Best Car Insurance in Massachusetts for 2026 [Top 10 MA Companies]

The best car insurance in Massachusetts comes from Nationwide, Liberty Mutual, and State Farm, with rates starting at $49 per month. Nationwide offers up to 25% off for bundling in MA, Liberty Mutual provides discounts to safe MA drivers, and State Farm offers flexible, tailored coverage for MA residents.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Content Team Lead

Tonya Sisler has been a technical insurance writer for over five years. She uses her extensive insurance and finance knowledge to write informative articles that answer readers' top questions. Her mission is to provide readers with timely, accurate information that allows them to determine their insurance needs and choose the best coverage. Tonya currently leads a team of 10 insurance copywri...

Tonya Sisler

Licensed Insurance Agent

Chris is the founder of Abrams Insurance Solutions and Marcan Insurance, which provide personal financial analysis and planning services for families and small businesses across the U.S. His companies represent nearly 100 of the top-rated insurance companies. Chris has been a licensed insurance agent since 2009 and has active insurance licenses in all 50 U.S. states and D.C. Chris works tireles...

Chris Abrams

Updated June 2025

3,071 reviews

3,071 reviewsCompany Facts

Full Coverage in MA

A.M. Best Rating

Complaint Level

Pros & Cons

3,071 reviews 3,792 reviews

3,792 reviewsCompany Facts

Full Coverage in MA

A.M. Best Rating

Complaint Level

Pros & Cons

3,792 reviews18,157 reviewsCompany Facts

Full Coverage in MA

A.M. Best Rating

Complaint Level

Pros & Cons

18,157 reviewsFinding the best car insurance in Massachusetts means comparing top providers like Nationwide, Liberty Mutual, and State Farm, which offer rates starting at $49 monthly.

Nationwide stands out for its digital tools, efficient handling of car accidents & claims, and bundling discounts.

Our Top 10 Company Picks: Best Car Insurance in Massachusetts

| Company | Rank | Claims Satisfaction | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 728 / 1,000 | A+ | Usage-Based Discounts | Nationwide | |

| #2 | 717 / 1,000 | A | Comprehensive Coverage | Liberty Mutual | |

| #3 | 710 / 1,000 | A++ | Trusted Brand | State Farm | |

| #4 | 706 / 1,000 | A | AARP Benefits | Farmers | |

| #5 | 701 / 1,000 | A+ | Strong Reputation | The Hartford |

| #6 | 692 / 1,000 | A | Customer Satisfaction | American Family | |

| #7 | 692 / 1,000 | A++ | Online Tools | Geico | |

| #8 | 691 / 1,000 | A+ | Accident Forgiveness | Allstate |

| #9 | 684 / 1,000 | A++ | Safe Drivers | Travelers | |

| #10 | 672 / 1,000 | A+ | Discount Variety | Progressive |

Liberty Mutual delivers solid value through its reliable network of local agents and a range of safe driver discounts, making it a strong choice for personalized service and cost savings.

State Farm offers flexible coverage and innovative tools to help drivers compare policies, customize protection, and find options that match their budget and lifestyle.

- Affordable options exist for the best car insurance in Massachusetts

- Top insurers provide strong claim support and local customer care

- Nationwide offers great value with low rates and flexible coverage options

Stop overpaying and find the best car insurance in Massachusetts. Use our free quote comparison tool to view rates from top local providers by entering your ZIP code.

#1 – Nationwide: Overall Top Pick

Pros

- Behavior-Based Savings: MA drivers with safe habits, like minimal hard braking or late-night trips, can save up to 40% with SmartRide. Learn more in our Nationwide review.

- Real-Time Driving Feedback: Massachusetts drivers receive actionable driving insights to improve behavior and unlock more discounts.

- Strong Claims Service: Despite the tech-focus, Nationwide does own an A+ claims standing, invaluable in injury-prone metro areas like Boston.

Cons

- Discounts May Vary by ZIP Code: Massachusetts rate reductions can differ significantly depending on location and local risk factors.

- Privacy Concerns: Some Massachusetts users may hesitate to enroll due to GPS tracking and trip monitoring.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#2 – Liberty Mutual: Comprehensive Coverage

Pros

- Wide Range of Add-Ons: MA drivers can choose from extras like new car replacement, better car replacement, and accident forgiveness. See our Liberty Mutual review for more.

- Strong Presence in MA: Liberty Mutual is headquartered in Boston, giving it a home-field advantage and familiarity with Massachusetts insurance regulations.

- Roadside Assistance Included: For those dealing with winter weather in MA, Liberty Mutual offers peace of mind with its roadside services.

Cons

- Above-Average Premiums: Comprehensive and full coverage rates in Massachusetts tend to be higher than competitors like Geico or USAA.

- Mixed Customer Service Reviews: Some MA drivers report inconsistent experiences with claims support and billing.

#3 – State Farm: Best for Trusted Brand

Pros

- Strong Agent Network in MA: With over 140 agents in Massachusetts, State Farm offers convenient, in-person support for those who value local service.

- Personalized Support: Among the best car insurance in Massachusetts for service, State Farm offers 24/7 claims help and local agent support. Read our State Farm review for more.

- Trusted Coverage: Known for financial strength, State Farm backs the best car insurance in Massachusetts with fast claims payouts and steady rates.

Cons

- Premiums Vary for High-Risk Drivers: While part of the best car insurance in Massachusetts, State Farm may charge higher rates for drivers with accidents or violations.

- Limited Online Quoting Tools: Compared to Geico or Progressive, State Farm’s quote system is less interactive, which may frustrate digital-first consumers in MA.

#4 – Farmers: Best for Policy Customization

Pros

- Exclusive AARP Discounts for Seniors in MA: Farmers offers AARP member-exclusive savings, ideal for Massachusetts’ aging population, over 17% are 65 or older.

- OEM Parts: Farmers will pay for original equipment manufacturer parts, which makes it a strong option if you want higher-quality repairs in Massachusetts.

- Signal Discount: Farmers’ Signal app gives up to 30% off, supporting its spot as the best car insurance in Massachusetts for safe drivers. Read our Farmers review for more.

Cons

- Higher Premiums: Farmers offers strong features, but costs more than some best car insurance options in Massachusetts.

- Limited Discounts: Farmers lacks certain national discounts, reducing its value as the best car insurance in Massachusetts for savings.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#5 – The Hartford: Best for Strong Reputation

Pros

- Highly Rated Claims Service: The Hartford scores above average in claims satisfaction, delivering fast, fair service for Massachusetts drivers, especially in busy areas like Boston.

- Disappearing Deductible Program: The Hartford’s vanishing deductible rewards safe driving—a perk in MA, where claims average $5.2K. Learn more in our The Hartford review.

- Strong Financial Standing: The Hartford has an A+ A.M. Best rating, which translates into strong financial stability, an important factor in MA highly regulated insurance market.

Cons

- Limited Telematics Savings: In Massachusetts, The Hartford only offers limited telematics discounts, which minimizes savings for tech-savvy safe drivers.

- Fewer Local Offices: Limited physical office presence in Massachusetts, which can be a drawback for those preferring face-to-face customer service or agent interactions.

#6 – American Family: Best for Customer Satisfaction

Pros

- Strong Focus on Community and Local Agents: American Family has local agents in eastern and central Massachusetts offering personalized service.

- Extensive Discount Options: The best car insurance in Massachusetts features savings for bundling, good students, low-mileage drivers, and KnowYourDrive telematics.

- Strong Customer Support: The best car insurance in Massachusetts is backed by dedicated agents and 24/7 claims reporting. Explore our American Family review.

Cons

- Limited Availability: The best car insurance in Massachusetts may be harder to access due to fewer agents and limited presence in the region.

- Eligibility Restrictions: The best car insurance in Massachusetts from American Family may not be available to all drivers, depending on location and driving profile.

#7 – Geico: Best for Online Tools

Pros

- User-Friendly Mobile App: Geico’s app scores 4.8/5 on the App Store and allows Massachusetts drivers to manage policies, file claims, and access digital ID cards instantly.

- Excellent Discounts: Massachusetts drivers benefit from discounts of up to 25%, including multi-policy, good driver, and military savings.

- Superb Digital Experience: Geico’s app and website make policy management, claims, and roadside assistance accessible. See more in our Geico car insurance review.

Cons

- Constrained Service Agents: Geico operates online, providing fewer in-person service options than agent-driven providers in Maryland.

- Higher Premiums for High-Risk Drivers: Drivers with accidents, violations, or poor credit may find Geico’s rates less competitive.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#8 – Allstate: Best for Accident Forgiveness

Pros

- Accident Forgiveness Available in MA: Allstate’s accident forgiveness in Massachusetts helps drivers avoid premium increases after their first at-fault accident.

- Exceptional Local Agents: Massachusetts customers receive local agents who give personalized assistance and help with claims. Discover details in our Allstate review.

- Competitive Discounts: Allstate gives up to 25% discounts for safe driving, bundling policies, and the Drivewise program.

Cons

- Only Works Once: The forgiveness only applies to one accident per policy, and repeat offenses will still impact rates.

- Varied Customer Service Reviews: Some customers report delays in claims and billing issues.

#9 – Travelers: Best for Safe Drivers

Pros

- Premier Responsible Driver Plan: Provides accident forgiveness and a decreasing deductible for each claim-free year, great for safe drivers in MA.

- Bundling Potential: Massachusetts homeowners and renters benefit from bundling policies (auto + home), often saving up to 13% on combined premiums.

- Reliable Claims Service: Travelers delivers the best car insurance in Massachusetts with solid financial strength and fast claims. Explore our Travelers review for the complete list.

Cons

- Mixed IntelliDrive Reviews: Some MA drivers report unexpected rate increases if telematics detect late-night driving or harsh braking, even without accidents.

- Less Aggressive Discounts: While they reward safe driving, Travelers offers fewer specialized discounts for occupations or academic achievement than some competitors.

#10 – Progressive: Best for Discount Variety

Pros

- Snapshot Program Offers: Progressive’s telematics-based program can provide up to 30% off for MA drivers with safe behavior, including smooth braking and low mileage.

- Digital Convenience: Progressive, one of the best car insurance options in Massachusetts, allows easy policy and claim management via app or website.

- Broad Discount Options: Progressive offers bundling, paid-in-full, and continuous coverage discounts in Massachusetts. Read our review of Progressive for full details.

Cons

- Price Fluctuations Post-Term: Some Massachusetts policyholders report higher renewal rates even with clean records, especially after the first year.

- Fewer In-Person Agents: Progressive has limited local agents, which may not suit those who prefer in-person service.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Car Insurance Rates and Coverage in Massachusetts

Massachusetts car insurance rates vary significantly by provider and coverage level. For minimum coverage, Geico offers the lowest monthly rate at $40, followed by State Farm at $43 and Travelers at $49. For full coverage, Geico remains the most affordable at $103, while Liberty Mutual is the most expensive at $222.

Massachusetts Car Insurance Monthly Rates by Coverage Level

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

|

| $80 | $205 |

| $55 | $142 | |

| $67 | $171 | |

| $40 | $103 | |

| $86 | $222 | |

| $57 | $146 | |

| $53 | $136 | |

| $43 | $111 | |

| $61 | $161 |

| $49 | $126 |

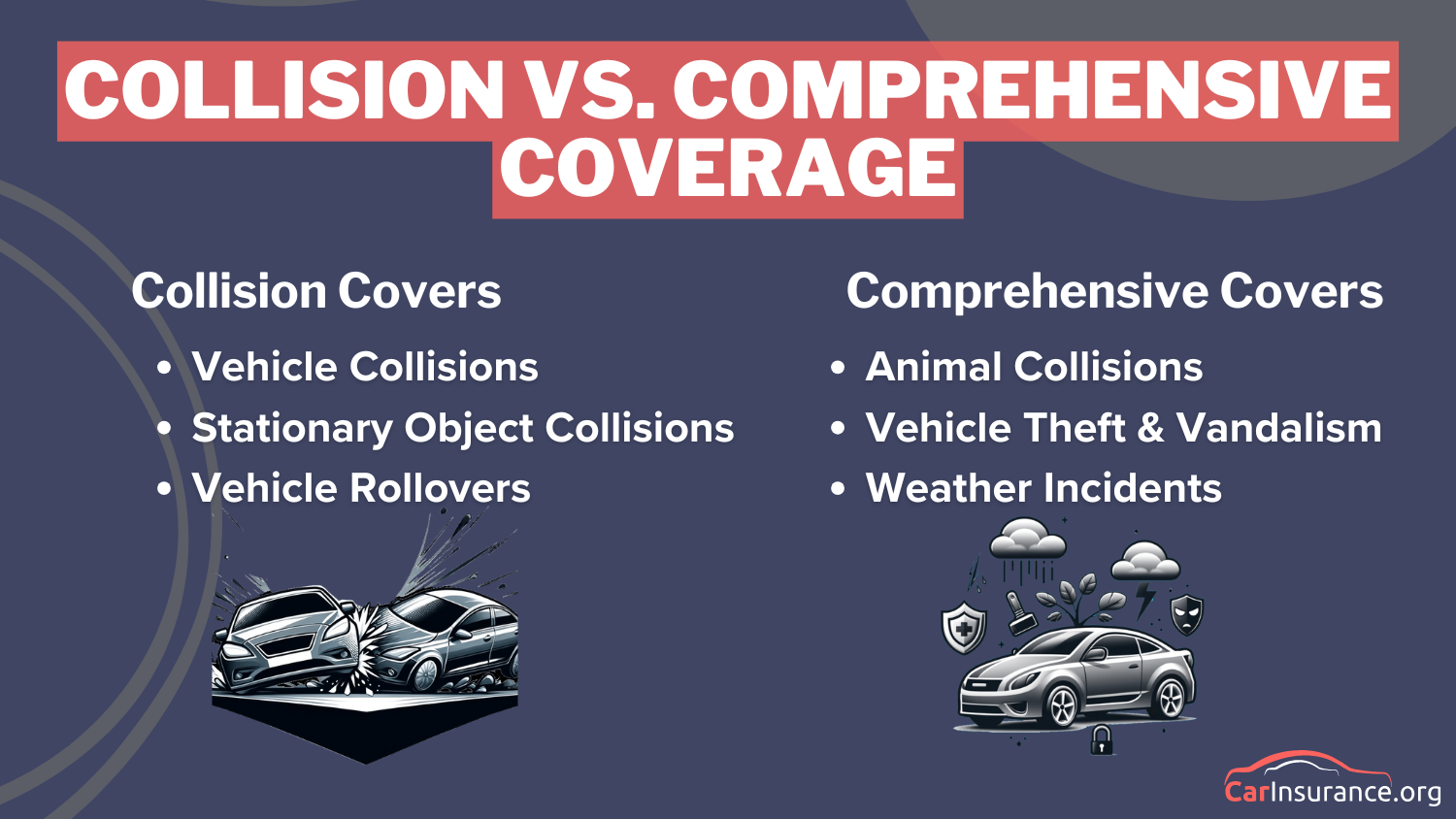

These differences highlight the importance of comparing quotes to find the best value based on your coverage needs. Collision and comprehensive coverage factors affect your car insurance rates. Collision is for accidents, and comprehensive is for theft, weather, and vandalism.

Massachusetts Car Insurance Monthly Rates by Provider & Coverage Type

| Insurance Company | Collision Coverage | Comprehensive Coverage |

|---|---|---|

| $105 | $35 | |

| $100 | $33 | |

| $98 | $31 |

| $85 | $30 | |

| $110 | $38 | |

| $95 | $34 | |

| $90 | $33 |

| $100 | $32 | |

| $108 | $36 | |

| $85 | $28 |

In Massachusetts, collision and comprehensive car insurance rates differ by company. USAA and Geico are the most affordable, with rates as low as $85 for collision and $28–$30 for comprehensive. In contrast, Liberty Mutual is the priciest at $110 and $38.

Collision coverage raises premiums by covering your car after a crash. For example, dropping it on an older vehicle can significantly lower your rate.Brad Larson Licensed Insurance Agent

Most other insurers, like State Farm and Progressive, fall in the mid-range, offering balanced options for different budgets.

Massachusetts Car Insurance Monthly Rates by Driving Record

| Insurance Company | Clean Record | One Accident | One DUI | One Ticket |

|---|---|---|---|---|

|

| $80 | $113 | $134 | $384 |

| $55 | $83 | $91 | $164 | |

| $67 | $96 | $93 | $294 | |

| $40 | $67 | $108 | $127 | |

| $86 | $117 | $156 | $392 | |

| $57 | $80 | $118 | $207 | |

| $53 | $94 | $70 | $141 | |

| $43 | $51 | $56 | $208 | |

| $61 | $89 | $93 | $74 |

| $49 | $68 | $103 | $230 |

Massachusetts car insurance rates rise sharply with driving violations. Geico and State Farm offer the lowest rates for clean records at $40 and $43. After a DUI, Progressive remains affordable at $70, while others like Liberty Mutual and Allstate exceed $130. State Farm offers consistently low rates across all driving records.

Car insurance rates in Massachusetts are highest for teens, with 16-year-old males paying around $309/month and females $271/month.

Rates drop by age 25 to about $70 for females and $65 for males, then stabilize, with 60-year-olds paying the lowest, around $51–$53/month. Younger males consistently face the highest premiums.

Auto Insurance Coverage Options in Massachusetts

When you buy car insurance, it’s important to understand what each option covers and how it applies to your situation. That kind of insight makes it easier to choose coverage that matches the way you drive, your car, and what you’re comfortable spending.

It also gives you a clearer view of the different variables that influence the cost of your policy, such as the level of coverage you choose and your driving record.

- Liability Coverage: Coverage for injuries or damage you cause to others in an accident.

- Personal Injury Protection (PIP): Whether or not you’re at fault, this helps cover your medical bills and lost income.

- Uninsured/Underinsured Motorist Coverage: Compensates you if you’re hit by a driver who doesn’t have insurance or whose coverage isn’t enough to pay for the damages.

- Collision Coverage: Pays for damage to your vehicle if you’re in a crash, regardless of who caused the accident.

- Comprehensive Coverage: Covers non-collision incidents such as theft, fire, vandalism, or weather damage.

It’s about more than just following legal requirements—it’s about making sure you’re financially protected when real-life situations happen. Additional coverages like collision and comprehensive may be especially valuable if you drive a newer car or rely on your vehicle daily.

Customizing your insurance to fit your lifestyle helps you avoid coverage gaps that could lead to costly out-of-pocket expenses. Be sure to explore the types of car insurance coverage archives to help guide your decision and choose what works best for you.

Massachusetts Minimum Car Insurance Requirements

Massachusetts requires drivers to maintain a minimum level of car insurance to ensure they have basic financial protection in case of an accident. That includes bodily injury liability coverage of at least $20,000 per individual and $40,000 per accident, which helps pay for injuries you may cause to others in a crash.

The state also requires $8,000 in personal injury protection (PIP), $20,000/$40,000 in uninsured motorist coverage, and $5,000 for property damage liability. While these limits meet legal requirements, they may not be enough to fully cover the costs of a serious accident.

Medical and repair costs can add up quickly, leading many drivers to increase coverage or add collision and comprehensive insurance. Cutting costs on car insurance in Massachusetts means more than finding the lowest premium—it involves understanding the factors that affect the price of car insurance and knowing which discounts to use.

Insurers offer savings for bundling, safe driving, and good grades. The list below shows discount options from each provider.

Auto Insurance Discounts From Top Massachusetts Providers

| Company | Anti-Theft | Bundling | Good Driver | Good Student | Safe Driver |

|---|---|---|---|---|---|

| 10% | 25% | 25% | 25% | 18% | |

| 25% | 25% | 25% | 20% | 18% | |

|

| 10% | 20% | 30% | 15% | 20% |

| 25% | 25% | 26% | 15% | 15% | |

| 35% | 25% | 20% | 12% | 20% | |

| 5% | 20% | 40% | 18% | 7% | |

| 25% | 10% | 30% | 10% | 12% | |

| 15% | 17% | 25% | 35% | 20% | |

| 15% | 13% | 10% | 8% | 17% | |

| 15% | 10% | 15% | 30% | 10% |

Car insurance discounts can mean big savings when used wisely. Whether you’re a safe driver, a student, or someone who combines policies within your household, these offers can significantly reduce your monthly payments.

Take the time to compare what each company provides so you can choose the insurer that best fits your needs and helps you unlock the greatest possible savings.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Top Auto Insurance Claims and Accident Hotspots in Massachusetts

In Massachusetts, auto insurance claims most often arise from everyday driving hazards like rear-end and side-impact collisions, which tend to result in high repair costs, as well as single-vehicle mishaps and frequent incidents involving parked cars.

5 Most Common Auto Insurance Claims in Massachusetts

| Claim Type | Portion of Claims | Cost per Claim |

|---|---|---|

| Rear-End Collision | 29% | $10,000 |

| Single Vehicle Accident | 19% | $12,000 |

| Parked Car Damage | 14% | $3,000 |

| Side-Impact Collision | 13% | $11,500 |

| Theft Claim | 5% | $8,000 |

While theft is less common, it still contributes noticeably to overall claim expenses. These statistics correspond with accident and claim volumes across large cities—Boston comes out on top with 4,498 accidents and 2,024 claims each year, while Worcester, Springfield, Cambridge, and Lowell give a good list of high-risk regions.

Massachusetts Accidents & Claims per Year by City

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Boston | 4,498 | 2,024 |

| Cambridge | 1,500 | 675 |

| Lowell | 1,200 | 540 |

| Springfield | 2,800 | 1,260 |

| Worcester | 3,200 | 1,440 |

This accident guide highlights the high rate of collision-related accidents in densely populated Massachusetts cities.

It also emphasizes how safe driving, secure parking, and staying informed about local accident trends can help reduce both accident risk and insurance costs.

Massachusetts Auto Insurance Risk Grades

If you’ve ever asked how much insurance do I need for my car? the answer in Massachusetts depends on factors like theft rates, winter weather, and traffic in cities like Boston.

Massachusetts Auto Insurance Premiums

| Category | Grade | Explanation |

|---|---|---|

| Uninsured Drivers Rate | A | Strict laws keep the uninsured driver rate relatively low |

| Vehicle Theft Rate | A- | Lower-than-average theft rates across most cities |

| Average Claim Size | B | Moderate – healthcare and repair costs are manageable |

| Weather-Related Risk | B | Winters increase claims due to snow/ice, but not extreme overall |

| Traffic Density | B- | Congestion in urban areas like Boston raises collision risk |

This guide shows how each factor impacts costs, helping you understand what drives rates and which risks to consider. Massachusetts ranks well in key insurance factors, keeping premiums stable.

Paying your premium annually instead of monthly can save up to 10% with many Massachusetts insurers.Tonya Sisler Content Team Lead

Strict penalties for uninsured driving and low theft rates help offset traffic and harsh winters, resulting in generally affordable auto insurance.

Car Insurance Picks for Massachusetts Drivers

Finding the best car insurance in Massachusetts depends on your location, driving history, and coverage level, with some providers offering rates as low as $49 per month. Whether you’re comparing rates by town or checking reviews, top picks like Nationwide, Liberty Mutual, and State Farm consistently lead for Massachusetts car insurance.

For new drivers, especially, identifying the best car insurance in MA for new drivers starts with comparing quotes and understanding different types of car insurance coverage. With the right insights, it’s easier to choose the right protection without overpaying.

So go ahead let’s find the best car insurance company in MA. Enter your ZIP code to find out which one has the coverage you want.

Frequently Asked Questions

Who is the best car insurance company in Massachusetts?

Nationwide is ranked the best overall. It offers affordable full coverage at $146 a month, a generous 25% bundling discount, and holds an A++ financial strength rating, making it ideal for budget-conscious drivers.

What safe driving discounts are available in Massachusetts car insurance?

For safe drivers, the best solution is Progressive, which provides Snapshot discounts. Geico and State Farm offer good-driving discounts, too. Enter your ZIP code to get the best car insurance quotes from leading insurers.

Which Massachusetts car insurance companies have the best claims service?

One area where Nationwide excels is filing a car insurance claim after an accident. Both its claims and customer service are well-regarded. Its A+ rating and customer-forward approach make it a solid option for support.

How does Massachusetts car insurance support drivers after minor violations?

Geico and USAA are the least expensive for drivers with minor infractions. Their rates for full coverage, as low as $72 a month and $53 a month respectively, could significantly mitigate the sting of a ticket.

Which insurers in Massachusetts offer accident forgiveness?

Allstate is well-known for offering accident forgiveness, which can help you avoid a rate increase after your first at-fault accident. It’s a valuable feature for peace of mind.

What telematics or safe-driving programs lower rates in Massachusetts?

Programs such as Snapshot from Progressive and Drive Safe & Save from State Farm monitor the way you drive. They can reward safe habits, but they also record things you do that can raise your premiums.

Are usage-based car insurance plans available in Massachusetts?

Yes. Providers such as Progressive, Allstate, and State Farm offer usage-based plans that adjust your rate based on how much and how safely you drive.

Do Massachusetts insurers reward claims-free drivers with discounts?

Geico, USAA and Nationwide regularly reduce premiums for claims-free drivers with loyalty or renewal discounts that can minimize long-term insurance costs.

How can drivers in Massachusetts save after a traffic ticket?

Opting for insurers such as Geico at $72 monthly or State Farm at $78 monthly can also limit premium hikes following a ticket. Frequently, such companies are lenient with small offenses that relate to citation vs. ticket.

Who offers quick claims processing for car insurance in Massachusetts?

Nationwide stands out for efficient claims service, backed by a strong A+ rating. USAA also excels in this area, offering fast claims response for military families and eligible members.

What driving courses qualify for insurance discounts in Massachusetts?

Which companies offer vanishing deductibles in Massachusetts?

Are there student discounts for Massachusetts car insurance?

Can bundling policies lower car insurance costs in Massachusetts?

What is a claims satisfaction guarantee in Massachusetts car insurance?

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.