Should you refinance your car loan? (Expert Advice for 2026)

Should you refinance your car loan? While comparing car refinance options could save you up to $1,000 by lowering your interest rate, consider the drawbacks of refinancing a car loan, such as extended loan terms or additional fees, which might outweigh the benefits.

Read more

Table of Contents

Table of Contents

Expert Insurance Writer

Merriya Valleri is a skilled insurance writer with over a decade of professional writing experience. Merriya has a strong desire to make understanding insurance an easy task while providing readers with accurate and up-to-date information. Merriya has written articles focusing on health, life, and auto insurance. She enjoys working in the insurance field, and is constantly learning in order to ...

Merriya Valleri

Licensed Insurance Agent

Jeff is a well-known speaker and expert in insurance and financial planning. He has spoken at top insurance conferences around the U.S., including the InsuranceNewsNet Super Conference, the 8% Nation Insurance Wealth Conference, and the Digital Life Insurance Agent Mastermind. He has been featured and quoted in Nerdwallet, Bloomberg, Forbes, U.S. News & Money, USA Today, and other leading fina...

Jeff Root

Updated March 2025

If you have an auto loan and want to reduce your financial obligations, you may wonder if you can refinance. Refinancing involves taking out a new loan to replace the existing one, usually with a new lender, with your car serving as collateral until the loan is paid off.

- Should you refinance your car loan? Review your loan for potential savings

- Refinancing can lower your interest rate and monthly payments

- Exploring whether you can refinance car insurance may boost your savings

Benefits of Refinancing Your Auto Loan

When you refinance an auto loan, you receive a few distinct benefits. The top benefits of refinancing are as follows.

Score Lower Interest Rates

The number one reason people refinance their auto loans is to score lower interest rates. You may get a better rate if your credit has improved considerably since you first purchased your vehicle. The same is true if market rates are better now than back then.

Pay Off Your Debt Sooner

If you have the money to increase your monthly payments, you may consider refinancing to pay off your debt sooner. Shorter terms typically come with lower interest rates, which means that even though your monthly payments may be higher, you will ultimately pay less in the long run.

Get Lower Monthly Payments

On the flip side, you may choose to elongate the terms of your loan. If you struggle to pay the full amount each month, extending the life of your loan can score you a lower payment over a longer term. However, beware that your interest rates may go up and, regardless of if they do or not, you may end up paying more over the life of the loan.

Receive Cash From Your Equity

Some auto lenders offer cash-out refinance loans. With this type of loan, you may be able to refinance the original loan and receive some cash to put toward other expenses. This option may only be available if you have considerable equity in your vehicle.

If any of these benefits sound appealing to you, consider whether refinancing makes financial sense in the short and long term. Check whether it is bad to have a car insurance driver monitor.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Understanding Car Loan Refinancing and its Implications

Do you need money to refinance your car? This is a common question many borrowers ask when considering refinancing options. While having funds upfront isn’t always necessary, some lenders may require a fee to process the refinancing application.

For example, State Farm auto refinance offers competitive rates but may involve certain costs based on the borrower’s credit history. It’s essential to compare various providers to find the best companies for refinancing auto loans to ensure you’re getting the most favorable terms.

‘It may a good time’: Expert shares whether you should refinance your auto loan. Here’s when you’ll know https://t.co/zT3QnLDjQ4 pic.twitter.com/pmaS8B8EoN

— The Daily Dot (@dailydot) August 13, 2024

Additionally, when exploring refinancing options, it’s important to note that car loan refinancing in Petersburg might have unique requirements depending on local regulations. Check out car insurance with telematics for more.

Evaluating the Benefits and Drawbacks of Refinancing a Car Loan

Before making a decision, it’s crucial to understand the drawbacks of refinancing a car loan. While refinancing can reduce your monthly payments, it may extend the loan term, leading to higher overall costs.

Comparing car refinance options helps in identifying whether the potential savings outweigh the drawbacks. If you’re evaluating if refinancing your car is worth it, consider the impact on your credit score and possible fees. A comprehensive approach involves reviewing the pros and cons of refinancing a car to determine its long-term benefits.

Car Loan Refinancing Potential Savings by State

| State | Average Current Rate | Average Refinanced Rate | Potential Monthly Savings | Potential Total Savings |

|---|---|---|---|---|

| Alabama | 6% | 4% | $50 | $600 |

| California | 6% | 4% | $75 | $900 |

| Florida | 6% | 4% | $70 | $840 |

| Texas | 6% | 4% | $60 | $720 |

| New York | 5% | 3% | $85 | $1,020 |

| Pennsylvania | 5% | 3% | $55 | $660 |

| Illinois | 5% | 3% | $65 | $780 |

| Ohio | 6% | 4% | $50 | $600 |

| Georgia | 6% | 4% | $60 | $720 |

| North Carolina | 6% | 4% | $55 | $660 |

| Washington | 6% | 3% | $75 | $900 |

| Michigan | 6% | 4% | $80 | $960 |

| Arizona | 6% | 4% | $50 | $600 |

| Massachusetts | 5% | 3% | $65 | $780 |

| Virginia | 5% | 3% | $70 | $840 |

Additionally, exploring whether you can refinance car insurance separately may lead to further savings but can complicate your financial planning. Understanding the cons of refinancing a car will ensure that you’re making a well-informed decision.

Read more: Best Car Insurance in Alabama

Exploring State Farm Car Loan Refinancing and Insurance Options

When considering State Farm car loan refinancing options, it’s essential to understand how refinancing car insurance can also impact your overall financial plan. Refinancing your car insurance could potentially lower your monthly premiums, similar to the benefits of refinancing a car loan, which often include reduced interest rates and lower payments.

Refinancing your car loan can lead to significant savings, with 60% of borrowers averaging $75 per month.Jeff Root Licensed Insurance Agent

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Weighing the Pros and Cons of Refinancing a Car Loan

While there are several pros and cons of refinancing a car loan, you should evaluate whether it’s a smart move based on your unique financial situation. One common question is, is it worth refinancing a car for 1%? If the new rate only reduces your payment by a small amount, the savings may not justify the effort.

Additionally, there are reasons not to refinance your car, such as extending the loan term, which increases the total interest paid over time. Asking yourself it is smart to refinance a car loan involves considering these factors carefully. For those with existing loans, State Farm auto loan refinancing offers flexibility but should be weighed against other financial goals before proceeding.

Refinancing Your Car Loan

In many cases, the question isn’t, “Can you refinance a car loan?” but rather, “How soon can you refinance a car loan?” Below are a few factors to consider to help you decide if refinancing your auto loan in Petersburg makes sense for you right now.

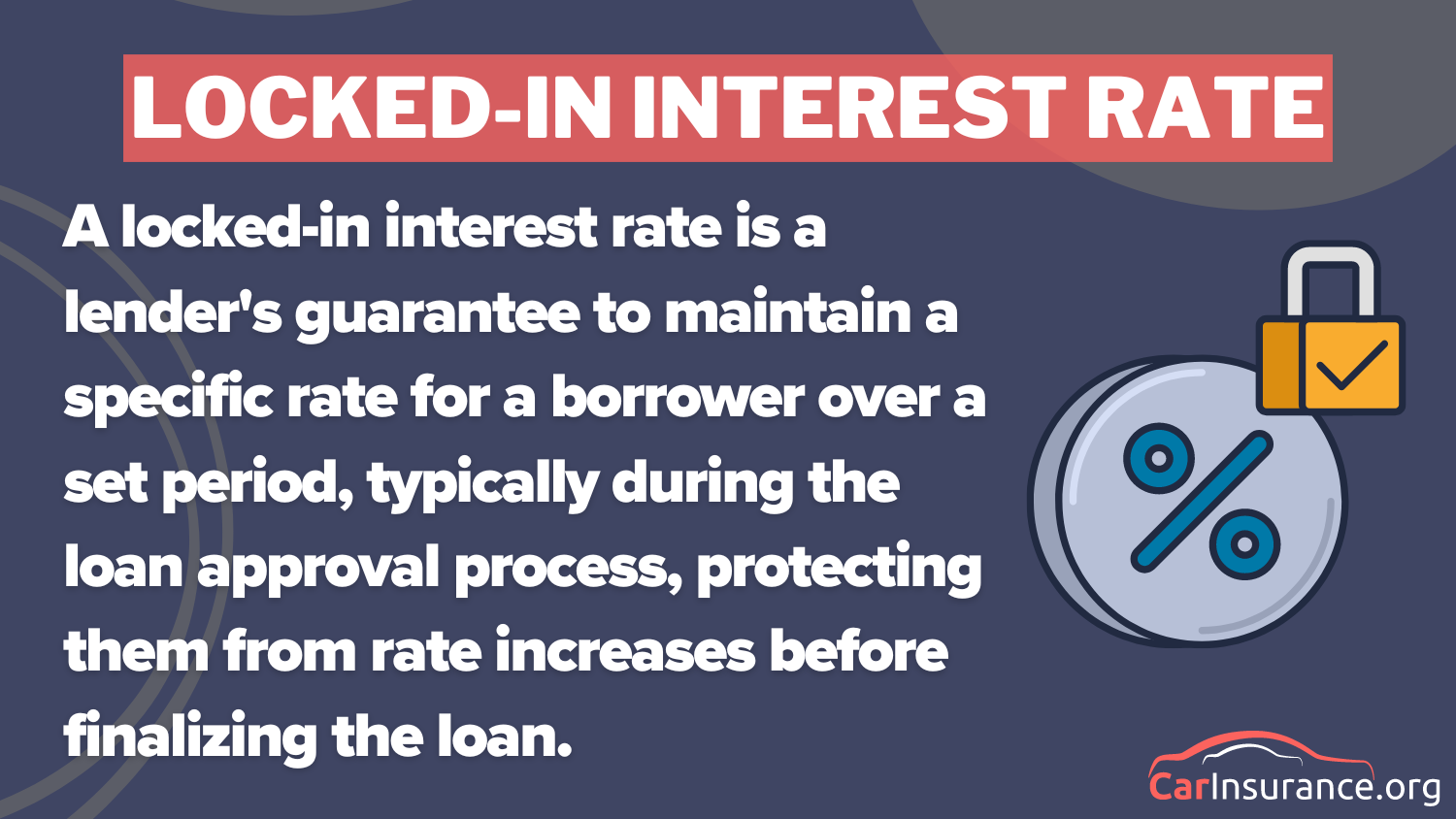

Interest Rates May Have Fallen Since You Got Your Loan

Interest rates fluctuate regularly, so there is a strong possibility that they have fallen since you took out your original loan. If you can lock in a rate that is even just two to three percentage points lower than your rates now, you can save thousands of dollars over the life of your loan.

As an example, consider how much you can save by scoring a rate that is 1% lower than your rate now. If you took out an auto loan for $36,000 at 7% interest for 60 months, you would pay a total of $42,771. However, if you refinance for a point lower, you will end up paying $41,759 for a savings of $1,102. If you shorten the life of that same loan, you can save an additional almost $1,500.

Credit Score May Have Improved Since You Took Out The Original Loan

If interest rates haven’t changed much since you took out your loan but your credit score has, you can still score a better rate by refinancing. For fair to poor credit, the average APR on a used vehicle is between 9.08% and 19.87%.

A good to excellent credit rating can get you a rate of between 5.38% and 3.61%. If you had less than stellar credit when you first took out the loan, it may make sense to refinance now that you’ve built it back up. Find the factors that affect the price of car insurance.

Access to More Capital

If you need to free up funds either by lowering your monthly payments or obtaining a cash-out refinance loan, refinancing may help.

Almost Paid Off Loan

If you have already almost paid off your loan in full, refinancing may make little sense. The longer you wait to refinance, the less you will save by doing so.

Refinancing May Impact Your Future Goals

When you refinance, you essentially obtain a new loan. If you hope to buy a home or other large asset in the near future, obtaining a new loan — even if for financial purposes — may get in the way of your goals. Waiting a couple more months will not minimize the benefits of refinancing, so hold until you’ve accomplished your goals before going through with the process.

How To Refinance a Car Loan

Refinancing an auto loan entails taking many of the same steps you took to obtain the original loan. That includes doing the following:

- Checking and improving your credit score

- Gathering income documentation

- Researching lenders

- Comparing loan offers

- Applying for the new loan

- Finalizing the contract

If your credit score has improved, and/or if you can show that you make timely payments on your current loan, you should have little trouble refinancing your auto loan.

Read more: Pros and Cons of Renting Your Car to Others

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Other Ways To Save Outside of Refinancing Your Auto Loan

If you decide refinancing is not for you, know that there are other ways you can save money on your monthly expenses, like reducing the cost of car insurance rates. When you shop around, you can save nearly $1,000 annually on auto insurance rates, which adds up to significantly more savings than what you can score with a refinance.

Refinancing your car loan can save you up to $100 a month on payments, making it a smart choice for many drivers seeking better rates.Brad Larson Licensed Insurance Agent

If you combine refinancing with newer, cheaper car insurance, you stand to save thousands. Take the first step toward cheaper car insurance rates. Enter your ZIP code below to see how much you could save.

Frequently Asked Questions

When should you refinance your car?

Refinancing is ideal when you can secure a lower interest rate, improve your credit score, or change the loan term to reduce monthly payments or total interest paid.

What are the cons of refinancing a car?

Cons include potential fees, a longer repayment period, and the possibility of negative equity if the car’s value is less than the remaining loan balance.

By entering your ZIP code below, you can get instant car insurance quotes from top providers.

Should you refinance your car for a lower interest rate?

Yes, refinancing for a lower interest rate can reduce your monthly payments and save you money over the life of the loan, making it a smart financial decision. Find out what things you can do to raise your insurance premiums.

How long should you wait to refinance your car?

It’s advisable to wait at least six months after obtaining your loan or after significant credit score improvements to ensure better refinancing options.

Does it make sense to refinance a car loan?

Yes, it can make sense if you find a significantly lower interest rate, wish to change the loan term, or want to lower your monthly payments.

Does State Farm refinance car loans?

Yes, State Farm offers refinancing options for car loans through its affiliated lending partners.

Curious to learn more? Find out whether insurance will cover a rental if your car breaks down.

Does refinancing a car hurt your credit?

Refinancing can have a temporary negative impact on your credit score due to a hard inquiry, but it may improve your score in the long run if it reduces your debt-to-income ratio.

Does refinancing look bad on credit?

Not necessarily; while it may cause a small dip in your score initially, responsible management of the new loan can lead to improvements over time.

Is refinancing a risk?

Yes, refinancing carries risks, such as extending your loan term, which could lead to paying more interest over time and possibly falling into negative equity. Find out if used car insurance is cheaper.

What happens after refinancing?

After refinancing, you’ll receive a new loan with updated terms, and you’ll need to make payments according to the new agreement. The old loan will be paid off, and your credit may be impacted slightly.

Related Articles

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.