Best Car Insurance in Wisconsin for 2026 [Check Out the Top 10 Companies]

Geico, Progressive, and State Farm provide the best car insurance in Wisconsin, with rates starting at $16 a month. State Farm is the cheapest car insurance option in Wisconsin. Progressive customizes coverage with bundling discounts, while Geico excels in customer service and local agent support.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Insurance Feature Writer

Rachel Bodine graduated from college with a BA in English. She has since worked as a Feature Writer in the insurance industry and gained a deep knowledge of state and countrywide insurance laws and rates. Her research and writing focus on helping readers understand their insurance coverage and how to find savings. Her expert advice on insurance has been featured on sites like PhotoEnforced, All...

Rachel Bodine

Licensed Insurance Agent

Eric Stauffer is an insurance agent and banker-turned-consumer advocate. His priority is educating individuals and families about the different types of insurance coverage. He is passionate about helping consumers find the best coverage for their budgets and personal needs. Eric is the CEO of C Street Media, a full-service marketing firm and the co-founder of ProperCents.com, a financial educat...

Eric Stauffer

Updated April 2025

13,285 reviewsCompany Facts

Full Coverage in Wisconsin

A.M. Best Rating

Complaint Level

Pros & Cons

13,285 reviews 18,157 reviews

18,157 reviewsCompany Facts

Full Coverage in Wisconsin

A.M. Best Rating

Complaint Level

Pros & Cons

18,157 reviewsGeico, Progressive, and State Farm offer the best car insurance in Wisconsin, with a starting rate of $16 per month. Each insurer is known for offering low rates, solid coverage features, and great customer support.

Geico is the best choice, offering only $23 per month. Check the details below to save big and select the best coverage for your needs.

Our Top 10 Company Picks: Best Car Insurance in Wisconsin

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 25% | A++ | Affordable Coverage | Geico | |

| #2 | 10% | A+ | Customizable Options | Progressive |

| #3 | 17% | B | Customer Service | State Farm | |

| #4 | 25% | A | Personalized Service | American Family | |

| #5 | 25% | A+ | Local Agents | Allstate | |

| #6 | 10% | A++ | Military Families | USAA | |

| #7 | 20% | A+ | Comprehensive Coverage | Nationwide | |

| #8 | 20% | A | Policy Bundling | Farmers |

| #9 | 25% | A | Custom Plans | Liberty Mutual | |

| #10 | 13% | A++ | Electric Vehicles | Travelers |

This guide will explain what the best car insurance companies in Wisconsin are famous for and how to find safe, budget-friendly car insurance for your needs.

- Geico provides affordable coverage and excellent service in Wisconsin

- Progressive offers customizable coverage to meet diverse needs

- State Farm excels in customer service with local agent support

Geico leads with top-rated service, while Progressive and State Farm meet Wisconsin drivers’ needs with flexible, reliable coverage options. Shop for the best liability-only car insurance with our free quote comparison tool. Enter your ZIP code to begin.

#1 – Geico: Top Overall Pick

Pros

- Low Rates: Geico offers some of the lowest-cost car insurance in Wisconsin, starting at $23 per month.

- Several Discounts: Bundling, safe driving, and military service discounts save customers money.

- Excellent Financial Strength: Geico is rated A++ by A.M. Best, according to Geico car insurance reviews.

Cons

- Limited Local Agents: Geico is based on online and phone assistance, which might not be for those who prefer face-to-face interaction.

- Increased Premiums for Hazardous Drivers: Accident or DUI drivers can expect high rate hikes, and some have reported problems with Geico customer service.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#2 – Progressive: Best for Customizable Options

Pros

- Personalized Coverage Options: Progressive enables drivers to customize their policies, which is why it’s one of the best options for Wisconsin drivers. Read our Progressive car insurance review for more information.

- Bundled Savings Advantage: When policies are bundled together, policyholders can save up to 10% on their premiums.

- Safe Driver Discounts: Progressive’s Snapshot program rewards responsible drivers with discounted rates for maintaining good driving habits.

Cons

- Expensive for Younger Drivers: Teens and new drivers may find other insurers cheaper when seeking Wisconsin car insurance quotes.

- Unpredictable Claim Handling: Some customers report slow claims handling, annoying those who want an easy process.

#3 – State Farm: Best for Customer Service

Pros

- Highly Rated Help: Our State Farm car insurance review praises its excellent customer service and hassle-free claims process.

- Discounts on Bundles: Save as much as 17% by bundling auto with home or renters insurance.

- Nationwide Coverage: An established insurer with wide-ranging policies and an extensive network of local agents.

Cons

- Premium Pricing: Though service is excellent, premiums can be pricey, particularly for high-risk drivers.

- Strict Policy Conditions: State farm reinstatement policy may have strict conditions requiring strict adherence to reinstatement.

#4 – American Family: Best for Personalized Service

Pros

- Individualized Service With Local Agents: Our American Family car insurance review discusses the individualized service clients can count on.

- Eye-Catching Discounts: American Family provides substantial savings discounts of up to 25% when bundling home and auto policies.

- High Customer Satisfaction: Praised for extraordinary claims handling and customer service, American Family receives top ratings consistently.

Cons

- Higher Rates for Some Drivers: Car insurance premiums could be higher than those of some national competitors.

- Limited State Availability: The presence of American Family Insurance in Hudson, WI, is limited.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#5 – Allstate: Best for Local Agents

Pros

- Extensive Agent Network: Consumers can receive face-to-face assistance from many agents. For example, Allstate has offices in Janesville, WI.

- Safe-Driving Incentives: Drivewise’s program saves policyholders money by rewarding them for safe driving.

- A—Rated for Security: With an A+ rating from A.M. Best, the Allstate car insurance review praises its security for its swift claim payment.

Cons

- Costly for High-Risk Drivers: Drivers with a history of accidents or speeding tickets will pay much higher rates.

- Fewer Discount Choices: Not all discounts are offered in every state, so qualifying is more difficult for some drivers.

#6 – USAA: Best for Military Families

Pros

- Unique Military Benefits: USAA has exclusive discounts and custom coverage selections for military personnel and their families.

- Best-Rated Customer Service: Renowned for outstanding service, USAA car insurance reviews rank the company highest for policyholder satisfaction.

- Cheap Premiums: Members and their families mostly get discounted Wisconsin auto insurance premiums.

Cons

- Membership Limitations: Policies exclusively cover veterans, active military members, and their families.

- No Face-to-Face Support: Unlike physical branches, online insurers usually have all inquiries and claims addressed remotely via computer services or call centers.

#7 – Nationwide: Best for Comprehensive Coverage

Pros

- Comprehensive Coverage Options: Our Nationwide car insurance review highlights its accident forgiveness and vanishing deductibles programs as key benefits.

- Substantial Multi-Policy Discounts: Policyholders can save up to 20% by bundling auto and home insurance, a common perk among insurance companies in WI.

- Strong Financial Support: With an A+ rating from A.M. Best, the insurer guarantees fair claims settlement.

Cons

- Unreliable Customer Service: Drivers often complain about Nationwide’s claims process, citing issues such as delays in claim resolution.

- More Expensive for Young Drivers: Premiums are more expensive for young, high-risk drivers.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#8 – Farmers: Best for Policy Bundling

Pros

- Customizable Coverage: Provides several add-ons, such as accident forgiveness and new car replacement.

- Bundle & Save: Save 20% by combining auto with home or life policies for extra discounts.

- Strong Local Support: Our Farmers car insurance review emphasizes its dependable agent network for face-to-face support.

Cons

- More Expensive Than Competitors: Premiums are higher than alternatives such as Geico and Progressive.

- Limitations on Discounts: Obtaining cheap car insurance in WI may be more difficult.

#9 – Liberty Mutual: Best for Custom Plans

Pros

- Tailored Coverage Plans: Our Liberty Mutual auto insurance review discusses its adaptive policy designs, such as deductible savings programs that alleviate out-of-pocket expenses.

- Substantial Discounts: Policyholders can save up to 25% by insuring more than one car under a single policy, a cost-effective option for those living with others.

- Rate Increases Protection: The accident forgiveness feature prevents your first at-fault accident from increasing your premium, creating financial security.

Cons

- Higher Premiums: Individuals with previous accidents or low credit scores might find the cost of liability car insurance in Wisconsin more favorable.

- Customer Complaints: Some customers have complained about delayed claim settlement and unexpected rate hikes.

#10– Travelers: Best for Electric Vehicles

Pros

- Special Discounts for Hybrid and Electric Cars: Travelers car insurance provides personalized discounts for hybrid and electric cars, encouraging green coverage.

- Highest Rated Financial Strength: According to our Travelers car insurance review, it boasts an A++ rating from A.M. Best, testifying to its financial stability and reliability in settling claims.

- Attractive Premiums for Safe Drivers: Safe drivers with a spotless record enjoy competitive Wisconsin car insurance rates.

Cons

- Restricted In-Person Agents: Travelers operate primarily online. They offer fewer local agents, which can be a drawback for those who need in-person assistance.

- Increased Premiums for Risky Drivers: Travelers auto insurance can cost more for those involved in accidents or traffic tickets.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Best Wisconsin Car Insurance Coverage and Rates

Car insurance rates in Wisconsin differ by provider and coverage. Comparing providers can help motorists get affordable car insurance in Wisconsin according to their requirements.

Wisconsin Car Insurance Monthly Rates by Provider & Coverage Level

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $43 | $123 | |

| $22 | $63 | |

|

| $38 | $109 |

| $23 | $62 | |

| $30 | $84 | |

| $80 | $226 | |

|

| $33 | $94 |

| $21 | $58 | |

| $26 | $72 | |

| $16 | $47 |

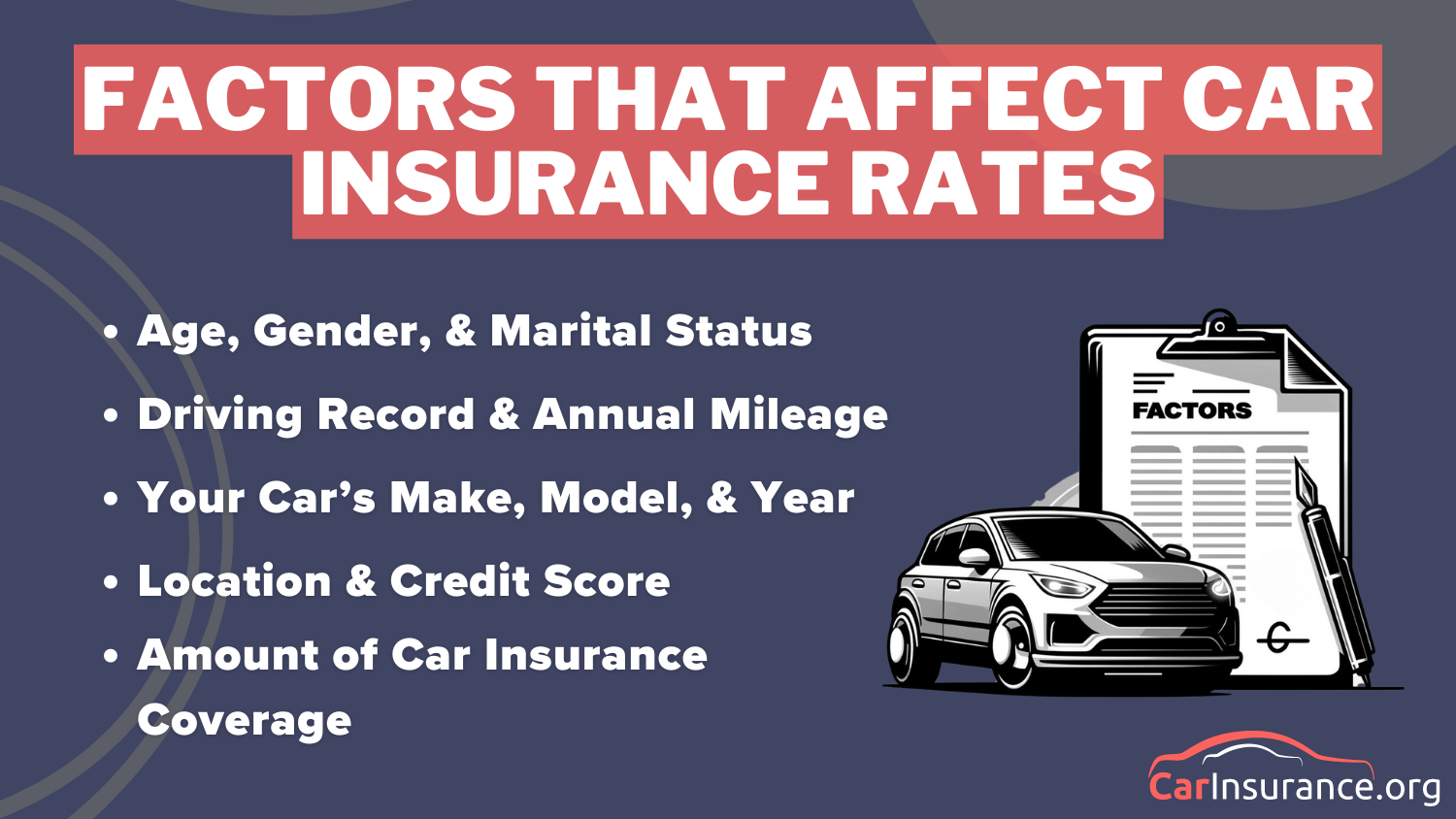

Several factors affect the price of car insurance, including age, driving history, and mileage. Safe drivers with low annual mileage often pay less, while younger or high-risk drivers may see higher premiums due to increased accident risks.

Location, vehicle type, and credit score also determine costs. Luxury vehicles and city locations tend to result in higher rates. Full coverage instead of minimum coverage raises premiums but provides greater financial protection for motorists.

The Best Wisconsin Car Insurance Discounts

Wisconsin motorists can reduce expenses with discounts such as bundling, safe driver incentives, and telematics initiatives. Knowing how to drive safely, no matter the time of day assists in earning accident-free and defensive driving discounts.

Car Insurance Discounts From the Top Providers in Wisconsin

| Insurance Company | Available Discounts |

|---|---|

| Multi-policy, Safe driver, New car, Anti-theft device, Full pay, Good student, Smart student, Early signing, Responsible payer, Drivewise (telematics) | |

| Multi-policy, Low mileage, Safe driver, Good student, Teen driver, Defensive driver, Generational, Loyalty, AutoPay, Early bird, Young volunteer discount | |

|

| Multi-policy, Good student, Safe driver, Bundling, Homeowner, Alternative fuel vehicle, Signal (telematics), Business/professional group, Pay-in-full |

| Multi-vehicle, Anti-theft, Defensive driving, Good student, Federal employee, Military, Emergency deployment, Membership, Seatbelt use, Five-year accident-free | |

| Early shopper, Multi-policy, Military, New car, Good student, Paperless billing, Online purchase, Accident-free, Anti-theft, Hybrid vehicle, Homeowner | |

| Multi-policy, Safe driver, Paperless billing, SmartRide (telematics), Affinity member, Defensive driving, Accident-free, Good student, Family plan, AutoPay | |

|

| Multi-policy, Continuous insurance, Safe driver, Snapshot (telematics), Homeowner, Pay-in-full, Paperless billing, Sign online, Teen driver, Multi-car |

| Multi-policy, Safe driver, Good student, Steer Clear (young drivers), Accident-free, Vehicle safety, Drive Safe & Save (telematics), Defensive driving | |

| Multi-car, Hybrid/electric car, Safe driver, Homeownership, Early quote, Continuous insurance, IntelliDrive (telematics), Good student, New car | |

| Safe driver, Defensive driving, Military-specific discounts, New vehicle, Multi-policy, Loyalty, Storage discount, Family discount, Vehicle storage |

Discounts vary by firm, with State Farm and USAA offering the best accident-free discounts. Bundling lowers costs by up to 22%. Since the average cost of a Wisconsin car insurance policy is relatively high, using several discounts together maximizes the savings.

Car Insurance Discounts From Top Wisconsin Providers

| Insurance Company | Safe Driver | Accident-Free | Bundling | Good Student | Anti-Theft Devices |

|---|---|---|---|---|---|

| 10% | 15% | 20% | 12% | 7% | |

| 12% | 14% | 18% | 10% | 6% | |

|

| 8% | 13% | 22% | 9% | 8% |

| 15% | 12% | 19% | 11% | 5% | |

| 9% | 16% | 21% | 13% | 7% | |

| 11% | 10% | 17% | 8% | 9% | |

|

| 14% | 12% | 16% | 9% | 6% |

| 13% | 17% | 20% | 10% | 8% | |

| 10% | 14% | 18% | 12% | 7% | |

| 15% | 18% | 22% | 14% | 10% |

Motorists can save even more by joining telematics, paying upfront, or with anti-theft devices. Comparing companies and selecting the most suitable discount combination guarantees Wisconsin citizens affordable insurance without compromising protection.

Wisconsin Minimum Car Insurance Coverage Requirements

Wisconsin’s fault system holds the negligent driver liable for damages from an accident. As a matter of state law, drivers must maintain bodily injury liability coverage and property damage coverage. Uninsured drivers face harsh penalties.

Wisconsin state law dictates a minimum of $25,000 in coverage for bodily injury per person, $50,000 per accident, and $10,000 for property damage. These limits pay for medical expenses and repair, but numerous drivers opt for higher limits to have greater peace of mind.

Geico offers Wisconsin drivers reliable minimum coverage at competitive rates, ensuring compliance with state laws.Brad Larson Licensed Insurance Agent

Wisconsin further requires uninsured motorist coverage to protect against uninsured motorists. Shopping for auto insurance quotes in WI enables drivers to obtain affordable rates that satisfy laws while providing ample coverage.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Wisconsin Car Insurance Accident Claims and Premiums

Wisconsin sees frequent car accidents & claims, with larger cities experiencing higher rates. Milwaukee reports 25,000 crashes yearly, while Madison follows with 8,200 accidents.

Wisconsin Accidents & Claims per Year by City

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Appleton | 3,700 | 2,900 |

| Eau Claire | 3,200 | 2,500 |

| Green Bay | 5,600 | 4,300 |

| Janesville | 2,600 | 2,000 |

| Kenosha | 4,800 | 3,600 |

| Madison | 8,200 | 6,400 |

| Milwaukee | 25,000 | 18,500 |

| Oshkosh | 2,900 | 2,200 |

| Racine | 4,200 | 3,200 |

| Waukesha | 3,500 | 2,700 |

Fender benders make up 29% of claims, averaging $2,000 per repair. Rear-end collisions cost around $3,000 per claim, while whiplash injuries, though rarer, average $10,000.

Wisconsin’s insurance premiums depend on factors like theft rates and claim sizes. The state earns an A for low vehicle theft but gets a B for moderate claim amounts.

5 Most Common Car Insurance Claims in Wisconsin

| Claim Type | Portion of Claims | Cost per Claim |

|---|---|---|

| Fender Benders | 29% | $2,000 |

| Rear-End Collisions | 22% | $3,000 |

| Whiplash Injuries | 18% | $10,000 |

| Side-Impact Collisions | 16% | $4,000 |

| Windshield Damage | 15% | $500 |

Weather impacts accident rates, earning Wisconsin a B grade. Snow and icy roads create risks, but uninsured drivers remain a bigger issue, with 13.3% lacking coverage.

Insurance costs vary by city, with Milwaukee and Madison having higher risks. Drivers in smaller cities, like Oshkosh, often pay less due to fewer accidents each year.

Wisconsin Report Card: Car Insurance Premiums

| Category | Grade | Explanation |

|---|---|---|

| Vehicle Theft Rate | A | Low vehicle theft incidents |

| Average Claim Size | B | Moderate claim amounts seen |

| Traffic Density | B | Moderate traffic congestion |

| Weather-Related Risks | B | Moderate weather-related risks |

| Uninsured Drivers Rate | C | 13.3% lack insurance coverage |

To save on the average car insurance in Wisconsin, drivers should practice safe habits and get uninsured motorist coverage to protect against financial losses.

How to Find the Best Car Insurance in Wisconsin in 5 Simple Steps

Buying the right car insurance in Wisconsin can be daunting, with so many choices to make. This step-by-step guide will help you compare insurers and types of coverage and get the most suitable policy for you.

These five steps will allow you to obtain the perfect combination of price and protection.

- Compare Different Quotes: Get quotes from insurers, look for discounts, and check reviews. This helps in securing an affordable policy with high customer satisfaction.

- Check Your Coverage Needs: Consider your needs, car’s value, and driving habits. In case you’re shopping around, compare car insurance for Wisconsin drivers.

- Check Insurer’s Reputation: Look up the company’s reviews, financial health, and complaint records to be sure you’re selecting a good insurance company.

- Examine Policy Terms: Know deductibles, exclusions, and additional coverage. Knowing when to use your deductible avoids surprises and keeps costs in check.

- Finalize Your Policy: Double-check details and payment terms to ensure you have the right coverage. Understanding deductibles will prevent you from spending money unnecessarily.

By going through these five steps, you can make a confident selection of the most suitable car insurance policy in Wisconsin. Spending time comparing carriers and knowing your coverage guarantees that you obtain the maximum coverage at a reasonable rate. Begin comparing today and drive peacefully!

Selecting the Best Car Insurance Provider in Wisconsin

When selecting the best car insurance in Wisconsin, comparing rates is key to determining the right coverage that meets your vehicle needs and budget. Understanding how car insurance works can also help make a wise decision.

Leading auto insurance providers such as Geico, Progressive, and State Farm have affordable policies, personalized plans, and quality customer service, making them the preferred options for Wisconsin drivers. Ready to find cheaper car insurance coverage? Enter your ZIP code to begin.

Frequently Asked Questions

Why Geico, Progressive, and State Farm are the top car insurance providers in Wisconsin?

Geico, Progressive, and State Farm are the top car insurance companies in Wisconsin because they are affordable, offer customizable coverage, and have good customer service. For expanded insights, check out the different types of car insurance coverage.

How does Wisconsin’s at-fault insurance system impact drivers in the event of an accident?

Since Wisconsin is an at-fault state, the driver responsible for an accident must cover damages, which affects the average car insurance cost in Wisconsin.

See how much you’ll pay for car insurance by entering your ZIP code into our free comparison tool.

What are the main benefits of combining auto with other policies?

Bundling policies like auto insurance in Wisconsin with homeowners’ or renters’ insurance can offer significant discounts and lead to cheap full coverage car insurance in Wisconsin.

How do Wisconsin’s minimum car insurance coverage requirements compare to those of other states?

Wisconsin requires lower minimum liability coverage than some states but mandates uninsured motorist coverage, which affects the average cost of car insurance in Wisconsin.

What role do demographics, such as age and gender, play in determining car insurance rates in Wisconsin?

Age impacts Wisconsin auto insurance rates more than gender, with younger drivers paying more and rates stabilizing in middle age.

Why is it important for Wisconsin drivers to have uninsured motorist coverage?

Uninsured motorist coverage protects drivers financially if an uninsured driver hits them.

What are some of the most significant discounts offered by top Wisconsin car insurance providers?

Top Wisconsin car insurance companies offer discounts for bundling different policies, maintaining a clean driving record, and installing vehicle safety features. Explore our Safety car insurance review for more insights.

How does a driver’s ZIP code affect their car insurance rates in Wisconsin?

A driver’s ZIP code affects Wisconsin car insurance quotes due to local accident frequency, crime rates, and population density.

What distinguishes USAA’s car insurance offerings from other providers, particularly for military families?

USAA offers military families some of the cheapest car insurance in Wisconsin through exclusive discounts and specialized coverage. Ready to find affordable car insurance? Use our free comparison tool to get started.

How do usage-based insurance programs help drivers save money on their car insurance premiums?

Usage-based programs help drivers get cheap auto insurance in Wisconsin by tracking their habits and offering discounts for safe driving. Learn how to lower your car insurance costs.

Related Articles

-

Apr 2025

Best Car Insurance in Nevada for 2026 [Check Out the Top 10 Companies]

-

Apr 2025

Best Car Insurance in Nebraska for 2026 [Find the Top 10 Companies Here]

-

Apr 2025

Best Car Insurance in Oregon for 2026 [Review the Top 10 Companies Here]

-

Mar 2025

Best Car Insurance in New Jersey for 2026 [Compare the Top 10 Companies]

-

May 2025

Best Car Insurance in Idaho for 2026 [Find the Top 10 Companies Here]

-

Mar 2025

Best Car Insurance in Alabama in 2026 [Your Guide to the Top 10 Companies]

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.