Best Car Insurance in Alabama in 2026 [Your Guide to the Top 10 Companies]

State Farm, Geico, and Progressive, have the best car insurance in Alabama, with rates starting at $20 per month. Whether you need customizable coverage from State Farm, the lowest rates from Geico, or help with budgeting from Progressive, you'll find cheap insurance in Alabama.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Insurance Feature Writer

Rachel Bodine graduated from college with a BA in English. She has since worked as a Feature Writer in the insurance industry and gained a deep knowledge of state and countrywide insurance laws and rates. Her research and writing focus on helping readers understand their insurance coverage and how to find savings. Her expert advice on insurance has been featured on sites like PhotoEnforced, All...

Rachel Bodine

Licensed Insurance Agent

Eric Stauffer is an insurance agent and banker-turned-consumer advocate. His priority is educating individuals and families about the different types of insurance coverage. He is passionate about helping consumers find the best coverage for their budgets and personal needs. Eric is the CEO of C Street Media, a full-service marketing firm and the co-founder of ProperCents.com, a financial educat...

Eric Stauffer

Updated March 2025

18,157 reviewsCompany Facts

Full Coverage in Alabama

A.M. Best Rating

Complaint Level

Pros & Cons

18,157 reviews 19,116 reviews

19,116 reviewsCompany Facts

Full Coverage in Alabama

A.M. Best Rating

Complaint Level

Pros & Cons

19,116 reviews 13,285 reviews

13,285 reviewsCompany Facts

Full Coverage in Alabama

A.M. Best Rating

Complaint Level

Pros & Cons

13,285 reviewsState Farm, Geico, and Progressive have the best car insurance in Alabama, with rates starting at $20 per month. Each insurer has its benefits, like State Farm has the best customizable coverage, Geico has the lowest rates, and Progressive has its budgeting tools.

Picking through the hundreds of car insurance providers is daunting. How do you know what provider is right for you from all the insurers available?

Our Top 10 Company Picks: Best Car Insurance in Alabama

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 17% | B | Customizable Coverage | State Farm | |

| #2 | 25% | A++ | Lowest Rates | Geico | |

| #3 | 10% | A+ | Budgeting Tools | Progressive |

| #4 | 10% | A++ | Military Families | USAA | |

| #5 | 25% | A+ | Value Services | Allstate | |

| #6 | 20% | A | Policy Customization | Farmers |

| #7 | 20% | A+ | Bundling Discounts | Nationwide | |

| #8 | 25% | A | Coverage Add-Ons | Liberty Mutual | |

| #9 | 13% | A++ | Driver Discounts | Travelers | |

| #10 | 25% | A | Family Packages | American Family |

When you pay hundreds every year for car insurance, you want to know that your money is well spent. That’s why we have put together this comprehensive guide. We cover everything from Alabama insurance providers and requirements to must-know facts.

Want to start comparing Alabama car insurance quotes today? Enter your ZIP code using our free online tool above.

- Alabama’s car insurance cost average is below the national average

- USAA is the cheapest under certain requirements

- Always shop around for the right coverage for you

#1 – State Farm: Best for Customizable Coverage

Pros

- Extensive Agent Network: State Farm has many local agents, making it easy to get specialized AL car insurance quotes personally.

- Customizable Coverage Options: Alabama motorists can get various coverage options, including liability, comprehensive, collision, uninsured/underinsured motorist, and more.

- High Financial Strength: State Farm can cover claims effectively, even during large-scale disasters, contributing to its standing as the best auto insurance in Alabama.

Cons

- Premiums Can Be Higher Without Discounts: Premiums can be higher for Alabama drivers who don’t qualify for extra savings.

- No Gap Coverage: This disadvantages Alabama drivers financing newer vehicles. The State Farm Car Insurance review tells more on what add-ons are available.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#2 – Geico: Best for Lowest Rates

Pros

- Affordable Premiums: Geico’s premiums are one of the cheapest car insurance in Alabama and often have the lowest rates.

- Robust Digital Tools: Geico’s highly rated digital services offer features to simplify Alabama drivers’ policy handling.

- Wide Range of Discounts: Geico offers Safe Driver Discount by having a clean driving record through DriveEasy and Military discounts in Alabama.

Cons

- Limited Local Agent Network: Geico operates online and by phone, so this may not appeal to Alabama drivers who prefer face-to-face interaction.

- Higher Rates for High-Risk Drivers: Rates can be less favorable for Alabama drivers with accidents, tickets, or a poor credit history.

#3 – Progressive: Best for Budgeting Tools

Pros

- Competitive Rates for High-Risk Drivers: Progressive is affordable for Alabama’s high-risk drivers. Read the Progressive Car Insurance review to find out more.

- Wide Range of Coverage Options: Offers standard coverage and extras such as Gap insurance and Ride-sharing coverage, which are helpful for drivers in Alabama’s needs.

- Usage-Based Discounts: The Snapshot program monitors driving habits and rewards those driving safely with cheap Alabama car insurance rates.

Cons

- Higher Rates for Low-Risk Drivers: While competitive for high-risk drivers, rates for safe Alabama drivers can sometimes be higher.

- Telematics Concerns: The Snapshot program requires tracking your driving habits. Any poor driving behavior around Alabama recorded results in higher premiums.

#4 – USAA: Best for Military Families

Pros

- Highly Competitive Rates: USAA has one of the best Alabama car insurance for military members, veterans, and their families. Read USAA insurance review to find out more.

- Outstanding Customer Service: USAA has highly rated customer satisfaction for its attentiveness and reliable support for Alabama drivers.

- Military-Specific Benefits: Active-duty members have extra benefits, such as Alabama vehicle storage discounts while deployed.

- Usage-Based Discounts: Programs like SafePilot allow safe Alabama drivers to earn additional savings by tracking driving habits.

Cons

- Eligibility Restrictions: USAA is strictly for military members, veterans, and their families. If you’re not eligible, you won’t be able to access their services in Alabama.

- Limited Local Agent Network: USAA primarily operates online or by phone, which may not appeal to those in Alabama who prefer face-to-face service.

- No Gap Insurance: USAA provides a total loss protection add-on for financed vehicles instead of gap insurance in Alabama.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#5 – Allstate: Best for Value Services

Pros

- Extensive Agent Network: Allstate has a strong local presence in Alabama, so getting personalized advice and service is more effortless.

- Wide Range of Coverage Options: Allstate offers standard coverage and additional options; the Allstate car insurance review tells more.

- Unique Features and Tools: Allstate’s Drivewise program rewards drivers with discounts for driving safely in Alabama.

- Good Discounts: There are various discounts for cheap insurance in Alabama, such as Safe Driver, Early Signing, and Responsible Payer Discount.

Cons

- Higher Premiums Without Discounts: Allstate’s Alabama car insurance rates tend to be higher than competitors, especially without discounts.

- Drivewise May Affect Rates: While Drivewise can offer discounts, poor driving behavior can result in more expensive Alabama auto insurance quotes.

- Not Ideal for High-Risk Drivers: Alabama drivers with poor credit or a history of accidents may find better rates with other insurers specializing in high-risk coverage.

#6 – Farmers: Best for Policy Customization

Pros

- Extensive Coverage Options: Farmers offers Alabama drivers standard coverage and valuable add-ons like Accident forgiveness and New car replacement.

- Personalized Service: Farmers operate through local Alabama agents, offering customized advice. Farmers Insurance review tells more on the provided services.

- Discount Opportunities: Farmers provides Alabama drivers various discounts, including multi-car discounts, Safe driver, and good student discounts.

- Signal Telematics Program: A usage-based program that rewards safe driving habits in Alabama, offering feedback and tracking through a mobile app.

Cons

- Higher Premiums: Farmers tend to have higher base rates than competitors for cheap car insurance in Alabama.

- >Limited Digital Experience: Farmers’ app and website may not be as user-friendly or feature-rich as other Alabama car insurers.

- Not Ideal for High-Risk Drivers: Farmers may not offer competitive rates for Alabama drivers with accidents, tickets, or poor credit.

#7 – Nationwide: Best for Bundling Discounts

Pros

- SmartRide Telematics Program: Safe Alabama drivers can earn discounts based on monitored driving habits through the usage-based insurance program.

- Extensive Discounts: Nationwide offers discounts that contribute to cheap car insurance in Alabama. Read the Nationwide Insurance review to find out more.

- Local Agent Support: In Alabama, Nationwide provides access to a network of local agents for personalized service and support.

- Flexibility for High-Risk Drivers: Nationwide offers competitive rates and coverage options for Alabama drivers with accidents or poor credit.

Cons

- Higher Premiums Without Discounts: Nationwide’s rates may be higher for Alabama drivers, particularly those not qualifying for multiple discounts.

- Telematics Privacy Concerns: Participation in the SmartRide program requires driving behavior tracking, which may not appeal to every Alabama driver.

- Not Ideal for Fully Digital Service: Alabama drivers who prefer an entirely digital experience might find competitors more appealing.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#8 – Liberty Mutual: Best for Coverage Add-ons

Pros

- Customizable Coverage Options: Liberty Mutual offers standard and optional coverage, making it one of Alabama’s best car insurance companies.

- Strong Discounts: Liberty Mutual provides a variety of discounts if you’re looking for Alabama’s cheap auto insurance.

- Usage-Based Insurance: The RightTrack program offers Alabama drivers savings of up to 30% based on safe driving habits.

- Local Agents and Digital Tools: Liberty Mutual combines the convenience of digital tools with access to local Alabama agents for in-person support.

Cons

- Higher Premiums: Liberty Mutual’s rates can be higher than those of other insurers operating in Alabama.

- Telematics Privacy Concerns: The RightTrack program requires monitoring your driving habits around Alabama, which may feel intrusive to some drivers.

- Not Ideal for High-Risk Drivers: Liberty Mutual may not be as competitive for drivers with poor credit, accidents, or traffic violations.

#9 – Travelers: Best for Driver Discounts

Pros

- Extensive Coverage and Customizable Options: Travelers offers standard and optional coverages for Alabama drivers. Travelers also tailor your policy to your needs.

- Competitive Discounts: Travelers provides discounts for cheap auto insurance in Alabama to lower car insurance costs.

- Wide Availability of Local Agents: Travelers operate through a network of agents, providing personalized advice and local support in Alabama.

Cons

- Limited Add-Ons in Some Areas: Not all optional coverages are available in Alabama.

- Add-Ons Can Increase Costs: Adding extras like gap insurance or accident forgiveness can significantly raise your premium in Alabama.

#10 – American Family: Best for Family Packages

Pros

- Teen Safe Driver Program: Teen drivers in Alabama are provided with monitoring tools and resources to promote safer driving habits and potentially lower premiums.

- Special Perks for Families: Amfam has family-focused programs and benefits, making it a good option for Alabama households with multiple drivers.

- Strong Customer Service and Local Agents: American Family has a network of local agents in Alabama. Check out the AmFam Insurance review for more.

Cons

- Limited Availability: American Family is not as widely available in Alabama as larger insurers, which may limit access in certain areas.

- Not Ideal for High-Risk Drivers: Alabama drivers with poor credit, a history of accidents, or traffic violations may find more affordable options elsewhere.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Alabama Car Insurance Rates and Coverage

Driving without insurance is illegal, but every state has different coverage requirements. If you are moving to Alabama or purchasing car insurance for the first time, knowing what Alabama law requires can be overwhelming.

Alabama Auto Insurance Monthly Rates by Provider & Coverage Level

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $39 | $108 | |

| $38 | $105 | |

|

| $48 | $133 |

| $32 | $89 | |

| $58 | $162 | |

| $34 | $96 | |

|

| $40 | $112 |

| $39 | $108 | |

| $28 | $79 | |

| $20 | $56 |

While insurance providers will help you get the mandatory coverage, you must also know what rates are best in your area when shopping for the cheapest car insurance in Alabama.

Alabama Core Coverage Rates

| Coverage Type | Monthly Rates |

|---|---|

| Liability | $40 |

| Collision | $55 |

| Comprehensive | $45 |

| Combined Total | $140 |

Because these rates are from 2015, remember that rates for 2025 and beyond will be slightly higher than the ones shown above. Shopping around for insurance providers and rates, though, will help keep costs down.

The good news is that because the countrywide average total for car insurance is $75, Alabama residents are still paying LESS for full car insurance than most U.S. residents.

Alabama’s Insurance Rates by Age and Gender

Plenty of outside factors influence rates. One factor that may surprise you is gender. Females will find that they generally pay more for car insurance than males with most providers, even with the same driving record and history.

This contradicts the popular belief that males ALWAYS pay more than females for car insurance! Age is also a huge factor, though this one isn’t as surprising.

Alabama Male Female Rates

| Insurance Company | Age: 17 Female | Age: 17 Male | Age: 25 Female | Age: 25 Male | Age: 35 Female | Age: 35 Male | Age: 60 Female | Age: 60 Male |

|---|---|---|---|---|---|---|---|---|

| $350 | $375 | $150 | $160 | $130 | $135 | $120 | $125 | |

| $340 | $370 | $145 | $155 | $125 | $130 | $115 | $120 | |

|

| $355 | $385 | $155 | $165 | $135 | $140 | $125 | $130 |

| $300 | $320 | $120 | $130 | $110 | $115 | $105 | $110 | |

| $340 | $370 | $145 | $155 | $125 | $130 | $115 | $120 | |

| $330 | $360 | $140 | $150 | $120 | $125 | $110 | $115 | |

|

| $310 | $340 | $130 | $140 | $115 | $120 | $110 | $115 |

| $320 | $350 | $135 | $145 | $120 | $125 | $110 | $115 | |

| $330 | $360 | $140 | $150 | $120 | $125 | $110 | $115 | |

| $290 | $310 | $115 | $125 | $105 | $110 | $100 | $105 |

Due to the common risks faced by teen drivers, younger drivers pay thousands more than older drivers unless parents add younger drivers to the parent’s insurance plan. Luckily, we have the perfect tool for car insurance quotes in Alabama, just enter your ZIP code below. We’ve also broken down Alabama’s insurance requirements for you.

Alabama’s Minimum Coverage Requirements

In Alabama, drivers need to have the state’s minimum coverage insurance. You face heavy fines or worse if you aren’t insured with the required bodily injury and property damage liability coverages.

Below are the coverage amounts Alabama requires ALL drivers to have (these coverages protect drivers in case of an accident).

- $25,000 coverage per person that pays for one person injured from the accident

- $50,000 coverage per accident to pay for all people injured from the accident

- $25,000 to pay for any property damage from the accident

It is important to note that the above amounts are only the MINIMUM amounts required. If you are in an accident, having more than the minimum coverage to cover unforeseen costs is wise.

Alabama Report Card: Car Insurance Premiums

Category Grade Explanation

Average Claim Size B Moderate-sized claims reported

Traffic Density B- Traffic congestion manageable

Weather-Related Risks C+ Frequent severe weather events

Vehicle Theft Rate C Theft rates slightly above average

Uninsured Drivers Rate D High uninsured driver percentage

From the table above on insurance premiums, it’s important to note that many drivers are not insured in Alabama despite it being required. Along with their slightly above-average theft rates, this alters minimum coverage costs to be slightly higher.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

The Available Add-ons, Endorsements, and Riders

We’ve covered additional liability coverages, but there are also great add-ons that you can purchase for your regular policy. While adding more to a policy that already covers all the basics may seem excessive, these coverages are practical and affordable.

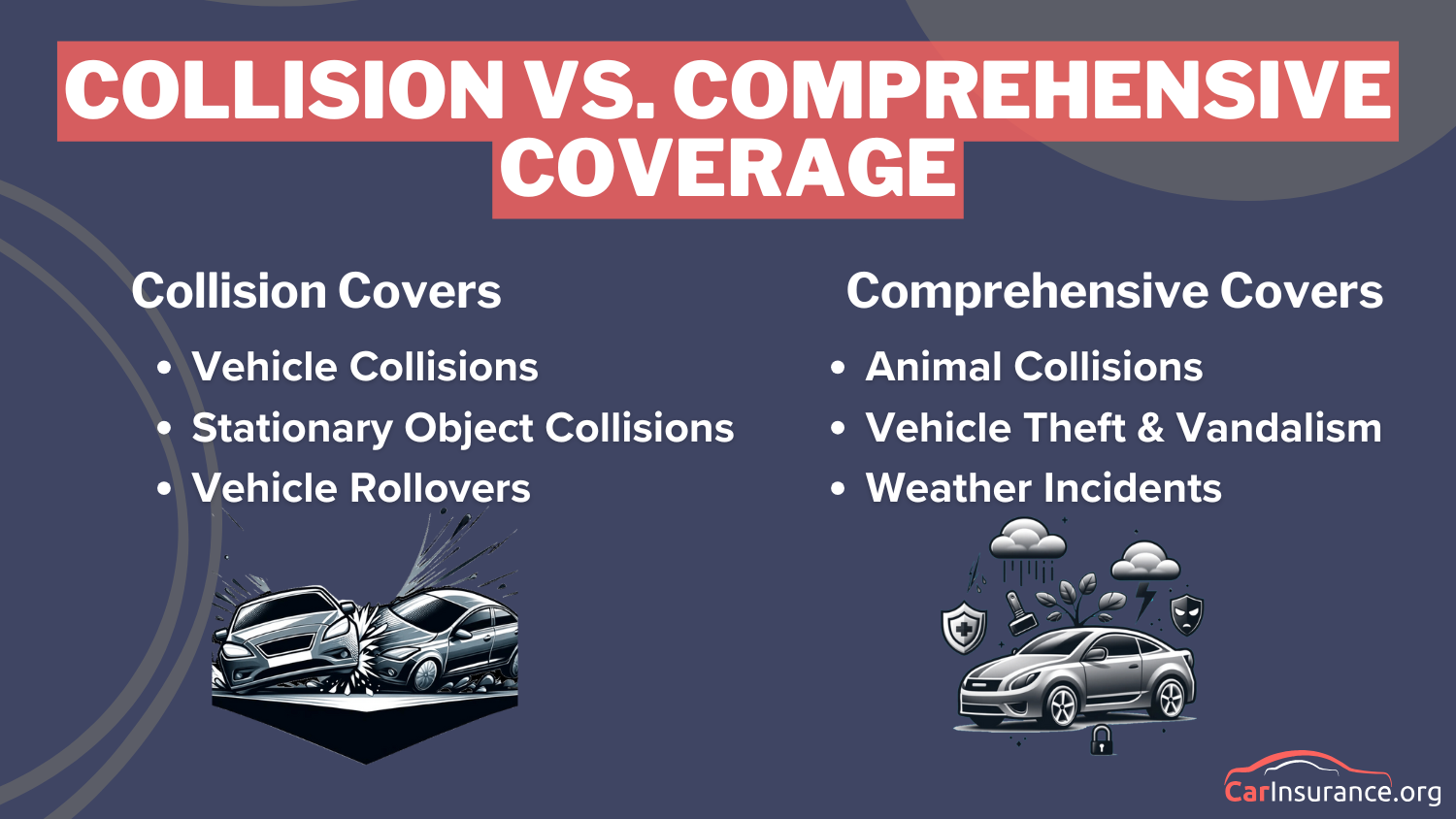

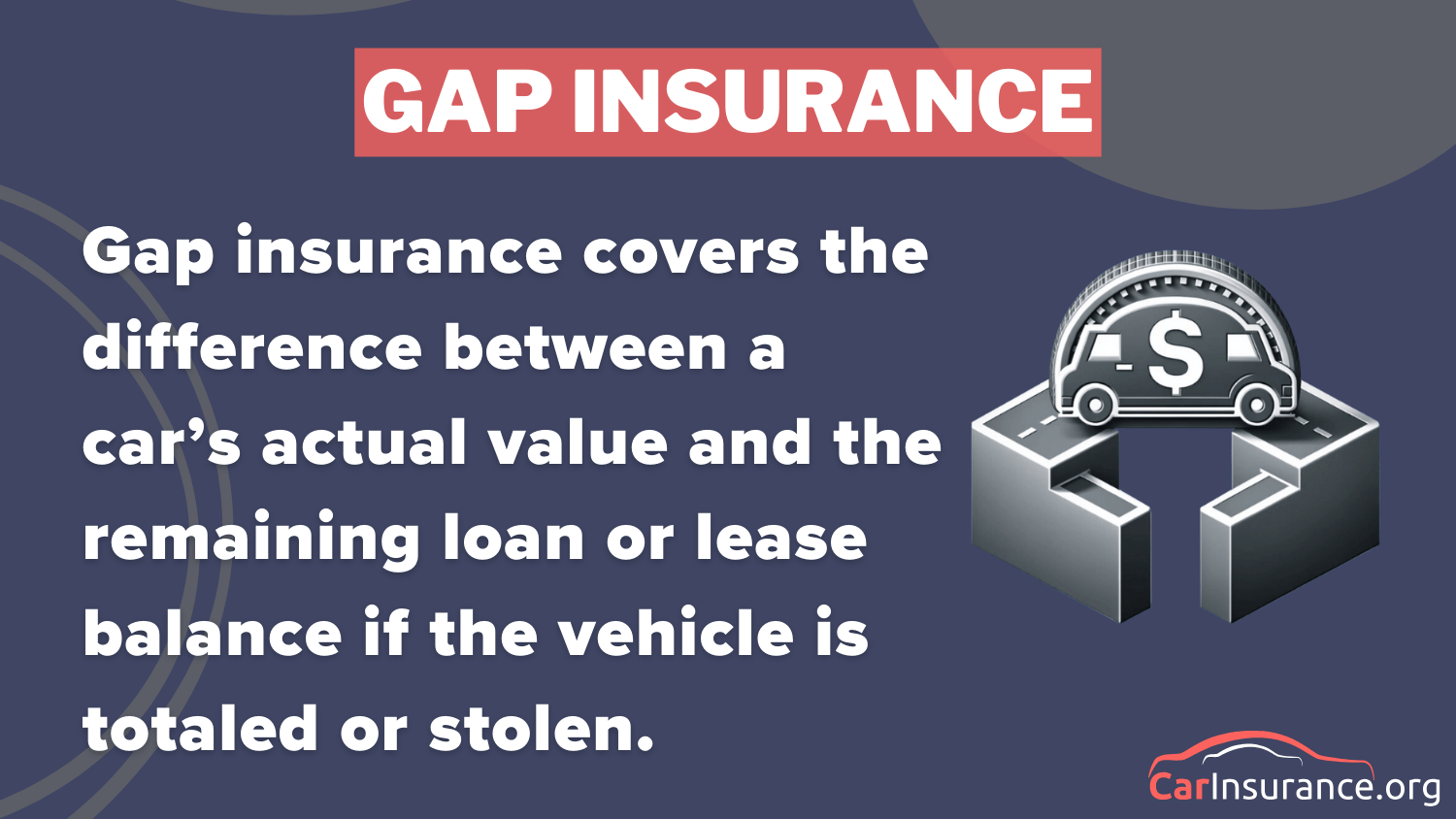

Gap Coverage as an add-on is worth looking at if you have a newer vehicle that is financed. New vehicles depreciate rapidly in the first few years, so if you've financed a new vehicle, you could owe more than the car is currently worth. If you get into an accident and the car is totaled, the insurer will only pay the vehicle's value; Gap Coverage covers that difference from what you owe.Michelle Robbins Licensed Insurance Agent

Best of all, you can pick and choose add-ons to create a plan that is custom-suited to your needs. For example, you’ll want special protection if you have a classic car! Look through the list of affordable and effective add-ons below to learn more.

- Gap insurance: Gap insurance pays the price difference between your car’s actual cash value and what you still owe on your car’s loans.

- Personal umbrella policy: Think of this insurance as an extension of liability insurance. PUP insurance helps protect you from lawsuits in case of an accident.

- Rental reimbursement: If you are in an accident and your car is in the shop, rental reimbursement will help pay the costs of renting a car.

- Emergency roadside assistance: This coverage helps you if your car breaks down. Your provider will pay for the roadside repair or towing.

- Mechanical breakdown insurance: If your car needs to be repaired due to something other than an accident, this coverage will pay for your repairs.

- Non-owner car insurance: If you don’t own a vehicle but still drive, this insurance will provide liability coverage.

- Modified car insurance coverage: If you like to customize your cars, you may need to purchase modified car insurance.

- Classic car insurance: Classic cars need protection different from regular cars. Generally, classic car insurance costs less, as classic cars aren’t driven as much.

- Usage-based insurance: This coverage gives discounts based on the driver’s speed, distance, and other factors. Insurers will give drivers a device to install in their car that records this information.

There are plenty of insurance add-on options! While the number of options may seem overwhelming, the variety means you can create a policy plan that is perfect for you.

The Best Auto Insurance Companies in Alabama

The multitude of road drivers means that insurance providers are in demand. More companies, though, means more choices. Finding an insurance company that is right for YOU can be challenging.

How do you know what rates provide you with the best benefits for your money? Insurers all promise their coverage is the best, but these declarations are false. There are many things to consider such as what discounts are on offer, what kind of coverage that will apply to your needs and more.

Alabama Report Card: Car Insurance Discounts

| Insurance Company | Anti-Theft | Bundling | Good Driver | Good Student | UBI |

|---|---|---|---|---|---|

| 10% | 25% | 25% | 20% | 30% | |

| 25% | 25% | 25% | 20% | 30% | |

|

| 10% | 20% | 30% | 15% | 30% |

| 25% | 25% | 26% | 15% | 25% | |

| 35% | 25% | 20% | 15% | 30% | |

| 5% | 20% | 40% | 15% | 40% | |

|

| 25% | 10% | 30% | 10% | $231/yr |

| 15% | 17% | 25% | 25% | 30% | |

| 15% | 13% | 10% | 8% | 30% | |

| 15% | 10% | 30% | 10% | 30% |

We want you to know your options before you throw in the towel and stick with the same provider you’ve always had. There are important factors to consider when choosing a provider, but luckily they are pretty straightforward.

Alabama State Laws Do You Need to Know

To follow the law, you need to know the law! However, it can often be confusing to understand the different driving laws. After all, driving laws are slightly different across states. Breaking a driving law, though, will result in a fine and perhaps other penalties (such as a suspended license).

Knowing your state laws is necessary, so we will give you an overview of essential laws in Alabama. Although all drivers must have insurance, there is a small catch.

Insurance companies can refuse to sell car insurance if you are a high-risk driver. If insurers refuse to sell a car insurance plan to you, you must purchase insurance from Alabama’s Auto Insurance Plan (AAIP). If you practice safe driving and state laws, you can proactively prevent being labeled as a high-risk driver. In turn, this will save you from increased rates.

Another fact you should know is that Alabama does NOT have an unfair claims settlement act. The Unfair Claims Settlement Act requires insurers to fully disclose what a policy covers so that insurers don’t conveniently “forget” benefits when they make a claim.

Because Alabama doesn’t have this law, you need to know your policy inside and out. You will notice a small mistake if you see what insurers owe you.

Vehicle Licensing Laws

If you drive without insurance, you face strict penalties. While the cost of car insurance can be daunting, the penalties for skipping are worse.

Penalties for Driving Without Insurance in Alabama

| Offense | Details |

|---|---|

| 1st | - Fine $500 - Registration suspension with $200 reinstatement fee |

| 2nd | - Fine $1,000 and/or six-month license suspension - $400 reinstatement fee with four-month registration suspension |

If you recall, Alabama accepts the following as proof of financial responsibility.

- A valid liability insurance ID card

- A copy of your car’s insurance policy

- A valid insurance binder (a temporary form of car insurance)

- A picture of your insurance ID card on your smartphone

Suppose authorities pull you over or are in an accident. In that case, you must provide proof of registration, proof of insurance, and a driver’s license.

Alabama may suspend your vehicle’s registration if you don’t have car insurance. Authorities will notify you if your registration is being suspended. According to the Alabama Department of Revenue, authorities may suspend your vehicle registration for specific reasons.

- “The Department did not receive a timely response to a questionnaire sent to verify the MLI coverage on the vehicle.”

- “The insurer identified in response to the questionnaire has failed to confirm or has denied coverage on the vehicle for the insurance verification date as requested.”

It is essential to have insurance; otherwise, you could lose the right to drive altogether because of a suspended license and registration. To learn more, check out the Alabama Set for Insurance Verification System. Teen drivers have restrictions placed on them to help them learn in a semi-controlled environment.

Alabama Teen Driver License Restrictions

Restrictions Details

Nighttime restrictions Midnight to 6 a.m.

Passenger restrictions (family members excepted unless noted otherwise) no more than 1 passenger

Age Limit Details

Nighttime restrictions 17 and licensed for 6 months (minimum age: 17)

Passenger restrictions 17 and licensed for 6 months (minimum age: 17)

To drive, drivers must have a learner’s license or permit at the age of 15 and meet the requirements before they can receive a restricted or adult license.

Alabama Teen Driver License Requirements

Requirements Time Restrictions

Mandatory Holding Period 6 months

Minimum Supervised Driving Time 50 hours (none with driver education)

Minimum Age 16 years old

Without proper training, teens risk negligent or reckless driving in the future, which becomes a serious issue. If people endanger themselves or others through careless driving, authorities WILL charge the drivers with reckless driving. Alabama law lists the following penalties:

- 1st Conviction: imprisonment for five to 90 days. Fine $25 to $500.

- 2nd Conviction: imprisonment for 10 days to six months. Fine $50 to $500. License suspension.

Reckless driving risks your and others’ safety, so drive carefully. If you don’t, you’ll end up in jail, and your future auto insurance fees will increase exponentially.

High-Risk Insurance

Sometimes, despite our best efforts, accidents happen. If an accident happens, authorities may require you to fill out an SR-22 form. This form is essentially an application for high-risk insurance, so your rates will increase. In multiple situations, authorities may require you to fill out an SR-22 form:

- A DUI/DWI

- Uninsured driving

- A traffic violation that causes serious injury/death

- High number of points on driving record

- High-risk car (think sports cars, etc.)

Insurance providers may not cover you if you are considered a high-risk driver and have SR-22 forms on your account. You will then need to apply for car insurance through the AAIP.

Statute of Limitations

Every state has a different amount of time in which you can file a claim, which is also known as a statute of limitations. If you don’t file and resolve your claim within the statute of limitations, you lose your chance to be paid the money you are owed.

5 Most Common Car Insurance Claims in Alabama

| Claim Type | Portion of Claims | Average Cost per Claim |

|---|---|---|

| Collision | 40% | $3,000 |

| Comprehensive (e.g., theft, weather) | 20% | $2,500 |

| Bodily Injury Liability | 15% | $15,000 |

| Property Damage Liability | 15% | $5,000 |

| Uninsured/Underinsured Motorist | 10% | $10,000 |

The statute of limitation’s time limit usually starts on the date of your accident, so make sure to file as soon as possible. Below, you will see Alabama’s statute of limitations, which is short compared to other states.

- Personal Injury: Two years

- Property Damage: Two years

Two years may seem like a long time, but it is easy to forget things you put off until tomorrow or next week. So, make sure to file that claim as soon as possible so you can get the claim process started. After all, the sooner you are paid, the better!

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Alabama’s Rules of the Road

Knowing the road rules inside and out increases your chances of staying safe while driving. Not to mention keeping others safe as well! Keep reading to learn about some of Alabama’s most important rules of the road.

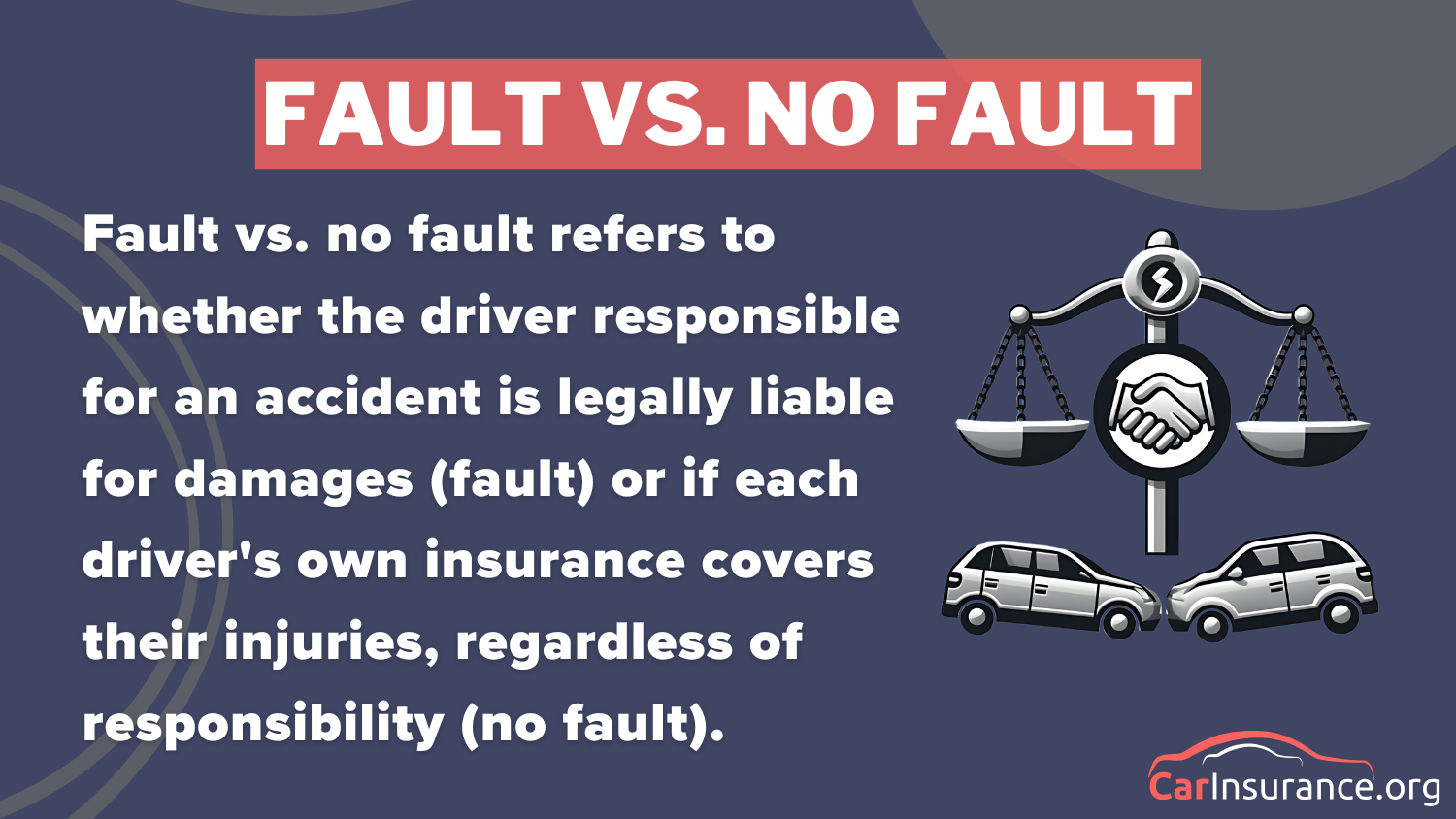

Fault vs No-Fault

Alabama is an at-fault state. This means the at-fault driver is liable for all accident-related costs, such as medical and property damage bills. This is completely different from a no-fault state, where both drivers have to pay for their own damages.

If an at-fault driver doesn’t have insurance or has poor coverage, he or she will be unable to pay off all the accident costs and risk going bankrupt. So follow the law and get insurance, as it is costly not to! Insurance will ensure you don’t lose your savings over an accident.

Speed Limits in Alabama

Below is the information on Alabama’s maximum speed limits. Be aware that speed limits vary from road to road — these are the absolute highest speeds on roadways.

Alabama Speed Limits

| Roadway | Speed Limit |

|---|---|

| Rural Interstates | 70 mph |

| Urban Interstates | 65 mph |

| Other Limited Access Roads | 65 mph |

| Other Roads | 65 mph |

If you go over the posted speed limits, you will receive a fine and points on your driving record (which may raise your insurance prices).

Alabama Seat Belt and Car Seat Laws

Alabama also has laws on seat belts and car seat use. These laws ensure drivers and passengers are safe — seat belt use helps prevent occupants from being thrown from the car in accidents. If you violate Alabama’s seat belt laws, you will receive fines.

Read more: What are the Alabama car seat laws?

Alabama Seat Belt Laws

| Safety Belt Laws in Alabama | Details |

|---|---|

| Effective Since | June 18, 1991 |

| Primary Enforcement | Yes; effective since December 9, 1999 |

| Age/Seats Applicable | 15+ years old in front seat |

| 1st Offense Max Fine | $25 plus fees |

Primary enforcement means that if an officer sees you are not wearing a seatbelt, they can pull you over and ticket you. Alabama requires backseat passengers to buckle up. Alabama’s car seat laws are fairly simple. Follow the rules below to keep children safe in the car.

Alabama Car Seat Laws

| Type of Car Seat Required | Age/Weight |

|---|---|

| Rear-Facing Child Restraint | Younger than one year old or less than 20 pounds |

| Forward-Facing Child Restraint | One to four years old or 20 - 40 pounds |

| Child Booster Seat | Five (but under six years old) |

| Adult Belt Permissible | Six through 14 years |

The fine for breaking the above laws is $25 plus fees. Alabama doesn’t have laws restricting riding in the cargo areas of pickup trucks. Just use common sense for everyone’s safety, as people can easily be thrown from pickups at sharp turns.

Alabama DUI Laws

Did you know around 300 people are killed annually in Alabama due to alcohol-related driving incidents. Drunk driving is one of the biggest culprits in driving fatalities.

Alabama has made drunk driving illegal (the same as every state) to help cut back on the number of drunk driving fatalities. The more that people are aware of the consequences of driving drunk, the less incentive there is to drive under the influence.

Alabama DUI Law

| Details | |

|---|---|

| Name for Offense | Driving under the influence (DUI) |

| BAC Limit | 0.08 |

| High BAC Limit | 0.15 |

| Criminal Status | 1st to 3rd offenses are misdemeanors; 4th+ in 5 years is a class C felony |

| Look Back Period | 5 years |

If you break the law, there are strict penalties in place that grow steadily worse with each offense. These strict penalties are in place for a reason — drunk driving strips away people’s judgment and results in frequent and often deadly accidents. In 2017, there were 268 deaths from alcohol-related accidents.

So stay safe — never drink and drive, and encourage others to do the same. Otherwise, you could lose the right to drive altogether, along with jail time and steep fines.

Marijuana-Impaired Driving Laws

There isn’t a specific law in place about marijuana-impaired driving in Alabama, but you can still be charged with impaired driving.

Did you know marijuana can stay in your system for weeks after use? If an officer thinks you're impaired and tests you, you can still be charged with impaired driving, EVEN if you aren't high at the time.Tracey L. Wells Licensed Insurance Agent & Agency Owner

Driving under the influence of marijuana will result in many of the same penalties as a DUI — suspended license, fines, and jail time.

Distracted Driving Laws

All it takes is a second with your eyes off the road for there to be an accident. Distracted driving is a major cause of accidents. In fact, distracted driving is just as dangerous as driving drunk! Alabama has created the following cellphone use laws to help regulate distracted driving.

Cellphone Use Laws in Alabama

| Details | |

|---|---|

| Hand-held ban | 16-year-old drivers; 17-year-old drivers who have held an intermediate license for fewer than 6 months |

| Text ban | All drivers |

| Enforcement | Primary |

Remember, primary enforcement allows officers to pull you over just for texting on your phone while driving.

Vehicle Theft in Alabama

Do you know what hazards to watch out for on your roads? All it takes is one mistake for an accident to happen! Knowing what the main driving risks are in Alabama can help you stay wary and avoid potential accidents.

To stay as safe as possible, keep reading to learn about the major causes of accidents in Alabama, as well as information about vehicle theft and commute times. Some types of cars are stolen significantly more often than other models. Check below to see if your vehicle makes the list!

Alabama Vehicle Thefts

| Vehicle Make/Model | Vehicle Year | Total Stolen |

|---|---|---|

| Chevrolet Pickup (Full Size) | 2005 | 499 |

| Ford Pickup (Full Size) | 2006 | 357 |

| Toyota Camry | 2014 | 205 |

| Nissan Altima | 2014 | 191 |

| Chevrolet Impala | 2004 | 191 |

| Honda Accord | 1998 | 180 |

| GMC Pickup (Full Size) | 1999 | 152 |

| Dodge Pickup (Full Size) | 1998 | 138 |

| Ford Mustang | 2002 | 122 |

| Ford Explorer | 2002 | 119 |

Next, we will examine some of the risk factors you should look for that involve harmful and risky behavior by drivers.

Alabama’s Crash Report

Where you live can affect the number of traffic fatalities. Three of Alabama’s cities made the National Highway Traffic Safety Administration’s (NHTSA) list of the highest-ranked cities for fatalities.

Road type also influences traffic fatalities. Generally, higher speeds on rural roads equal more significant impacts. The worse the impact, the more likely there is to be a fatality.

Alabama Accidents & Claims per Year by City

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Auburn | 2,500 | 1,750 |

| Birmingham | 15,000 | 10,500 |

| Decatur | 3,000 | 2,100 |

| Dothan | 3,500 | 2,450 |

| Gadsden | 2,000 | 1,400 |

| Hoover | 4,000 | 2,800 |

| Huntsville | 8,000 | 5,600 |

| Mobile | 12,000 | 8,400 |

| Montgomery | 9,000 | 6,300 |

| Tuscaloosa | 6,000 | 4,200 |

Another major culprit in traffic fatalities is drunk driving. Drinking severely impairs a driver’s judgment, which is the last thing you want when driving! All it takes is one slight swerve off the road or a missed stop sign to cause a fatal accident.

A sobering part of drinking and driving is that many teens participate in this dangerous act. While the national average for underage drunk driving deaths is 1.2 fatalities per 100,000 population, Alabama’s rate is much higher!

Unfortunately, Alabama’s teen fatality rate is among the HIGHEST rates in the U.S. Clearly, underage drinking is a significant problem in Alabama. If you look at the table below, you can see the teen arrest rate in Alabama.

Alabama only ranks 48th in the U.S. for the number of underage arrests for drinking and driving, even though there is a high number of underage fatalities.

Alabama Transportation

In today’s busy world, there is always somewhere to be! From work to dinner with friends, driving is by far the most common means of transportation.

Car Ownership in Alabama

| Number of Vehicles per Household | Percentage of Households |

|---|---|

| 0 | 5% |

| 1 | 20% |

| 2 | 40% |

| 3 | 25% |

| 4 | 7% |

| 5+ | 3% |

You’ll need a car to drive. Most Alabama residents have more than one, though. Ownership of two to three cars is the norm, which is a lot of cars!

Commute Time in Alabama

| Commute Time (Minutes) | Percentage of Commuters |

|---|---|

| Less than 5 | 3% |

| 5–9 | 8% |

| 10–14 | 12% |

| 15–19 | 16% |

| 20–24 | 14% |

| 25–29 | 6% |

| 30–34 | 10% |

| 35–39 | 4% |

| 40–44 | 5% |

| 45–59 | 7% |

| 60–89 | 9% |

| 90+ | 6% |

The average commute time in the U.S. is 25.3 minutes. Alabama’s commute is slightly less, which is good news for Alabama drivers. A few minutes saved each day may not seem like much, but if you had a long drive before, you’d quickly appreciate those extra minutes.

The Best Auto Insurance Quotes in Alabama

Start comparing shopping today by entering your ZIP code using our free online tool below to find Alabama’s best auto insurance quote.

Before making final decisions on your insurance company, learning as much as possible about your local insurance providers and their coverages is crucial. Call your local insurance agent to find out how much car insurance is in Alabama on average.

Questions to consider include, “What are the minimum coverage requirements in my state, and what form of coverage do you recommend?” “Do you guys offer any bundle discounts if I take out both my auto and home insurance with you?” and “What is the average rate of insurance quotes you guys offer?”

Before making big insurance decisions, use our free tool below to compare insurance quotes and find out how much car insurance you need.

Frequently Asked Questions

What are Alabama’s minimum car insurance requirements?

Alabama requires drivers to carry liability insurance with minimum limits of $25,000 for bodily injury per person, $50,000 for bodily injury per accident, and $25,000 for property damage per accident.

Is car insurance mandatory in Alabama?

Yes, Alabama law mandates that all drivers have at least the minimum required liability insurance. If you are caught driving without insurance, you will be fined, your license suspended, or your vehicle registration suspended.

What are Alabama’s penalties for driving without insurance?

A driver’s first offense can result in a fine of up to $500, suspension of registration, and reinstatement fees. Subsequent violations can result in fines of up to $1,000, a 6-month license suspension, and higher reinstatement fees.

What is SR-22 insurance, and when is it required in Alabama?

Drivers with violations such as DUIs or driving without insurance must have an SR-22. This certificate of financial responsibility proves they carry the state-required minimum insurance.

Does Alabama use a fault-based system for car accidents?

Yes, Alabama is a fault-based state. If the driver who caused the accident is found to be at fault, they are responsible for covering damages and injuries through their insurance.

What is uninsured/underinsured motorist coverage, and is it required in Alabama?

If you’re in an accident with an uninsured or underinsured driver, this coverage protects you by covering the difference. While it’s not mandatory, Alabama insurers must offer it, and you can reject it in writing.

How can I lower my Alabama car insurance premiums?

There are numerous ways to reduce your premiums: shop around and compare rates to get a good Alabama car insurance quote. Enter your ZIP code below and use our comparison tool to do this.

Next is to maintain a clean driving record by driving safely. You can even use a telematic program to encourage safer driving and get bonus discounts. You can also bundle policies such as home and auto insurance to get discounts from some insurers.

Also, take advantage of discounts for good driving, multiple vehicles, or safety features, and increase your deductible if it’s financially feasible.

Does Alabama require proof of insurance?

Yes, you must carry proof of insurance in your vehicle. You must show it for renewal or when law enforcement asks.

What factors affect Alabama car insurance rates?

A few factors will influence your rates, such as driving history, age, gender, marital status, vehicle make and model, location, and credit score.

What is the grace period for car insurance in Alabama?

Alabama does not have a mandatory grace period. Failing to renew or maintain coverage can result in penalties or a lapse in coverage.

Related Articles

-

Mar 2025

Best Car Insurance in West Virginia for 2026 [Compare the Top 10 Companies]

-

May 2025

Best Car Insurance in Minnesota for 2026 [MN’s Top 10 Companies]

-

Apr 2025

Best Car Insurance in Wisconsin for 2026 [Check Out the Top 10 Companies]

-

Mar 2025

Best Car Insurance in North Carolina for 2026 [10 Standout Companies]

-

May 2025

Best Car Insurance in Idaho for 2026 [Find the Top 10 Companies Here]

-

Mar 2025

Best Car Insurance in New Jersey for 2026 [Compare the Top 10 Companies]

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.