Make sure you keep the required documents on hand to avoid penalties and ensure you meet state requirements.

Steps to Get a Driver’s License in North Carolina

Here are the requirements to obtain your Limited Learner Permit:

Be between 15 and 18 years old

Complete a driver education course

Have a Driving Eligibility Certificate or a high school diploma or equivalent

Pass the vision test

Pass the written test and sign test

Pay the limited learner permit fee of $15.00 (subject to change)

Cash, money order, or personal check

Here are the requirements to obtain your Limited Provisional License:

Be between 16 and 18 years old

Have your learner permit for at least 12 months

Have no convictions of moving violations within 6 months of applying

Pay the limited provisional license fee of $15.00 (subject to change)

Cash, money order, or personal check

Here are the requirements to obtain your Full Provisional License:

Be between 16 ½ and 18 years old

Have your limited provisional license for at least 6 months

Have no convictions of moving violations within 6 months of applying

Pay the full provisional license fee of $4.00/yr (subject to change)

Cash, money order, or personal check

The following documents are required for application if you are under the age of 18:

Original birth certificate

Original social security card

Driving Eligibility Certificate or a high school diploma or equivalent

Here are the requirements to obtain your first Driver’s License if you are over the age of 18:

Pass the vision test

Pass the written test and sign test

Pass the driving test

You can obtain a learner permit, which will allow you to practice and learn how to drive before taking the driving test. To obtain a learner permit, pass the vision, signs, and written tests. (Read about learner’s permit insurance coverage).

Pay the driver’s license fee of $4.00/yr (subject to change)

Cash, money order, or personal check

The following documents are required for application if you are over the age of 18:

One document showing proof of residency

Two documents showing proof of age and identity

One document showing proof of financial responsibility

In North Carolina, high school students under 18 must complete a driver’s education to get a license. The course takes 30 hours of classroom instruction, a vision test, and behind-the-wheel training, ending with a Driving Eligibility Certificate.

New drivers should review the North Carolina auto insurance guide to understand coverage options. Knowing what car insurance brokers do can help find the best car insurance in North Carolina at the best rates.

Rules of the Road in North Carolina

North Carolina Department of Transportation provides an online overview of the rules of the road. You can also read about all of North Carolina’s traffic laws in the Motor.

North Carolina residents typically fall into three coverage markets: the preferred, the standard, and the non-standard market.

The preferred market has the lowest rates in North Carolina because its members have a clean driving record. They may also have a good credit score, live in relatively safe areas, and have other markers of low risk.

Those in the standard market still have some of the best rates in North Carolina because they have fair driving records, though their rates may not be as low as the preferred market rates. Again, many factors go into insurance and determining who is eligible for the lowest rates.

Those in the non-standard market pay significantly more than the average cost of coverage in North Carolina because they have less experience and/or driving records with multiple infractions, including traffic tickets, accidents, and drunken driving offenses.

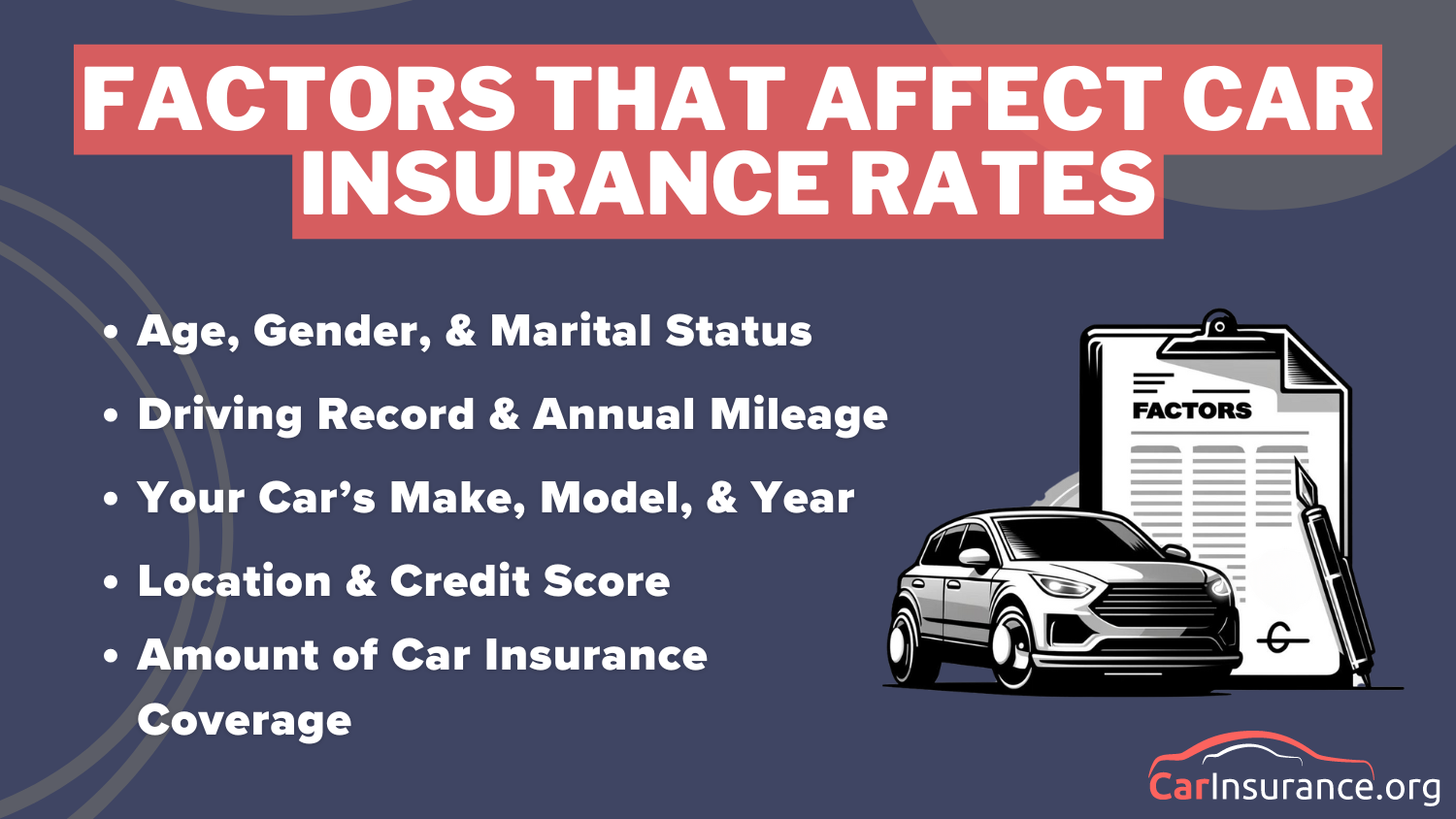

Factors Influencing Car Insurance Rates in North Carolina

Age, gender, marital status, vehicle type, and location influence North Carolina auto insurance rates. Younger drivers, high-risk vehicles, or those with poor driving records typically pay more, while married individuals and safe drivers may receive lower rates from auto insurance companies in North Carolina.

Other factors that affect car insurance include credit history, vehicle use, and claims history. Drivers with good records and lower-risk vehicles can access better rates, while those in high-risk areas or with a history of accidents may face higher premiums.

Car Insurance Rates in North Carolina by Age, Gender & Coverage Level

North Carolina auto insurance rates vary based on age, gender, and coverage level. Young drivers, especially males, tend to face higher premiums, while rates decrease as drivers age. For those seeking the best car insurance in North Carolina, shopping around can help find the cheapest car insurance companies offering competitive rates based on individual needs.

Car Insurance Monthly Rates in North Carolina by Age, Gender & Coverage Level

For example, a 25-year-old female may pay significantly less for full coverage than an 18-year-old male. As drivers age, the cost of coverage generally lowers, making it easier to find affordable options while maintaining the right protection for your needs.

Best Car Insurance Rates in North Carolina by Car’s Make and Year

Your vehicle’s make, model, and year significantly affect the cost of auto insurance in NC. For example, luxury cars like the 2020 BMW X5 or the 2020 Cadillac Escalade tend to have higher monthly premiums than more affordable vehicles like the 2021 Chevrolet Equinox or the 2019 Ford F-150.

Make & Model

Monthly Rates

2021 Audi A4

$180

2020 BMW 3 Series

$200

2020 BMW X5

$200

2020 Cadillac Escalade

$220

2020 Chevrolet Silverado

$150

2021 Chevrolet Equinox

$135

2021 Chrysler Pacifica

$155

2019 Ford F-150

$140

2020 Ford Mustang

$180

2021 GMC Sierra 1500

$155

2020 Honda Civic

$120

2021 Honda CR-V

$130

2020 Hyundai Elantra

$115

2020 Jeep Wrangler

$160

2022 Kia Sorento

$140

2021 Lexus RX 350

$190

2020 Mazda CX-5

$145

2021 Mercedes-Benz C-Class

$210

2021 Nissan Altima

$125

2021 Porsche Macan

$250

2021 Ram 1500

$150

2021 Subaru Outback

$135

2021 Tesla Model 3

$250

2021 Toyota RAV4

$130

2021 Toyota Camry

$130

2021 Volkswagen Jetta

$125

Best Car Insurance Monthly Rates in North Carolina by Your Car's Make, Vehicle and Year

If you’re looking for the best car insurance in North Carolina, consider how the vehicle you drive affects your premiums, as insurance companies may also be willing to insure a car not under your name. Rates can vary, so comparing options can help you find the best deal.

Cheap Car Insurance Rates in NC by Driving Record and Annual Mileage

Rates can vary greatly when you look for car insurance in your area, and factors like driving record and annual mileage can significantly affect your average cost.

Typically, drivers with a clean record pay lower premiums, but those with a ticket, accident, or DUI may have to pay a higher price. Also, the miles driven annually can affect insurance rates, with higher mileage generally leading to increased costs.

Cheap Car Insurance Monthly Rates in NC by Driving Record and Annual Mileage

If you’re looking for the best car insurance in North Carolina, be aware that your driving behavior is key in setting your rates. Safe driving habits and low mileage are great ways to save on your premium.

Cheapest Car Insurance Rates in North Carolina by State & Credit Score

How much is car insurance in North Carolina? You may be wondering this question because finding an auto insurance provider across the state can be challenging, and elements like location and credit score can affect coverage prices.

Cheapest Car Insurance Monthly Rates in North Carolina by State & Credit Score

When seeking the best car insurance in North Carolina, it’s important to note that credit scores can heavily affect premiums. For motorists looking for high-risk auto insurance in NC, you must compare car insurance rates by state and check with your local agent or broker to see which providers offer the cheapest auto insurance in North Carolina.

Searching the Best Car Insurance in North Carolina: Tips for Affordable Coverage

Knowing the difference between agents and brokers is important when looking for car insurance quotes in NC. Agents work for insurance companies and earn commissions, while brokers represent clients and help find the best car insurance in North Carolina that meets their needs. Both can help lower your car insurance cost by finding competitive rates.

Before purchasing insurance, ensure that the Department of Insurance licenses the company, agent, or broker. You can verify their credentials and check complaint reports to ensure you’re working with a reputable professional who can help you find the best North Carolina auto insurance company for affordable coverage and price options.

What to do After an Accident in NC

If you’re in an accident in North Carolina, stop immediately, check for injuries, call the police, and exchange information with the other driver, even if they don’t have insurance. If you fail to do so can lead to legal trouble. You should also report the accident to your insurance company as soon as possible to start the claims process.

You can contact the Department of Insurance for help if your claim is delayed or denied unfairly. Car insurance companies in North Carolina may recover costs from the at-fault driver’s insurer. Also, remember that you need insurance to buy a car in North Carolina before driving it legally.

If you’re a high-risk driver and your driving record is full of infractions, such as accidents, tickets, or drunken driving offenses. In that case, you may have difficulty finding the best car insurance in North Carolina to sell you a policy. If you need help choosing the right coverage for your needs, you can start by comparing auto insurance quotes in North Carolina to get the best car insurance.

However, because drivers in North Carolina are required to have insurance, the North Carolina Reinsurance Facility was created in 1973 to help drivers who have been unsuccessful in purchasing coverage due to their less-than-clean driving records.

When choosing an insurer, look beyond price. Geico’s strong customer service and hassle-free claims process make it a top choice for drivers in NC.

Schimri Yoyo

Licensed Agent and Financial Advisor

Suppose you violate certain traffic laws, such as driving while uninsured, driving under the influence, causing an accident while driving while uninsured, or having too many traffic tickets within a short time span, resulting in your license being suspended or revoked.

In that case, you may have to show proof of financial responsibility in the form of SR-22 insurance, or they may request your insurance card to determine your policy number in order to get your license back. If this applies to you, ask your insurer if they provide SR-22 because not all insurers do.

Ready to shop around for the best car insurance company? Enter your ZIP code and see which one offers the coverage you need.

Frequently Asked Questions

Who is the best car insurance company in NC?

The best car insurance companies in NC vary based on your needs, but top picks often include Geico, State Farm, and Progressive, known for offering competitive rates and good customer service.

What is considered full coverage in NC?

Full coverage in North Carolina typically includes liability coverage, comprehensive coverage, and collision coverage. It can also include uninsured/underinsured motorist coverage and medical payments (depending on your policy). Know what type of coverage is best for you by entering your ZIP code into our free comparison tool.

What is the average cost of car insurance in North Carolina?

Depending on personal circumstances, the average cost of car insurance in North Carolina varies but is typically around $83 to $100 per month for full coverage and around $42 to $50 for minimum coverage.

What is the new law for car insurance in NC?

The most recent update in North Carolina’s car insurance laws includes allowing drivers to purchase uninsured motorist coverage in higher limits, though you can still opt for the state minimum.

What is North Carolina state insurance called?

North Carolina state insurance generally refers to the minimum car insurance requirements set by the state, which include liability and uninsured motorist coverage.

Is Allstate licensed in North Carolina?

Yes, Allstate is licensed to sell car insurance in North Carolina and is an active provider in the state. Type in your ZIP code and see which car insurance provider is the best option for you.

What car insurance is required in North Carolina?

In the state of North Carolina, carrying minimum car insurance coverage is not bad. Still, the law requires that all drivers have 30/60/35 liability insurance and uninsured motorist insurance with minimum coverage limits.

Why are cars cheaper in North Carolina?

Car prices may be lower in North Carolina due to lower vehicle taxes, fewer urban areas with high demand, and lower living costs than other regions. Compare rates and get quick car insurance quotes from top companies by entering your ZIP code.

Did NC insurance rates go up?

Yes, car insurance rates in North Carolina, like many other states, have increased in recent years, driven by factors like higher repair costs, accidents, and natural disasters.

Why is NC car insurance so expensive?

NC car insurance rates can be expensive due to factors such as population density, weather events like hurricanes, a high number of uninsured drivers, and the cost of car repairs.

19,116 reviews

19,116 reviews